Finance Bill 2025 Impact on Blocked Credit, Credit Note, ISD

Table of Contents

Finance Bill 2025 Impact on Blocked Credit & Credit Note, ISD

The Finance Bill 2025 introduces key amendments under the GST framework, significantly impacting input service distributors, blocked credits, and credit notes. The amendments streamline tax credit distribution, remove ambiguities in blocked credit and credit note adjustments, and settle the taxation of vouchers. These changes enhance Input tax credit efficiency, reduce disputes, and ensure better compliance under GST. Here’s a breakdown of the key changes:

Input Service Distributor: Expanded Scope

- Amendment in Definition: The definition of input service distributors now explicitly includes the ability to distribute input tax credit on interstate services procured under RCM. The revised definition now allows input service distributors to claim credit on taxes paid under the RCM for interstate inward services. Businesses can distribute Reverse Charge Mechanism-paid tax credits on common input services across their branches, enhancing efficiency and reducing tax costs.

- These amendments enable input service distributors to distribute credit of RCM-paid IGST for common services across distinct persons as per sections 5(3) & 5(4) of the Integrated Goods and Services Tax Act, 2017. 1 April 2025, aligning with the implementation timeline of earlier ISD-related amendments under Finance Act 2024. This means the businesses can pool and distribute RCM credit effectively across branches. Which Helps in seamless input tax credit utilization and reduces compliance burdens.

Blocked Credit: Retrospective Clarity on “Plant & Machinery”

- Clarification in Section 17(5)(d): The term “plant or machinery” is now explicitly defined as “plant and machinery,” and this change is retroactively applicable from July 1, 2017. Courts had earlier interpreted the phrase ambiguously, leading to disputes. The Finance Bill 2025 amendment removes uncertainty in claiming Input tax credit on capitalized plant and machinery but continues to block credit for immovable property construction.

- Section 17(5)(d) of the Central Goods and Services Tax Act, 2017: Clarifies that the term “plant and machinery” applies retrospectively from 1 July 2017. Reinforces that Input tax credit remains blocked for construction-related expenses, except for capitalized plant & machinery. This impact and retrospective effect may impact pending litigations. Businesses need to reassess earlier Input tax credit claims on immovable property.

