Guide to GSTR-1 Table-Wise Details Reporting

Table of Contents

Guide to GSTR-1 Table-Wise Details Reporting

GSTR-1 is a GST return used for reporting all outward supplies (sales) made during a tax period. It contains invoice-wise details of taxable supplies, exports, debit notes, credit notes, amendments, and other outward supply transactions. Under this blog we provide a table-wise summary of transactions to be reported in GSTR-1, helping taxpayers identify the correct table for various outward supplies. Key Facts

| Particulars | Details |

| Return Name | GSTR-1 |

| Purpose | Reporting Outward Supplies (Sales) |

| Filed By | Regular GST-registered taxpayers |

| Frequency | Monthly or Quarterly |

| Monthly Due Date | 11th of the succeeding month |

| Quarterly Due Date (QRMP) | 13th of the month following the quarter |

| Filing Portal | www.gst.gov.in |

GSTR-1 is the primary GST return for reporting sales transactions. The information furnished in GSTR-1 serves as the basis for:

- Generation of recipient’s GSTR-2A

- In case of Generation of recipient’s GSTR-2B

- Availment of Input Tax Credit (ITC) by recipients

- Government matching and reconciliation of transactions

- Therefore, accurate filing of GSTR-1 is critical to avoid notices, mismatches, and ITC disputes

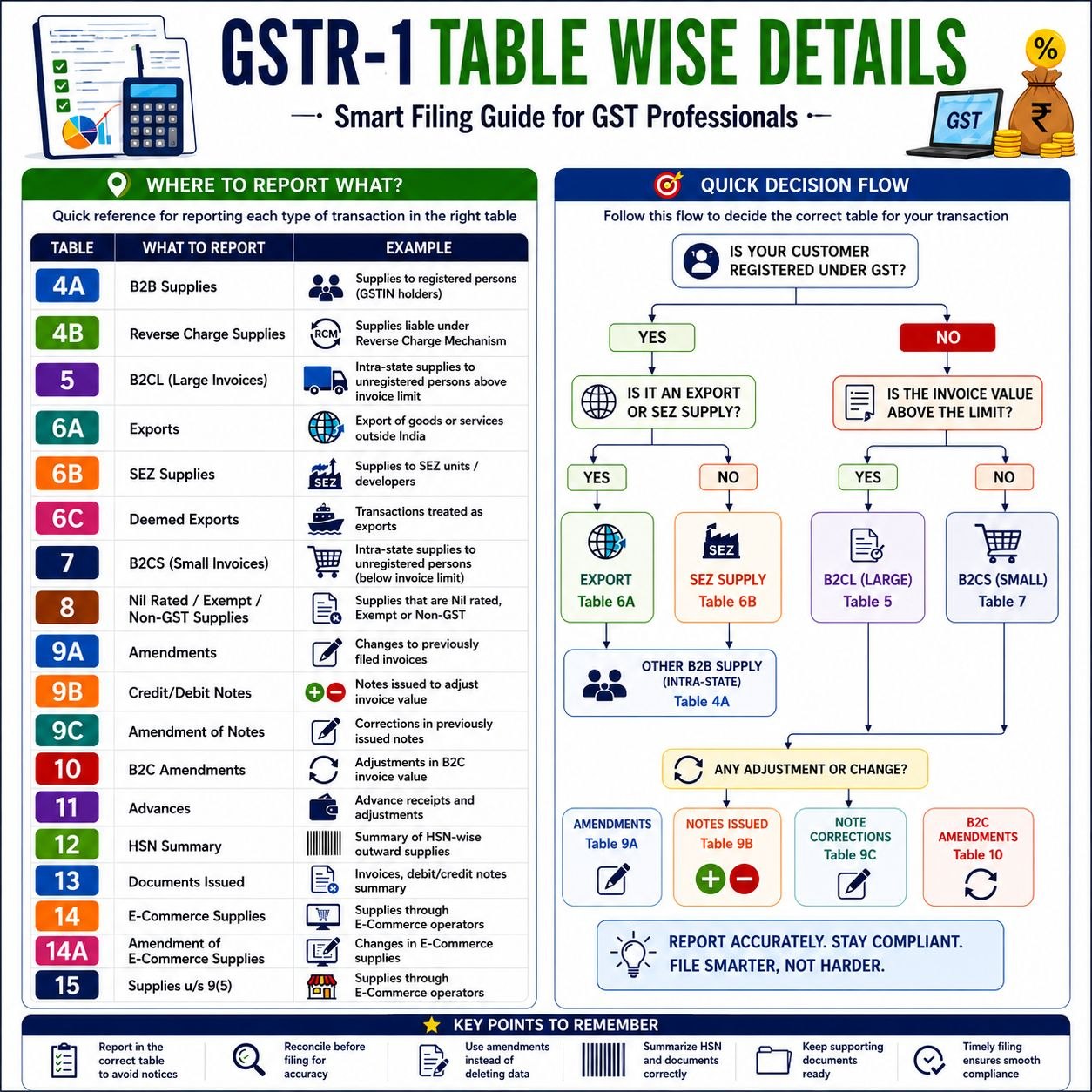

Table-wise Reporting in GSTR-1

A proper table-wise classification in GSTR-1 helps ensure accurate reporting and smooth ITC flow to recipients and minimizes GST notices and reconciliation issues. following are Table-wise reports in GSTR-1:

