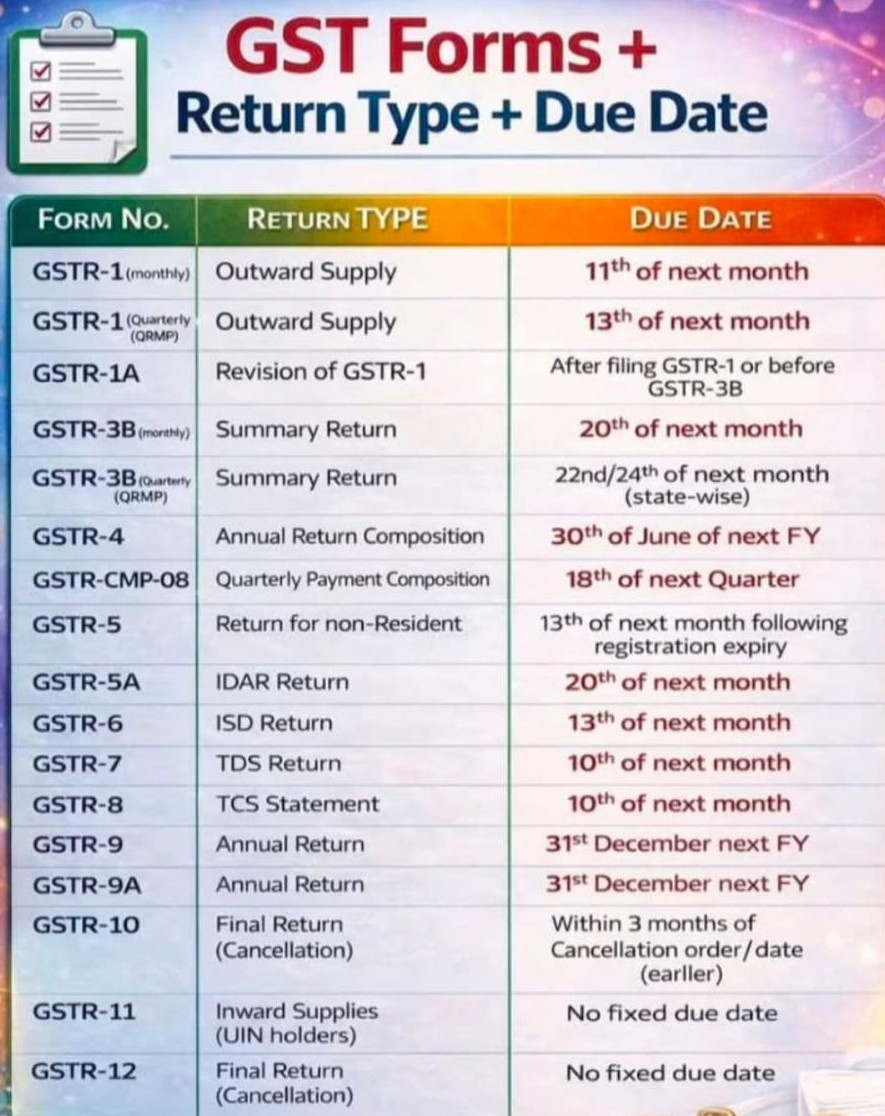

GST E‑Invoicing (AATO INR 5 Cr) Mandate w.e.f. FY 2025‑26

Table of Contents

Applicability Check Threshold & Entity for GST E‑Invoicing Mandate (AATO INR 5 Cr)

Applicability – AATO INR 5 Cr Threshold: E‑invoicing is mandatory for businesses whose Aggregate Annual Turnover (AATO) exceeds INR5 crore in any financial year since FY 2017‑18, based on PAN level—this includes all GST registrations under that PAN. From 1 April 2025, any entity with PAN-level AATO ≥ INR10 crore must strictly upload invoices within 30 days to avoid rejection and ITC denial. Businesses crossing INR5 crore are already within the e-invoicing regime, with the 30-day timeline tightening compliance for mid-sized firms. Taxpayer must ensure your systems, processes, and teams are aligned well before the new financial year starts. (Governed by Rule 48(4) of CGST Rules, 2017).

GST E‑Invoicing Mandate in case Aggregate turnover exceeded applicable limit in any FY since 2017-18 – INR 500 Cr → INR 100 Cr → INR 50 Cr → INR 20 Cr → INR 10 Cr (as notified from time to time)

GST E‑Invoicing Mandate Applicable to:

- B2B supplies

- Exports

- Deemed exports

- SEZ supplies (SEZ Developer/Unit – subject to notifications)

GST E‑Invoicing Mandate Not applicable to:

- B2C invoices (QR Code applies separately)

- Delivery challans (except where notified)

GST E‑Invoicing Entity is NOT exempt: (Exempt: SEZ units*, insurance, banking, NBFCs, GTA, passenger transport, cinema exhibitors, govt departments)

GST E‑Invoicing Mandate required document Types & Coverage

Mandatory for issuance of B2B invoices, B2G supplies, Exports (goods & services), & Deemed exports. Covers taxable, exempt, and export supplies under the same PAN. Following are Exempt entities (even if turnover threshold exceeded)

- SEZ units (not developers)

- Banks & NBFCs

- Insurance companies

- Goods Transport Agencies (GTAs)

- Passenger transport services

- Multiplex cinemas.

