All about the Latest GST Amendments for FY 2024–25 & 2025–26

Table of Contents

All about the Latest GST Amendments for FY 2024–25 & FY 2025–26

GST is firmly moving towards real-time compliance, system-driven checks, and accountability. Businesses must shift from reactive filing to continuous compliance monitoring. The government has introduced far-reaching reforms in the GST framework for FY 2025–26, aimed at improving ease of doing business, tax governance, digital security, and operational consistency. With the new financial year underway, businesses must realign systems, processes, and controls to remain compliant. This article outlines the key GST rule changes for FY 2025–26 and their business impact.

Input Tax Credit (ITC) – Tightened Conditions

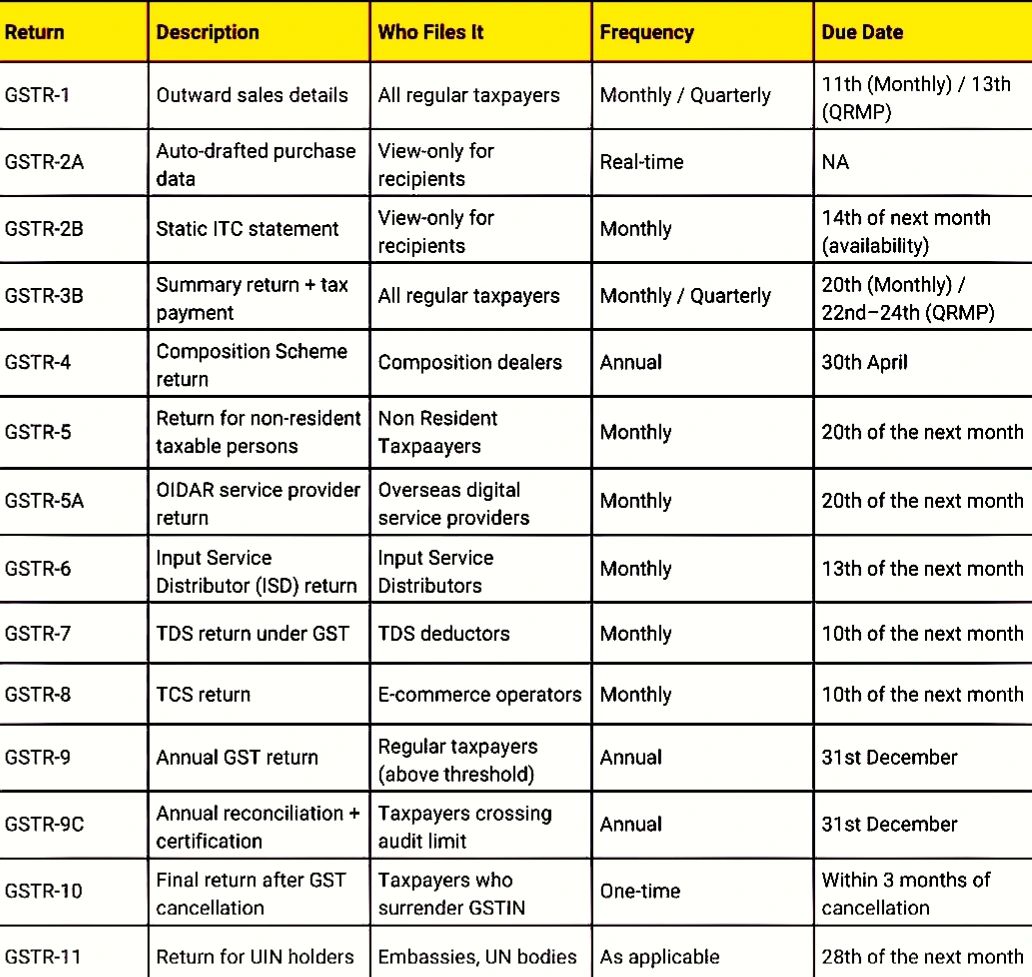

- Supplier GSTR-1 & GSTR-2B requirement: Input Tax Credit may now only be claimed if the supplier has filed GSTR‑1, and the credit appears in the purchaser’s GSTR‑2B.

- Timely GST payment by supplier: Suppliers must make GST payment within 180 days of invoice date; otherwise, recipients must reverse claimed Input Tax Credit with interest.

- Invoice-level verification via Invoice Management System (effective Oct 2024/Oct 2025): Buyers are mandated to Accept, Reject, or Mark Pending invoices in the Invoice Management System before claiming ITC in GSTR‑3B. Deemed acceptance occurs if no action is taken.

- Not taking action leads to deemed acceptance.