| Table | Particulars | What to Report |

| 4A | B2B Supplies | Taxable supplies made to registered persons (GSTIN holders). |

| 4B | Reverse Charge Supplies | Supplies on which recipient is liable to pay GST under RCM. |

| 5 | B2CL (Large Invoices) | Interstate supplies to unregistered persons exceeding the prescribed invoice value limit. |

| 6A | Exports | Export of goods or services outside India. |

| 6B | SEZ Supplies | Supplies made to SEZ units or SEZ developers. |

| 6C | Deemed Exports | Transactions notified as deemed exports under GST law. |

| 7 | B2CS | Supplies made to unregistered persons not covered under B2CL. |

| 8 | Nil Rated / Exempt / Non-GST Supplies | Supplies attracting nil rate, exempt supplies, and non-GST supplies. |

| 9A | Amendments to B2B Invoices | Corrections in previously reported B2B invoices. |

| 9B | Credit/Debit Notes | Credit notes and debit notes issued against original invoices. |

| 9C | Amendment of Notes | Changes in previously reported credit/debit notes. |

| 10 | B2C Amendments | Amendments to B2C supplies were reported earlier. |

| 11 | Advances | Advances received and adjustments against supplies. |

| 12 | HSN Summary | HSN-wise summary of outward supplies. |

| 13 | Documents Issued | Invoice series, debit notes, credit notes, vouchers, etc. |

| 14 | E-Commerce Supplies | Supplies made through E-Commerce Operators (ECO). |

| 14A | Amendment of E-Commerce Supplies | Corrections relating to supplies reported in Table 14. |

| 15 | Supplies u/s 9(5) | Supplies through ECO where tax is payable by the operator under Section 9(5). |

Quick Decision Flow – GSTR-1 Table-Wise Details Reporting

- Is the customer registered under GST? : If YES

- Is it an Export? : Report in Table 6A

- if it Supply to SEZ? : Report in Table 6B

- Other Regular B2B Supply : Report in Table 4A

If NO (Customer Unregistered)

- Is Invoice Value Above B2CL Limit?: Report in Table 5 (B2CL)

- Invoice Value Below Limit: Report in Table 7 (B2CS)

Any Corrections Required? then GSTR-1 Table-Wise Details Reporting

| Nature of Correction | Table |

| Invoice Amendment | Table 9A |

| Credit/Debit Note | Table 9B |

| Amendment of Notes | Table 9C |

| B2C Invoice Amendment | Table 10 |

Important Practical Points related to GSTR-1

- Table-4A – B2B Supplies: Include taxable invoices to registered persons, supplies to composition dealers, and supplies attracting forward charge.

- Table-4B – Reverse Charge Supplies: Report invoices where supply is made but tax will be paid by the recipient under RCM.

- Table-5 – B2CL: Typically includes interstate B2C supplies exceeding the notified invoice threshold.

- Table-6A – Exports: Report exports with payment of IGST and exports under LUT/bond without payment of IGST.

- Table-8 – Nil Rated/Exempt: Examples Healthcare services and educational services. Fresh fruits and vegetables and Petroleum products (non-GST)

- Table-11 – Advances: Applicable where GST is required on advances received and subsequent adjustments.

- Table-12 – HSN Summary: Must report HSN-wise quantity, taxable value, and tax details.

- Table-13 – Documents Issued: Includes a summary of tax invoices, revised invoices, debit notes, credit notes, receipt vouchers, and refund vouchers.

- Tables-14 & 15 – E-Commerce Transactions: Important for sellers operating through Amazon, Flipkart, Swiggy, Zomato, etc., and Section 9(5) transactions where GST liability rests with the ECO.

Common Errors to Avoid in GSTR-1

Reporting B2B sales in B2C tables, incorrect GSTIN of recipient, mismatch between GSTR-1 and GSTR-3B, omitting credit notes/debit notes, incorrect HSN reporting, and missing export invoices. And errors in e-commerce turnover reporting.

Compliance Checklist Before Filing GSTR-1

- Reconcile sales register with GSTR-1.

- Verify GSTIN of all B2B customers.

- Match exports with shipping bills.

- Verify SEZ supplies separately.

- Check all credit/debit notes.

- Validate HSN summary.

- Verify document series.

- Reconcile with GSTR-3B before filing.

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.