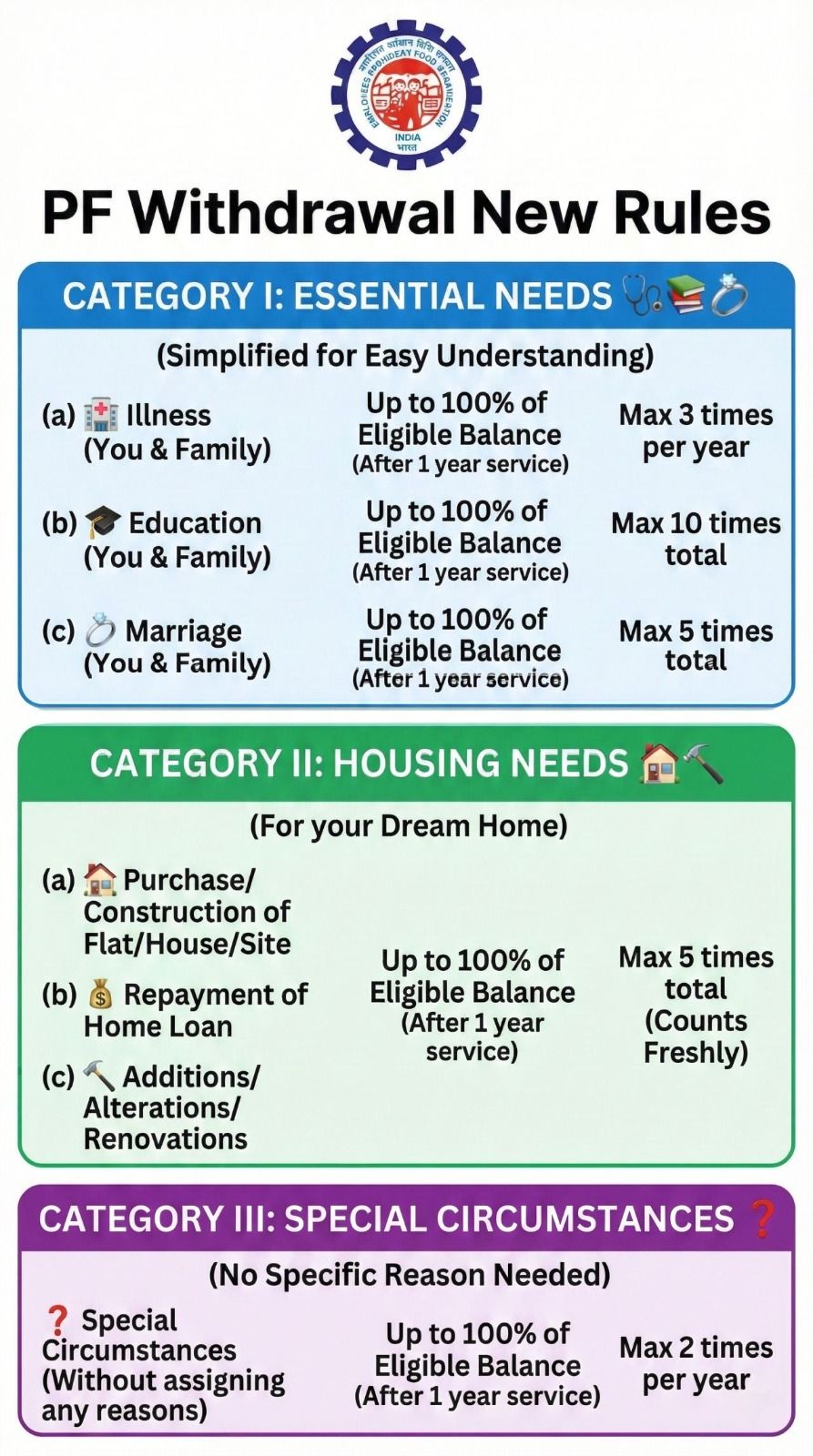

New Labour Codes impact on costs & A/cs Dec 2025 onwards

Table of Contents

New Labour Codes impact on costs & A/cs Dec 2025 onwards

In this blog mention the accounting implications of India’s new labour codes, which came into effect in November. ICAI (Institute of Chartered Accountants of India) has issued guidance that companies must reflect these changes in their financial statements starting from the December Quarter of FY26.

