Summary About Income-Tax Filling & Assessments

Table of Contents

Summary about Income-Tax Assessments Procedures, Appeals and Revision

Filing Of Returns:-

Steps Compute income for each Source of Income Aggregate the income from various sources under the respective Heads of Income Arrive at the Gross Total Income Claim the Deductions available Arrive at the Total Income.

Steps Compute Reduce Add the Tax payable on the Total Income the Rebates, if any from the tax payable Surcharge as applicable to the tax Add the Education Cess to the figure of tax plus surcharge Arrive at the Gross Tax Liability.

- Steps From the Gross Tax payable, reduce the TDS Arrive at the Net Tax Payable or the Refund due as the case may be If the net tax payable is equal to or more than Rs. 10,000 then Advance Tax is payable Advance tax is payable in 3 installments (4 in case of companies) during the previous year itself.

- Steps If there is a shortfall in payment of advance tax then calculate Interest u/s. 234B and/or 234C If the return is filed late then calculate Interest u/s. 234A From the net tax payable, reduce the Advance Tax Add the Interest to the balance amount to arrive at the Self Assessment Tax Payable / Net Refund Due.

- Steps Pay the Self Assessment Tax File the Return physically or upload the return electronically.

- Advance Tax [Section 211] :- Advance tax is payable in 3 Installments (4 in case of Companies)— Payable on 15th June 15th September 15th December 15th March— and Where first installment of 15th June is payable only if the assessee is a company.

Self Assessment Tax [Section 140a]

:-When on computation of income for the year for the purpose of filing the return of income it is found that some tax remains payable even after adjustment of advance tax along with deducted/collected at source, such balance tax along with interest thereon is required to be paid as self-assessment tax before filing the returns of income. From A.Y 2013-14, any return uploaded without paying the Self-assessment tax would not be accepted by the Income-tax department and considered defective.

- Return Of Income [Section 139]:- Normal Return Belated Return Revised Return Loss Return Defective Return.

- Normal Return :-Who is required to file return of income — Company or a firm – mandatory requirement — Others – total income exceeds basic threshold limit (i.e. INR 2,00,000 for A.Y. 2013-14)— Any person who is otherwise not required to furnish return of income will be required to file a return if he has any asset located outside India or has signing authority in any account located outside India.

- Belated Return :- Any person who has not furnished a return within the time allowed u/s 139(1) or Within the time allowed under a notice issued u/s— 142(1), but filed before the end of one year from the relevant assessment year or the completion of the assessment, whichever is earlier.

- Revised Return:- Can be filed if the assessee discovers an omission or wrong statement Replaces the original return Can be filed before the end of one year from the relevant assessment year or the completion of the assessment, whichever is earlier Can be revised further Belated return cannot be revised.

- Loss Return:- Return must be filed within the prescribed time limits If not filed, no carry forward of loss, however carry forward of loss under House property head, unabsorbed depreciation & unabsorbed family planning expenses are permissible

- Defective Return:- Incomplete return Assessee may be given an opportunity to rectify the defect If the defect not rectified, the return treated as invalid. Return defective if: columns of return not filled or annexure not— attached; computation of income tax not attached;— proof of tax deposited is not produced within the— period of two years, Non furnishing of tax audit report; etc— Self-assessment tax is not paid (from A.Y 201314).

