FAQ’s – Parameters for GST Department Notice

Table of Contents

FAQ’s – Parameters for GST Department Notice

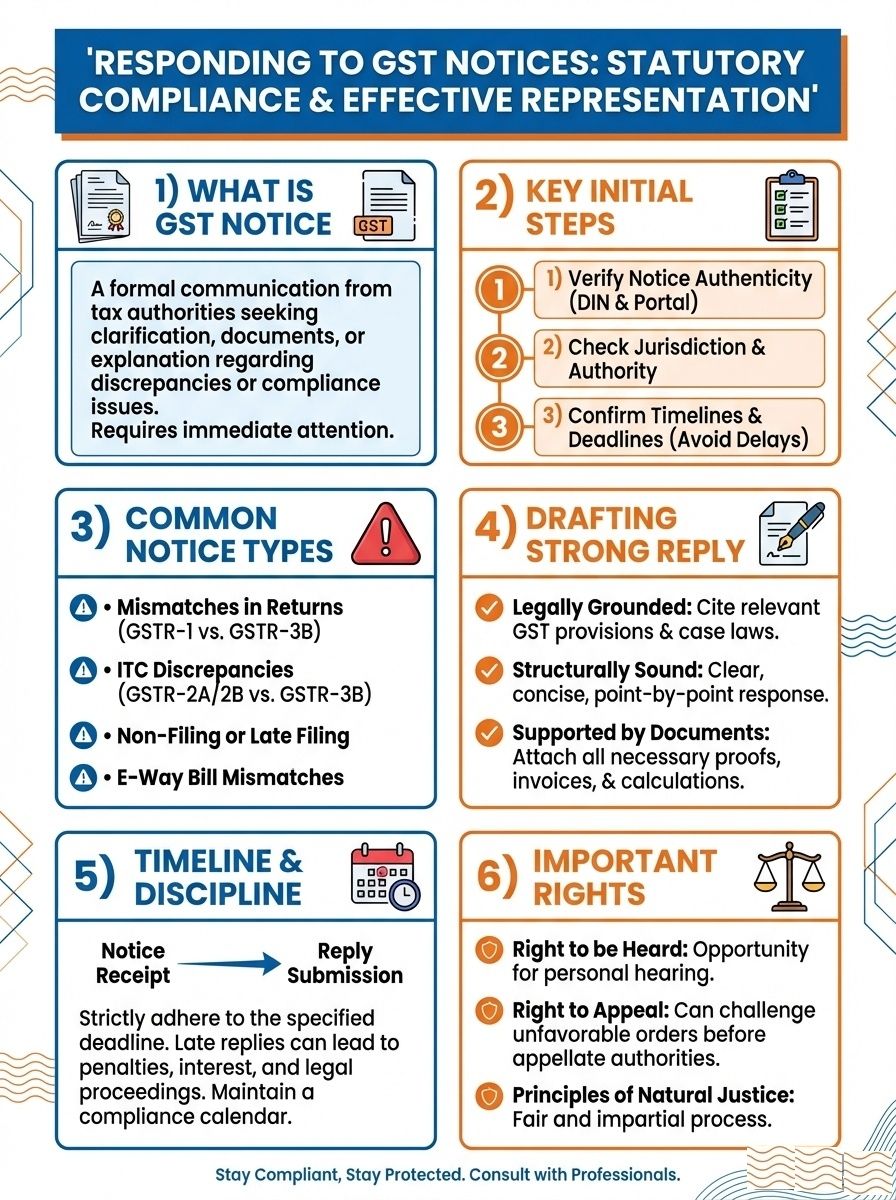

Q.: The GST department issues notices for return scrutiny depending on a variety of characteristics. Why is the department sending out these notices?

Ans: GST Consultants give advice that Officer may analyse the return supplied by the registered person to check the correctness of the return and inform him of the anomalies identified (Form GST ASMT-10) and ask his explanation thereto, as per section 61 – Scrutiny of returns read with rule 99.

Q.: What is your question? What are the many parameters that the GST administration considers when scrutinising returns?

Ans: Responses: The GST department issues notices for return scrutiny based on a total of 15 parameters (Parameters 0069 to 0083) as follows:

- Ineligible ITC claimed by non-genuine taxpayers (NGTPs) whose RC is cancelled from the outset.