The implementation of the new Labour Codes will have a direct impact on costs and accounting from the December quarter onwards. Companies are required to reassess gratuity and leave encashment liabilities in line with the revised provisions and appropriately recognise & disclose the impact in their financial statements, as highlighted by the Institute of Chartered Accountants of India.

Applicability & Timing : All companies listed & Most unlisted must reassess and reflect increased gratuity and leave liabilities in their interim financial statements for the December 2025 quarter (ending 31 Dec 2025).

Changes Driving the Impact on costs & A/cs Dec 2025 onwards

Expanded Definition of “Wages”: The new labor codes mandate that at least 50% of total remuneration must comprise Basic Pay, dearness allowance, and retaining allowance. Where this threshold is not met, wages are deemed to be 50% of total remuneration. Consequently, gratuity calculations must now be based on a higher “last drawn wage,” significantly increasing liability. The new wage definition requires that basic pay + dearness allowance + retaining allowance form at least 50% of total remuneration. Employers may need to restructure salary components to comply with the 50% wage rule.

Eligibility Extended to Fixed-term Employees : Earlier, gratuity eligibility generally required 5 years of continuous service for permanent employees. Under the new Codes, fixed-term (contractual) employees become eligible after just 1 year, expanding the employee base covered.

Enhanced Leave Obligations: Leave provisions have been widened, including changes in leave entitlements and encashment rights. Any increase in leave-related obligations must be recognised immediately as an expense, leading to higher short-term costs.

Accounting Treatment per Standards

New labour codes will increase companies’ accounting liabilities. Higher gratuity costs must be booked in Dec quarter results. Gratuity payment must be based on last drawn wages for all staff. Paid leave eligibility cut to 180 days from 240. Gratuity liability will rise because it is now calculated on last drawn wages for all employees, including fixed-term employees. The paid leave eligibility threshold was reduced from 240 days to 180 days, making more employees eligible. ICAI states that any increase in gratuity liability due to these changes must be recognized immediately in P&L as per Ind AS 19 and AS 15. Companies need to make accounting adjustments starting in the December quarter 2025.

| Accounting Standard | Treatment of Liability Increase |

| Ind AS 19 | Treated as past service cost, recognised immediately in the Profit & Loss account |

| AS 15 (Indian GAAP) | Similar treatment for vested benefits; for unvested benefits, amortisation over the vesting period is permitted |

Practical & Disclosure Impacts on costs & A/cs Dec 2025 onwards

Increased gratuity and leave liabilities will impact quarterly profitability, affecting EBITDA, PAT, and EPS. Companies will need to:

- Obtain fresh actuarial valuations

- Update payroll and HR systems

- Enhance financial statement disclosures under Ind AS 19 / AS 15

Structural changes to salary composition made to comply with wage norms may themselves constitute plan amendments, triggering additional accounting implications beyond routine actuarial adjustments.

Summary of Immediate Actions required from Dec 2025 onwards

- Reassess gratuity & leave liabilities using revised wage definitions and expanded eligibility criteria.

- Accounting Standards Under Ind AS 19, treat as past service cost, expense immediately. & Under AS 15, similar treatment for vested benefits.

- Higher gratuity and leave liabilities will affect profitability in Q3 FY26. Recognise the additional liability as past service cost in the P&L for Q3 FY26 (Dec 2025).

- Payroll restructuring, actuarial valuation, and disclosure updates are required. Clearly disclose actuarial assumptions, valuation methods, and transitional impacts in the financial statements.

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.