Guide on GST Penalties under Sections 73, 74 & 74A

Table of Contents

Complete Guide on GST Penalties under Sections 73, 74 & 74A

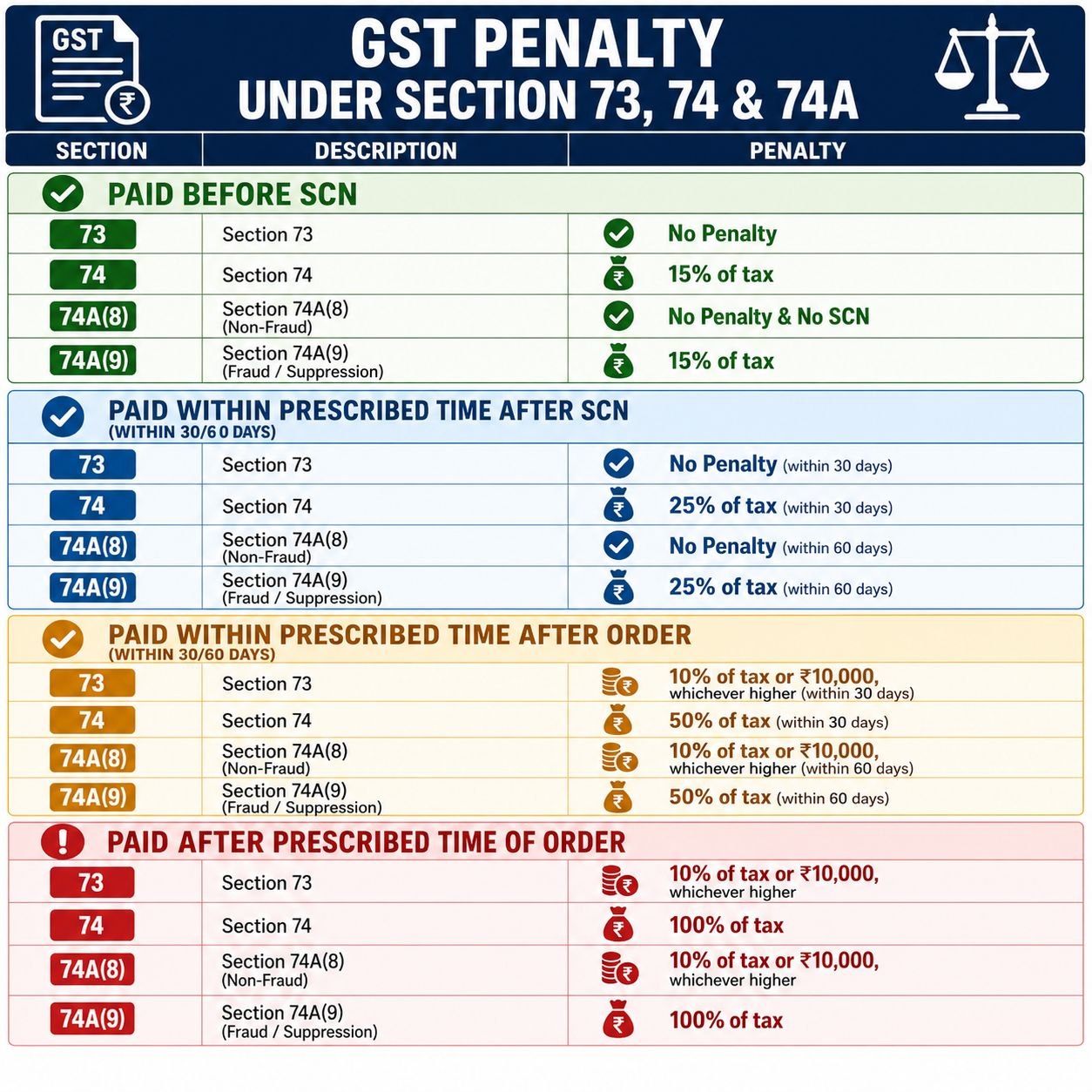

Under this article we are going to summarize the penalty provisions applicable under different GST demand and recovery sections. Section 73 deals with non-fraud cases; Section 74 deals with fraud, willful misstatement, or suppression of facts; and Section 74A (introduced from FY 2024-25 onwards) provides a common framework for demand and recovery proceedings with separate treatment for fraud and non-fraud cases.

Section 73 – Non-Fraud Cases

Applicable where tax has not been paid, short paid, erroneously refunded, or input tax credit wrongly availed/utilized without fraud, willful misstatement, or suppression of facts.

If Tax is Paid Before Show Cause Notice

- Tax + Interest paid voluntarily.

- No Penalty.

- Show Cause Notice is generally not issued for the amount paid.

If Paid Within 30 Days of Show Cause Notice

- Tax + Interest paid within 30 days of SCN.

- No Penalty.

If Paid Within 30 Days of Order

- Tax, interest, and penalty are payable.

- Penalty = 10% of Tax or ₹10,000, whichever is higher.

If Paid After 30 Days of Order

- Penalty remains 10% of Tax or ₹10,000, whichever is higher.

Section 74 – Fraud / Suppression Cases

Applicable where tax is unpaid or short paid due to Fraud, Wilful misstatement, Suppression of facts and Intent to evade tax

If Paid Before Show Cause Notice (SCN)

- Tax + Interest + Penalty

- Penalty = 15% of Tax

If Paid Within 30 Days of Show Cause Notice (SCN)

- Tax + Interest + Penalty

- Penalty = 25% of Tax

If Paid Within 30 Days of Order

- Tax + Interest + Penalty

- Penalty = 50% of Tax

If Paid After 30 Days of Order

- Tax + Interest + Penalty

- Penalty = 100% of Tax

Section 74A – Common Demand Provision

Section 74A has replaced the separate approach for future periods by creating a unified demand mechanism while distinguishing fraud and non-fraud cases.

A. Section 74A(8) – Non-Fraud Cases

- Before Show Cause Notice : Tax + Interest paid. and No SCN and No Penalty.

- Within 60 Days of Show Cause Notice : Tax + Interest paid. and No Penalty.

- Within 60 Days of Order : Penalty = 10% of Tax or ₹10,000, whichever is higher.

- After 60 Days of Order : Penalty = 10% of Tax or ₹10,000, whichever is higher.

B. Section 74A(9) – Fraud / Suppression Cases

- Before SCN : Penalty = 15% of Tax

- Within 60 Days of Show Cause Notice : Penalty = 25% of Tax

- Within 60 Days of Order: Penalty = 50% of Tax

- After 60 Days of Order: Penalty = 100% of Tax

Quick Comparison on GST Penalties under Sections 73, 74 & 74A

Interest is payable in all cases where tax is recoverable. Early payment significantly reduces penalty exposure. The key distinction between Section 73 and Section 74 is the presence of fraud, suppression, or willful misstatement. Under Section 74A, the benefit period after the Show Cause Notice and order has been extended to 60 days. Proper documentation and voluntary compliance before Show Cause Notice can completely eliminate penalties in non-fraud cases.

| Stage | Section 73 | Section 74 | Section 74A(8) | Section 74A(9) |

|---|---|---|---|---|

| Before Show Cause Notice | No Penalty | 15% | No Penalty & No SCN | 15% |

| After Show Cause Notice | No Penalty (30 days) | 25% | No Penalty (60 days) | 25% |

| After Order (within prescribed period) | 10% of tax or ₹10,000 | 50% of tax | 10% of tax or ₹10,000 | 50% of tax |

| After prescribed period | 10% of tax or ₹10,000 | 100% of tax | 10% of tax or ₹10,000 | 100% of tax |

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.