New 30‑Day Reporting Rule related to GST E‑Invoicing (Effective 1 April 2025):

Businesses with AATO ≥ INR10 crore must upload invoices, credit notes, and debit notes to the Invoice Registration Portal (IRP) within 30 days of issue. Invoices beyond this 30-day window will be rejected by IRP and deemed invalid. Affected documents lose legal status; recipients will be denied Input Tax Credit (ITC) (“No IRN = No ITC”).

Mandatory Multi-Factor Authentication

To strengthen security and data integrity, MFA (two-factor authentication) is now mandatory for accessing the e-Invoice and e-Way Bill portals for all taxpayers, regardless of turnover, from 1 April 2025.

- Earlier, MFA was rolled out in phases based on turnover (e.g., INR20 crore, INR5 crore) during early 2025.

- Make sure all GST portal logins (especially for e-invoicing/e-way bills) include MFA setup (OTP via registered mobile/Sandes app).

Compliance Checklist related to GST E‑Invoicing

Review turnover across all GST registrations under PAN. Upgrade ERP/billing systems for Real‑time reporting, 30‑day upload cutoff &Mandatory Multi‑Factor Authentication for IRP login. GST taxpayer must strengthen internal SOPs:

-

- Timely invoice generation

- IT system validation

- Staff training on new deadlines

Case-Insensitive IRN Generation (Effective 1 June 2025)

From 1 April 2025, taxpayers with an Annual Aggregate Turnover of INR 10 crore and above must report/upload e-invoices (including credit & debit notes) to the Invoice Registration Portal within 30 days from the invoice date.

- If an invoice is dated 1 April 2025, it cannot be uploaded after 30 April 2025.

- The IRP system will reject entries beyond this 30-day window.

Previously, this 30-day restriction applied only to taxpayers with turnover above INR100 crore. The lowered threshold to INR10 crore significantly broadens the compliant group.

The Invoice Registration Portal will treat invoice/document numbers as case-insensitive for IRN generation from 1 June 2025. Invoice numbers will be auto-converted to uppercase during IRN generation. This aims to avoid duplicate IRNs due to letter-case differences and align with GSTR-1 reporting behavior

Fresh Invoice Series & System Updates

While not strictly part of the e-invoicing mandate, many systems are recommending that fresh invoice series be started from 1 April 2025 to align with updated compliance validations in the GST and E-Way Bill systems. This avoids numbering conflicts and ensures proper linkage with IRN generation.

ERP / Software Integration & Process Controls

Given the tightened timelines and system restrictions:

- Ensure ERP/accounting software is fully integrated with Invoice Registration Portal with real-time or near real-time reporting.

- Internal controls must flag invoices approaching the 30-day window to avoid rejections.

- Early automation reduces manual errors and liability risk.

Compliance Risks if Not Followed

- Late reporting (>30 days) = Invoice Registration Portal will reject the e-invoice

- No IRN → invoice may be treated as invalid for claiming ITC

- Manual late reporting (especially above INR10 cr turnover) will attract audit and denial of ITC exposure

- ERP or process delays can cascade into GSTR-1 / GSTR-3B mismatches

Consequences of Non‑Compliance of GST E‑Invoicing Mandate

| Non‑Compliance Action | Consequence |

| Invoice not uploaded within 30 days | IRP rejection; becomes invalid |

| No Invoice Reference Number (IRN) | ITC disallowed for recipient |

Both supplier and recipient are impacted—no ITC for the buyer and legal risk for the supplier.

Summary of E-Invoicing Mandate Changes (FY 2025-26)

| Change | Effective From | Key Impact |

| 30-day reporting rule widened to INR10 Cr+ | 1 Apr 2025 | Stricter reporting timeline |

| MFA mandatory for all taxpayers | 1 Apr 2025 | Enhanced portal security |

| Case-insensitive No Invoice Reference Number handling | 1 Jun 2025 | Prevent No Invoice Reference Number duplicates |

| A fresh invoice series recommended | FY 25-26 start | Better compliance & system alignment |

Our services include:

1. ROC, MCA & LLP compliances

2. Incorporation of Companies/LLPs and related filings

3. Annual & event-based compliances

4. Drafting of resolutions, minutes, notices & agreements

5. Secretarial Audit & Compliance Management

6. Support to CA/CS/CMA firms on outsource basis

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.