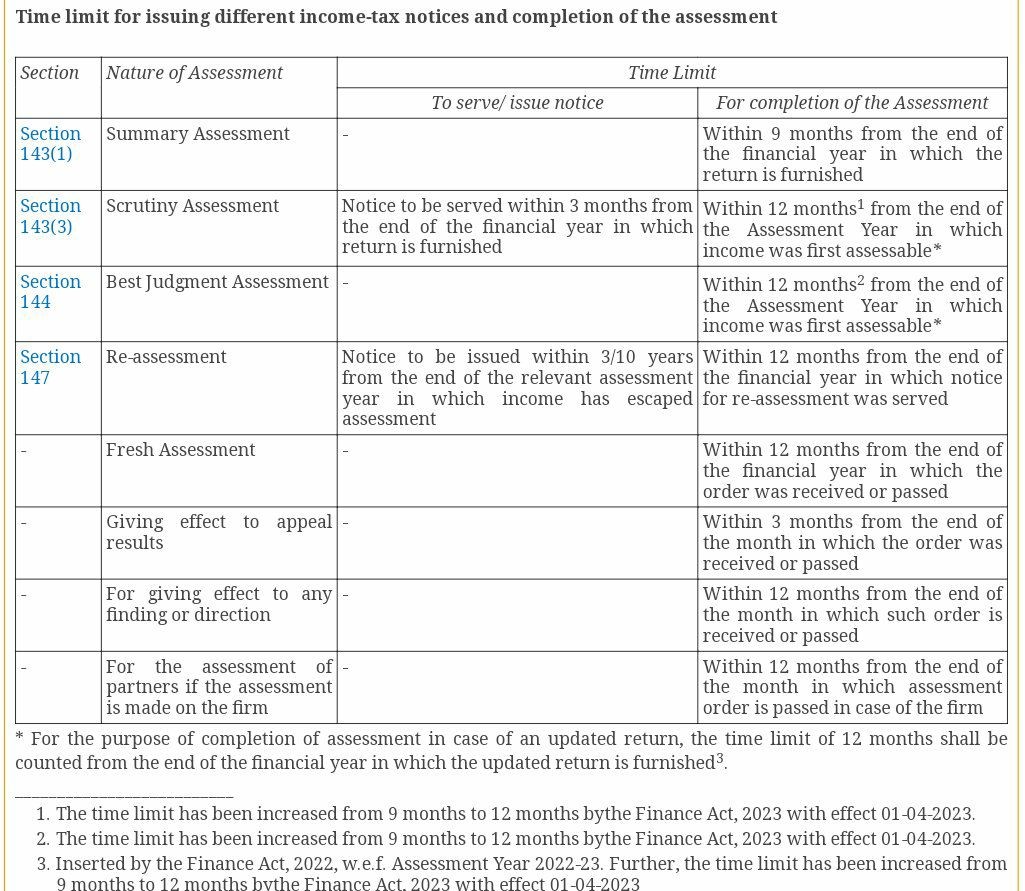

- Return Is Filed – What Next? Either a summary assessment (Section 143(1)) and/or A regular (scrutiny) assessment (Section 143(3)).

Summary Assessment [Sec. 143(1)]:-

To be issued only if there is a demand or a refund due. If no demand/refund then Acknowledgement is deemed to be the intimation Time limit – the end of one year from the relevant assessment year or the completion of the assessment, whichever is earlier .There will be no processing of the returns where assessees are selected for Scrutiny.

State And U.T. Wise Break-Up of Direct Tax Collections

Pre-Assessment and Post-Assessment Tax Collections

- Scrutiny Assessement [Sec. 143 (2)/(3)]:- Time limit for issuing notice Time limit for completing the scrutiny Type of questions that are being asked.