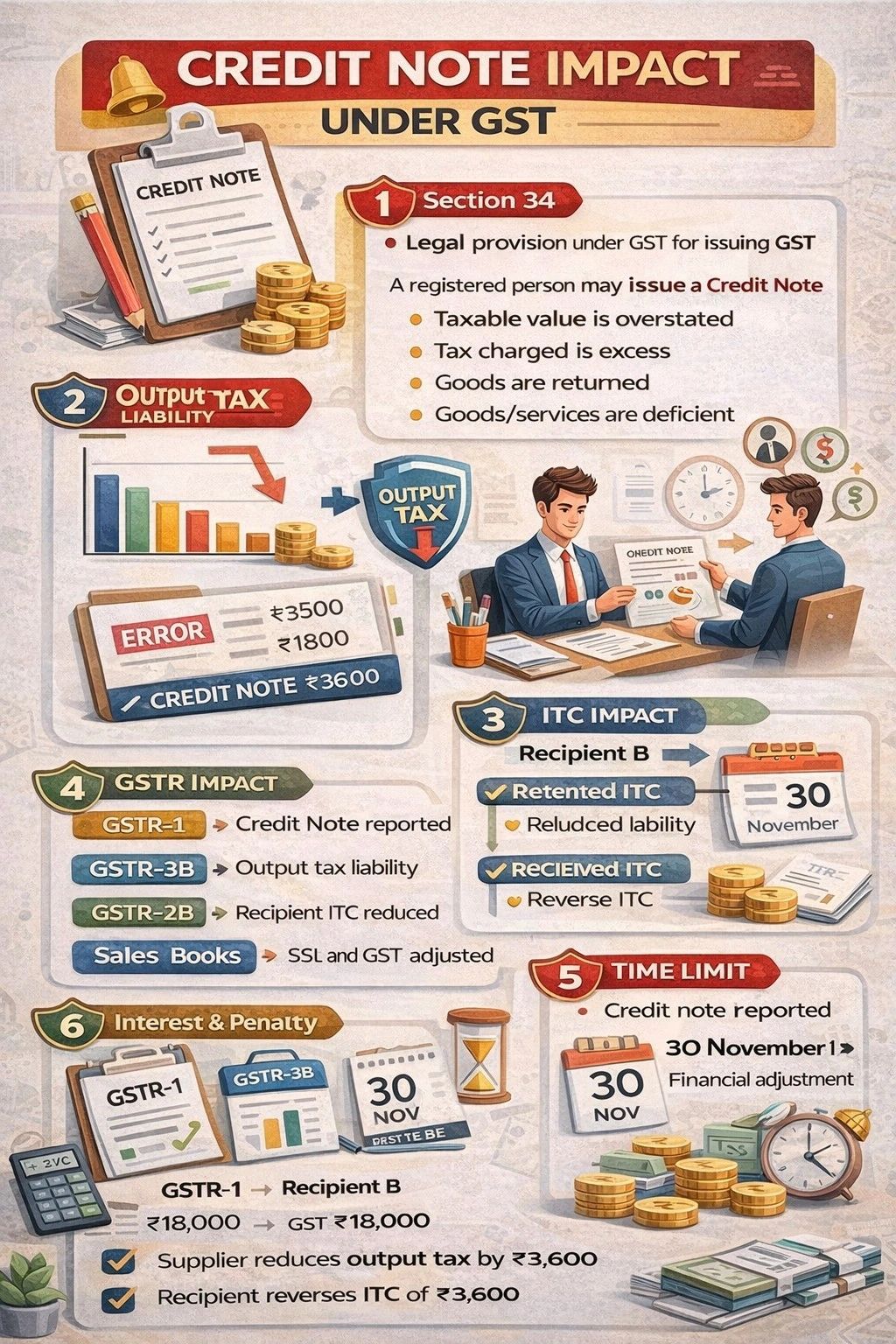

Credit Note: New Conditions for Tax Liability Adjustments

- Amendment in Section 34(2): Suppliers can now only reduce output tax liability through credit notes if Goods and Services Tax invoices has not availed of input tax credit on the corresponding supply. The tax burden has not been passed on to another party. This prevents double benefits, ensuring credit reversal aligns with tax compliance. Proper input tax credit adjustments prevent misuse of credit notes. Suppliers must coordinate with recipients to track input tax credit reversals.Credit Note Impact under GST—With Relevant Sections : Credit notes are a vital compliance tool under GST to correct tax liability and ITC mismatches. Below is a section-wise practical explanation every tax professional should know.

- Section 34 – Credit Note under GST : Statutory provision for issuance: A registered person may issue a credit note when the taxable value is overstated, the tax charged is excessive, goods are returned, and goods or services are deficient. Credit notes must be reported in GSTR-1.Impact on Output Tax Liability : Reduction allowed only if conditions are met. Output tax liability can be reduced only when:

- A credit note is declared in return

- The recipient has not availed ITC or has reversed ITC

- A credit note is issued on or before 30th November following the end of the FY

- Or before filing of the annual return, whichever is earlier

If any condition fails, no GST reduction permitted

- Credit Notes impact both supplier & recipient

- Proper reporting + ITC reversal is non-negotiable

- Time limit under Section 34 is crucial to avoid disputes

Section 16(2) – ITC Impact on Recipient

Responsibility of recipient: If the recipient has already availed ITC, ITC must be reversed proportionately, non-reversal may attract Interest u/s 50 or Departmental notice. Return-wise Compliance Flow

Stage Impact GSTR-1 Credit Note reported by supplier GSTR-3B Output tax liability reduced GSTR-2B ITC auto-reduced for recipient Books of Accounts Sales & GST adjusted Time Limit – Section 34(2) : Critical compliance deadline: Credit notes cannot be adjusted in GST if issued after 30th November of the following FY or after filing the annual return.

Post-deadline credit note = Financial adjustment only (No GST impact) : Interest & Penalty Exposure

- Excess ITC retained by recipient → Interest u/s 50

- Wrong / non-reporting → Proceedings u/s 73 or 74

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.