- Updates in Oct 2025 allow remarks, partial reversals, new statuses, and invoice-level ITC declarations.

E-Invoicing – Strict Upload Timeline

- 30‑day generation window: From April 2025, taxpayers with AATO over INR10 crore must register e‑invoices within 30 days of issuance; submissions beyond this are rejected, affecting ITC eligibility.

- Invoice number case-insensitive: From June 1, 2025, IRNs are treated uniformly for CDs (e.g., abc and ABC are same).

E‑Way Bill – Age Restrictions & New Portal

- E‑Way Bill validity for invoices up to 180 days; extensions allowed up to 360 days—both rules effective January 1, 2025.

- E‑Way Bill 2.0: Launching July 1, 2025, with real-time synchronization and MFA login.

Multi-Factor Authentication – Mandatory for All

- Phased rollout:

- AATO >INR20 crore: from Jan 1, 2025

- AATO >INR5 crore: from Feb 1, 2025

- All users: from April 1, 2025 — requiring OTP, authenticator apps, or similar.

GSTR‑9 (Annual Return) – MSME Relief

- Permanent exemption: Taxpayers with turnover ≤ INR2 crore are exempt from filing GSTR‑9 from FY 2024–25 onward. Those above INR2 crore must file GSTR‑9; turnover >INR5 crore require GSTR‑9C.

- Enhanced reporting structure:

- Input Tax Credit split across years (new Tables 6A1 and 6A2).

- Rule-wise reversal disclosures.

- Deferred Input Tax Credit (claimed by Nov 30).

- Liability-to-payment reconciliation (Table 9).

- Distinct disclosures for credit/debit notes within cutoff dates.

GST Compliance Dashboard & Return Enhancements (FY 2025–26)

- Compliance dashboard (beta): Expected launch in April 2025 offering real-time risk scores, anomaly tracking, and reporting trends.

- GSTR‑3B automation changes:

- From April 2025: GSTR‑3B auto-drafts Input Tax Credit and tax liability from GSTR‑1/GSTR‑2B; Table 3 becomes non-editable from July 2025.

- From July 2025: Returns older than 3 years cannot be filed.

- ISD registration becomes mandatory for entities with multiple GSTINs under one PAN.

Key Impacts & Action Points due to GST Amendments: FY 2024–25 & FY 2025–26

| Area | Impact | Recommended Actions |

| ITC Claims | Higher risk of denial + penalty | Reconcile GSTR‑2B, enable IMS workflows |

| E‑Invoicing | Input Tax Credit loss on delayed reporting | Automate reporting, sync ERP–IRP |

| E‑Way Bill | Transit blocked for old invoices | Monitor invoice age, upgrade logistics |

| MFA Rollout | Access controls tightened | Enable OTP/app-based Multi-Factor Authentication |

| Annual Filings | Less burden for SMEs | Confirm GSTR‑9 eligibility |

| System Changes | Non-editable auto-drafting | Audit GSTR‑1/GSTR‑2B carefully |

Conclusion

Staying updated and proactively implementing these changes—such as using an Invoice Management System for invoice validation, configuring timely e‑invoicing and e‑way bill systems, enabling MFA, and adapting to detailed annual return norms will reduce compliance risks, prevent Input Tax Credit denials, and smoothen GST audits. Compliance Steps

- Monthly Invoice Management System reconciliation and GSTR-2B checks before GSTR-3B.

- ERP updates for 30-day e-invoicing and multi-factor authentication.

- For INR 6 crore turnover firms: Ensure supplier GSTR-1 timeliness to avoid Input Tax Credit denial, interest, and disruptions

India’s GST rules for FY 2025-26 introduce reforms like mandatory ISD registration, MFA for all users, and tightened e-invoicing/e-Way Bill timelines to boost compliance, security, and transparency. These changes replace flexible options like cross-charging with standardized ISD invoicing via GSTR-6, while restricting e-Way Bills to 180-day-old invoices (360-day max extensions). Businesses must update systems promptly to avoid ITC losses, portal blocks, and penalties. Impact on GST Taxpayers

- Non-compliance → ITC denial, interest, penalties, operational disruptions.

- Compliance Actions

-

Register as ISD and configure ERPs for GSTR-6, new formats, and MFA.

-

Reconcile invoices monthly; file pending GSTR-7 sequentially.

-

Update invoicing for 30-day e-reporting and 180-day e-Way limits

-

- Example: Company with ₹6 crore turnover:

- Must upload e-invoices within 30 days.

- Ensure suppliers file GSTR-1 timely.

- Use MFA for portal access.

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.