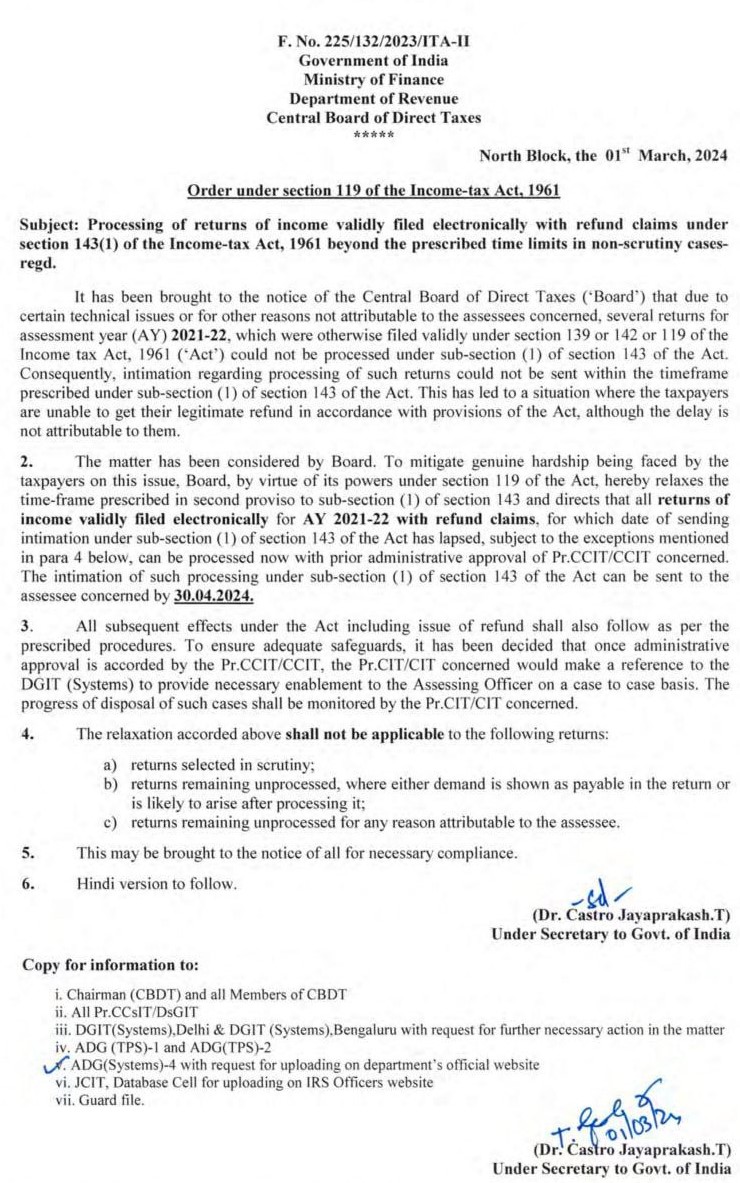

- Processing of returns of income validly filed electronically with refund claims under section 143(1) of the Income-tax Act, 1961 beyond the prescribed time limits in non-scrutiny cases.

- Refunds [Section 237]:- A claim for refund shall be claimed in Form No. 30 Adjustment of refund against demand for another year (Section 245).

- Interest [Section 234a 234d]:-TO SECTION à For Defaults in furnishing return of income [SECTION 234A] à For Failure to Deduct and pay tax at source [SECTION 201(1A)] à Interest for Default in payment of Advance Tax [SECTION 234B].

- Interest [Section 234a 234d]:- A To Section For Deferment of Advance Tax [SECTION 234C] Corporate Assessee [SECTION 234C(1)(a)] Non Corporate Assessee [SECTION 234C(1)(c)] àShort payment of Advance Tax in case of Capital Gains/Casual Income [First Proviso to SECTION 234C(1)].

- Interest [Section 234a 234d]:- Interest à TO SECTION on Excess Refund [SECTION 234D] For à Making Late Payment of Income tax [SECTION 220(2)] Interest à Payable to Assessee [SECTION 244A].

Rectification Of Mistakes [Section 154]:-

Rectification of Mistakes an income-tax authority may with a view to rectifying any mistake apparent from the record: amend any order passed by it-amend any intimation or deemed intimation under- section 143(1) and section 200A. Rectification may also be made on application by the assessee Orders cannot be rectified after expiry of 4 years from the end of the financial year in which order sought to be amended was passed On rectification plea by assessee – Amendment / refusal order to be passed within 6 months from the end of the month in which the application is received by the income tax authority.

INCOME TAX PORTAL UPDATE

- You can now file a rectification application u/s 154 directly with the AO for their assessment orders! A game-changer for taxpayers—no more manual filings or grievance routes.

- Rectification Of Mistakes:- Mistake Obvious and patent- Self evident and reached without debate- Fresh determination of facts should not be required- Misreading of a clear provision of law/ applying an- inapplicable provision/ overlooking mandatory provision Statutory interpretation should not be involved- Record Includes all materials/ documents available at the time- of passing the order of assessment Fresh documents/ materials not recorded at the time of- passing the order cannot be considered Record of any period can be considered.

- Rectification Of Mistakes:- Examples of mistakes apparent from record which can be rectified —Error of law or fact — Clerical or arithmetical error — Error in determination of written down value —Overlooking the obligatory provisions of the legislature — Mistakes arising out of retrospective amendment of law.

