Key Highlights of Income Tax Act 2025 for FY 2025-26

What Taxpayers & Professionals Should Know about Income Tax Act, 2025

India’s Income-tax framework in 2025 continues to evolve towards simplification, digitization, and transparency, with a strong emphasis on voluntary compliance and technology-driven administration. Here are the key takeaways for FY 2025-26 & beyond.

- Faceless & Technology-Based Regime : Assessments, appeals, rectifications, refunds, and even penalty proceedings are increasingly faceless, reducing human interface while enhancing objectivity and accountability.

- Greater Data Matching & Reporting : Income and transactions are closely monitored through AIS & TIS, including salary & interest income, capital gains (equity, property, securities), crypto/virtual digital assets (VDA), foreign income & assets, and high-value financial transactions. Mismatch = Automated notice

- The Income Tax Dept. has made stricter disclosure norms for mandatory and accurate disclosure of foreign income & foreign assets, VDAs (crypto transactions), & high-value investments & transfers. Nondisclosure may lead to heavy penalties, interest, and prosecution in case of serious cases.

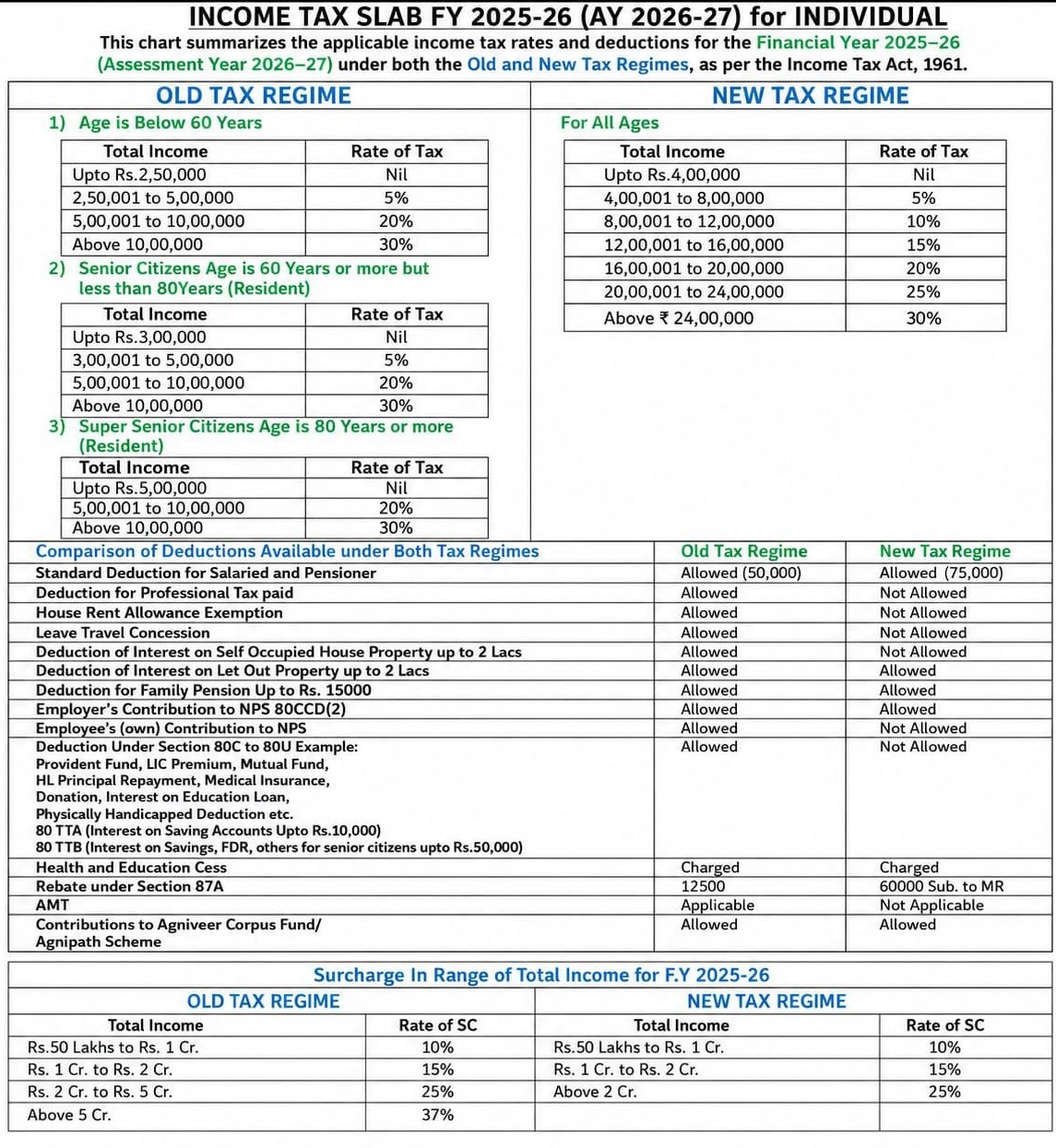

- New vs Old Tax Regime : New Tax Regime continues as the default option, & Taxpayers may still opt for the Old Regime after proper evaluation, Wrong regime selection can result in higher tax outgo

- Faster Corrections & Rectifications: The tax dept has enhanced powers of CPC to correct refund issues, rectify tax credit mismatches, fix interest computation errors & lessen litigation, and speed up resolution .

- Strong Focus on Ease of Compliance: The tax dept is trying to make simplified ITR forms, Pre-filled return data, online notice responses & Time-bound grievance redressal

Before filing your ITR, the taxpayer must reconcile AIS & TIS, review Form 26AS & disclose all foreign income/assets, and choose the correct tax regime. Smart planning > risky tax-saving tricks. The taxpayer may call us. For assistance with ITR filing, revision, notice replies, or tax planning, you may contact us.

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.