Brief about GST E-Invoicing and its application

Table of Contents

Brief about GST E-Invoicing & it’s applicability.

It is mentioned under Rule 48(4) of CGST Act, in which the registered taxpayer companies is mandatory to make invoices, by providing or uploading json file of invoices on IRP (Invoices registration portal) and get an IRN (Invoice Reference Number) which contains a QR code. After going to the process to generate E-Invoice which provided by the Supplier to their buyer is known as E-invoice in GST.

E-Invoice Applicability chart based on turnover

| S.no | Notification No. of Amendment | Annual turnover / (Threshold limit) |

With Effect From |

|

1. |

Central Tax notification no. 61/2020 | 500 crore | 1st October 2020 |

|

2. |

Central Tax notification no. 88/2020 |

100 crore |

1st January 2021 |

|

3. |

Central Tax notification no. 05/2021 |

50 crore |

1st May 2021 |

| 4. | Central Tax notification no. 01/2022 | 20 crore |

1st May 2022 |

| 5. | Central Tax notification no. 17/2022 | 10 crore |

1st October 2022 |

FAQ’s on E-invoicing under GST:

Who is liable for GST e-invoicing?

E-invoicing is liable for the firms in which annual turnover limit goes above the Threshold limit are liable for E-Invoicing.

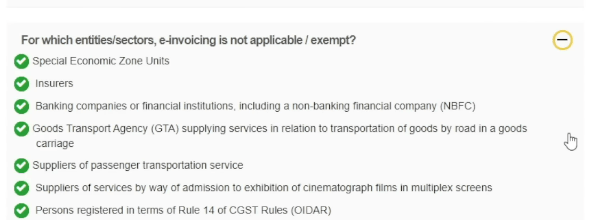

Who is not liable for GST e-invoicing?

What is basic threshold limit for e-invoicing?

- Currently the threshold limit for e-invoicing is 20 crores but after the release of notifications no. 17/2022- central tax, and it changes to 10 crores which come to effect from 1st October 2022.

- For e-invoice which year turnover is to be noted:

- If the annual turnover goes above the threshold limit in any of the previous fiscal year since 2017-18 then the company is applicable for generating E-Invoicing.

For better understanding take a look on case study of Three Companies:

| Financial Year | Turnover of Company A | Turnover of Company B | Turnover of Company B |

| 2016-17 |

12 |

7 |

10 |

|

2017-18 |

9 |

8 |

9 |

|

2018-19 |

7 |

8 | 8 |

|

2019-20 |

8 |

15 |

11 |

|

2020-21 |

9 |

11 |

13 |

|

2021-22 |

5 |

9 |

17 |

| Applicability of E-Invoicing | Not Applicable | Applicable |

Applicable |

Note: All figure mentioned Above are in Crores.

Can an Cancellation and Modifications are applicable in E-invoicing possible ?

Modification cannot be made immediately after generating an E-Invoices. However, the cancellation can be made after completion of 24 hours of getting Invoice Reference Number (IRN).

· After completion of 24 hours, a credit note or debit note can be issued or modification of Form GSTR1 can be done according to the update details, these three options are available for the supplier.

· Cancellation of IRN cannot be done, in case E-way bill is already generated for the IRN.

· After the cancellation of the e-invoice the similar invoice number cannot come to use in generating IRN

· A complete cancellation of e-invoice is allowed but there is option for the half or partial cancellation.

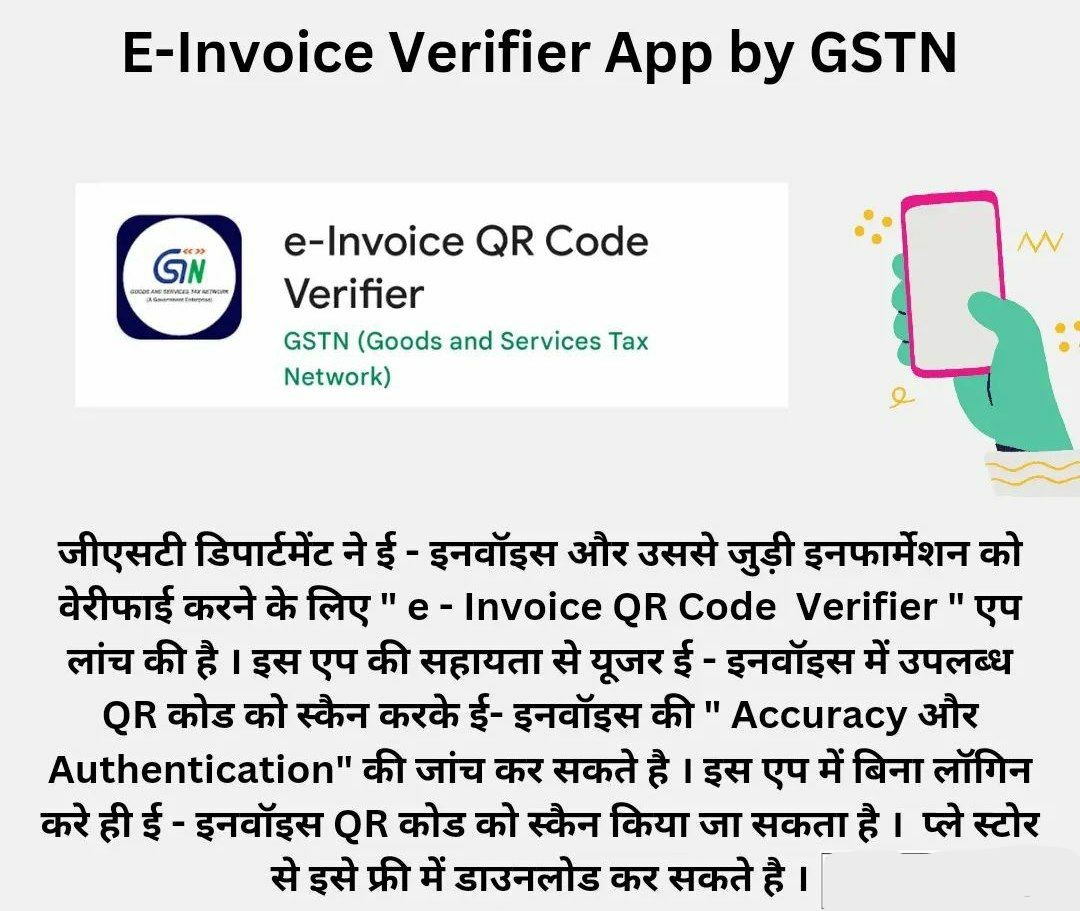

E-invoicing App.

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.