- GSTR-1 has a higher outbound tax than GSTR-9/GSTR-3B.

- E-Way Bills have a higher outward tax than GSTR-3B.

- ITC claimed from GSTR-3B that is ineligible Non-filers

- GSTR-9/3B claims an excess ITC that is not supported by GSTR-2A or GSTR-9/8A.

- Suppliers who claimed ineligible ITC from RC have their claims revoked.

- GSTR-1 has a lower turnover rate than GSTR-8 (TCS)

- GSTR-3B has a lower turnover rate than GSTR-7 (TDS)

Q.: Why ITC claims after the last date of ITC availment as per section 16(4) GSTR-3B

- Less RCM obligation declared in GSTR 9/3B/4 than shown by suppliers in GSTR-1

- ITC on purchase invoices uploaded by the supplier in GSTR-1 after the deadline for claiming -section 16 (4)

- Excess IGST on imports reported in GSTR 6E vs. ICEGATE data

- Interest on GSTR 3B payments that are late

- Excess ISD ITC claimed in GSTR9 6G vs. GSTR 2A ISD

- The Excess RCM ITC reported in GSTR9 6CDF vs. liability reported in GSTR 9_4G

Q.: What step should the officer take after receiving an explanation for the situation?

Ans: If the explanation (from GST ASMT-11) is judged to be satisfactory, the registered person will be notified in Form GST ASMT-12 and no further action will be taken.

If no satisfactory explanation is provided, or if the officer accepts the discrepancies but fails to take corrective action in his return for the month in which the discrepancy is accepted, the officer may initiate appropriate action, including those under section 65/66/67, or proceed to determine the tax and other dues under section 73/74, within thirty days of being notified by notice.

Q.: What general precautions should a taxpayer take to avoid the GST department scrutinising their returns, and what conclusion should we draw from this?

Ans: All GST returns must be filed on time, and to prevent such scrutiny, taxpayers should –

- Reconcile the information of outgoing taxes submitted in GSTR-1 with outgoing taxes declared in GSTR-3B/GSTR-9, as well as the E-way bill created.

- Match the ITC claimed by each party in GSTR-3B/9 with the ITC in GSTR-2A/GSTR-9 8A.

- Compare the amount of TCS/ TDS collected and paid through GSTR-8/ 7 to the amount of turnover declared in GSTR-1/ 3B.

- Verify that the tax paid under RCM declared in GSTR-9 4G is greater than or equal to the RCM liability represented in GSTR 2A on the basis of GSTR-1 provided by the supplier, and that the claim made under GSTR-9 6D is less than or equal to the RCM liability reflected in GSTR 2A.

- Ensure that GSTR-3B is filed on time and that, if there is a delay in filing the return, any interest owing on taxes discharged through the cash component is paid on time.

- Reconcile IGST paid and imports on ICEGATE with GSTR-9 6E and GSTR-3B 4(A)(1) claims (4).

- The auditor must verify that the tax reported on GSTR-9 6G is less than or equal to GSTR-2A ISD, and that GSTR-9 4G is larger than or equal to GSTR-9 6CDF.

Q.: What are the issues that a taxpayer will encounter?

Ans: It is sometimes the case that the honest taxpayer pays for the mistakes of others, such as in the ITC parameters, even though the honest taxpayer suffers as a result of the mistake of another taxpayer.

Q.: When is the GST ASMT 10 notice issued?

Ans : If there are any anomalies in the GST return, the GST officer will issue an ASMT 10 to the taxpayer.

Q.: How do I submit an ASMT 10 clarification?

Ans. The taxpayer can use the GST portal to submit his or her response.

Q.: What is the deadline for responding to ASMT-10?

Ans. A taxpayer must respond within 30 days after receiving the notice.

Q.: Which format should you use to respond to ASMT 10?

Ans. To respond to the notice, the taxpayer must use the ASMT 11 format.

Q.: What happens if a response isn’t sent inside the time frame?

Ans. The department may take action under sections 65, 66, and 67, or pursue tax recovery under sections 73 and 74.

About IFCCL

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.