- Revision Of Orders By Commissioner [Section 263 & 264]:-

Revision Of Orders By Commissioner U/S 263 Pre-requisites — Erroneous order Record shall include and shall be deemed always to have included all records available at the time of examination by the Commissioner Revised order should be passed before the expiry of 2 years from the end of the financial year in which order sought to be revised was passed Opportunity of being heard should be given to the assessee before passing an order under section 263 Powers of Commissioner – Enhance, modify or cancel the assessment and direct a fresh assessment Appeal can be filed to the Appellate Tribunal against the order under section 263 —Prejudicial to interests of Revenue.

- Revision Of Orders By Commission U/S 264 :- Revision of orders, on own motion of Commissioner or on application by the assessee Revision of order on own motion by the Commissioner, to be passed within one year from date of order sought to be revised Application by assessee should be made within 1 year from date on which the order in question was communicated or date on which assessee came to know of order, whichever is earlier Order to be passed within 1 year from end of financial year in which application is made by assessee for revision Pre-requisite – Assessee to waive right of appeal Where appeal against the order has been filed – no revision possible

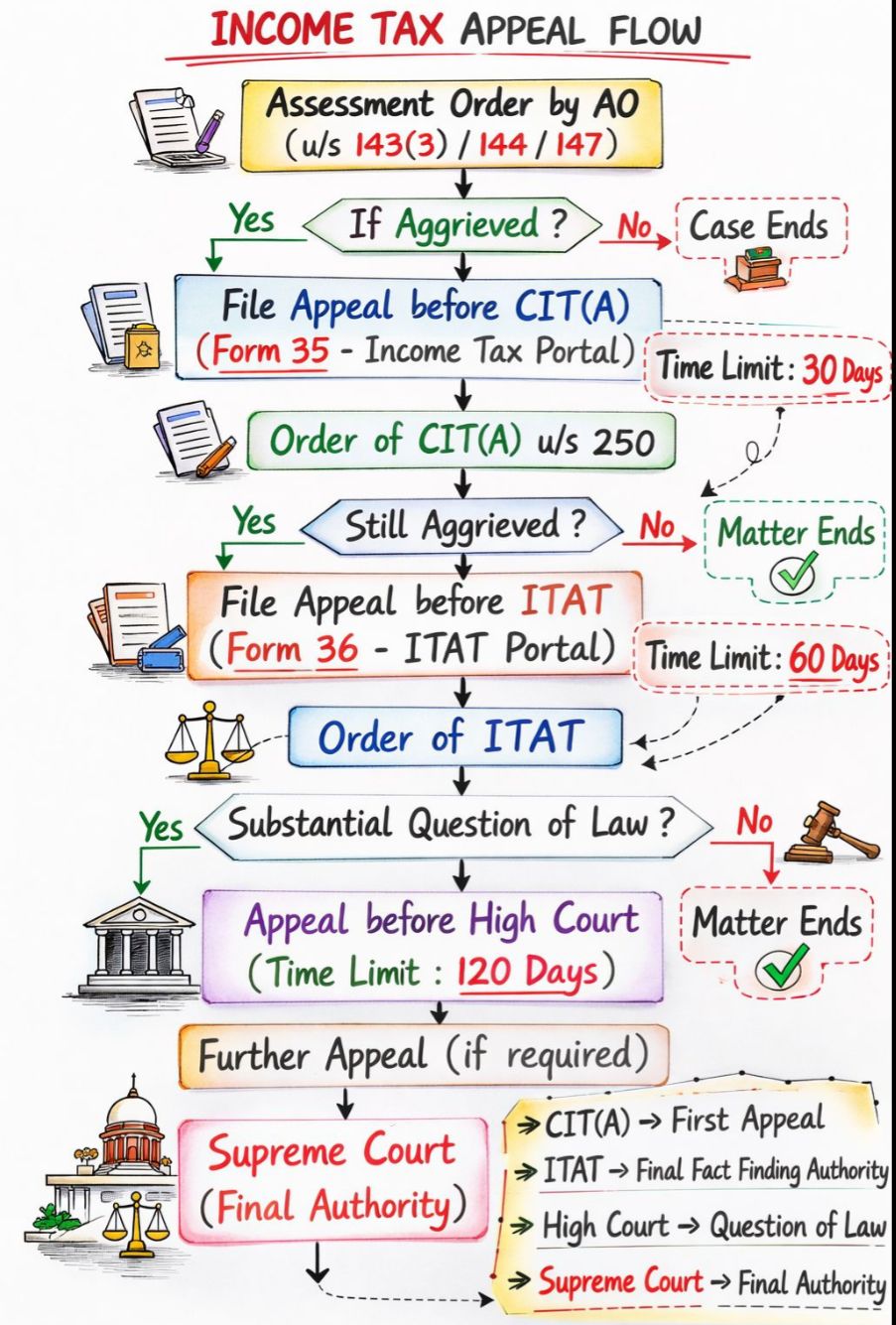

Appeals To Commissioner(Appeals) [Section 246a To 249]:-

Appeals To Commissioners (Appeals) Appealable orders (Illustrative): Scrutiny assessment order—Best Judgment assessment order— Reassessment order— Rectification order enhancing assessee’s liability—Appeal against intimation passed under section 200A— Tonnage tax order— Appeal to CIT(A) within 30 days of Date of payment of tax, where appeal is in respect of TDS—under section 195 Date of service of notice of demand relating to assessment or— penalty Date on which intimation of order sought to be appealed against—is served.

- Appeals To Commissioners (Appeals):- Time extended if sufficient cause proven Appeal to be filed in prescribed form and manner CIT(A) fixes a day and place for hearing the appeal, and notice of the same is given to the appellant and the assessing officer whose order is being appealed against During the course of the hearing, CIT(A) may entertain additional ground/evidence raised by the appellant in seeking modification of the assessment order passed by the assessing officer CIT(A)’s order disposing of the appeal is in writing and states decision and reasons supporting the same CIT(A) has powers to confirm, reduce, enhance or annul the assessment Where possible, CIT(A) to dispose within 1 year from the end of the financial year in which appeal was filed.

- Appeals To Tribunal [Section 252 To 255]:-

Appeals To Tribunal Should be filed within 60 days of the date on which the order sought to be appealed against is communicated Memorandum of cross-objections – within 30 days of receipt of notice that an appeal has been preferred to the ITAT Time extended if sufficient cause proven To be filed in prescribed form and manner Additional ground/ evidence can be raised for the first time before the ITAT. In such a case opportunity of being heard should be given to the assessing officer After hearing both parties, the ITAT passes an order as it thinks fit and communicates the same to the assessee and the Commissioner Where possible, ITAT to dispose within 4 years from the end of the financial year in which appeal was filed In case order of stay is made, appeal to be disposed within 180 days of stay order; else, stay stands vacate.

- Appeals To Tribunal Mistakes Apparent From Record :- Order of ITAT can be amended within 4 years from date of ITAT order [Section 254(2)] if it is brought to the notice by the assessee or the assessing officer Final fact finding authority Binding nature

- Appeal To High Court [Section 260a]:-

Appeals To High Court Right exercisable u/s 260A Preferred against ITAT’s order Only for a case involving a “substantial question of law” Should be filled within 120 days of receipt of ITAT’ sorder Can also be filed by the Tax department Rules framed for court proceedings and conduct has to be observed

- Appeals to Supreme Court Right Exercisable u/s 261:- Preferred against High Court’s order Only for a case involving a “substantial question of law” Should be filled within 60 days of receipt of High Court’s order Can also be filed by the Tax department Rules framed for court proceedings and conduct has to be observed.

Time For Filing Return Of Income [Sec. 139 (1)] Different Situations Due Date for filing Return:

- Where the assessee is a company:- 30th September

- Where the assessee is person other than a company :-

- In case where accounts of the assessee are required to be audited under any law:- 30th September

- Where the assessee is “working partner” in a firm whose accounts are required to be audited under any law:- 30th September

- In any other case:- 31st July

Hope the information will assist you in your Professional endeavors. For query or help, contact: info@caindelhiindia.com or call at 9555 555 480

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.