All about TDS Compliance Reform Effective from 1.04.2026

Table of Contents

Understanding about Tax Deducted at Source Compliance Reform Effective from 1st April 2026

The TDS (Tax Deducted at Source) framework has undergone a structural overhaul with the introduction of the Income Tax Act, 2025 and Income Tax Rules, 2026. This is not just a change in sections; it is a shift towards real-time, technology-driven tax compliance.

What Has Changed? (Big Picture)

India’s tax reporting framework is poised for a significant transformation with the proposed implementation of the Income‑tax Act, 2025, effective from FY 2026‑27. The following are the big picture of change:

- Transition from old law → new Act with renumbered sections & simplified structure

- Focus on automation, transparency, and reduced disputes

- Movement from year-end adjustments → real-time TDS accuracy

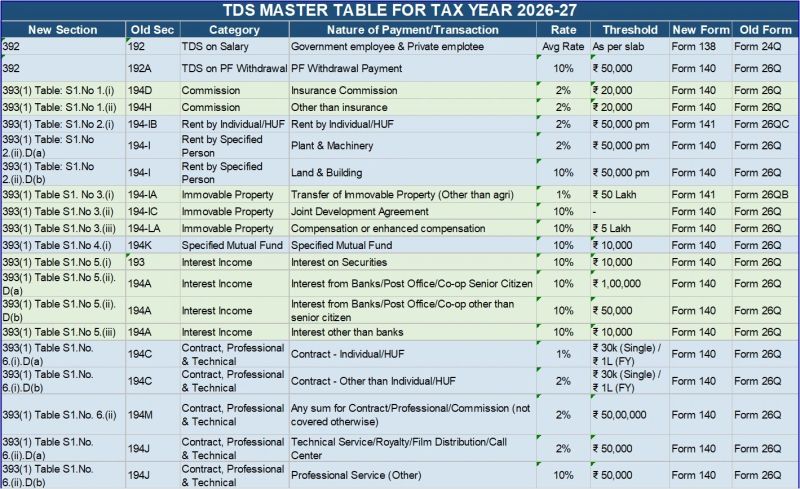

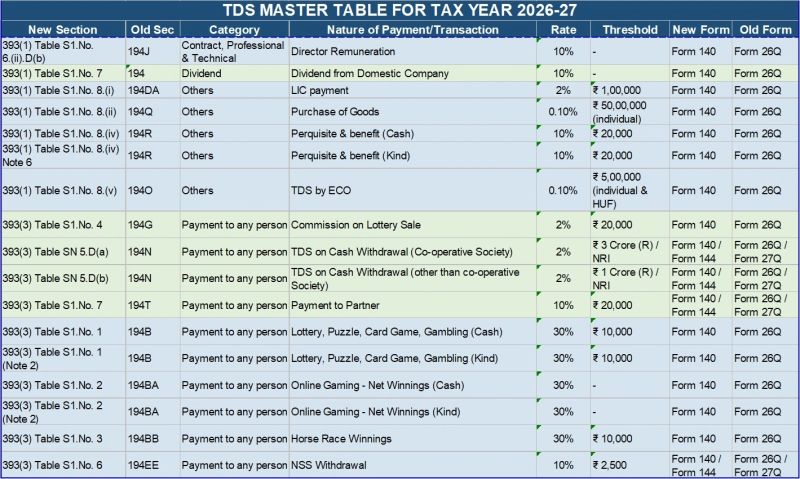

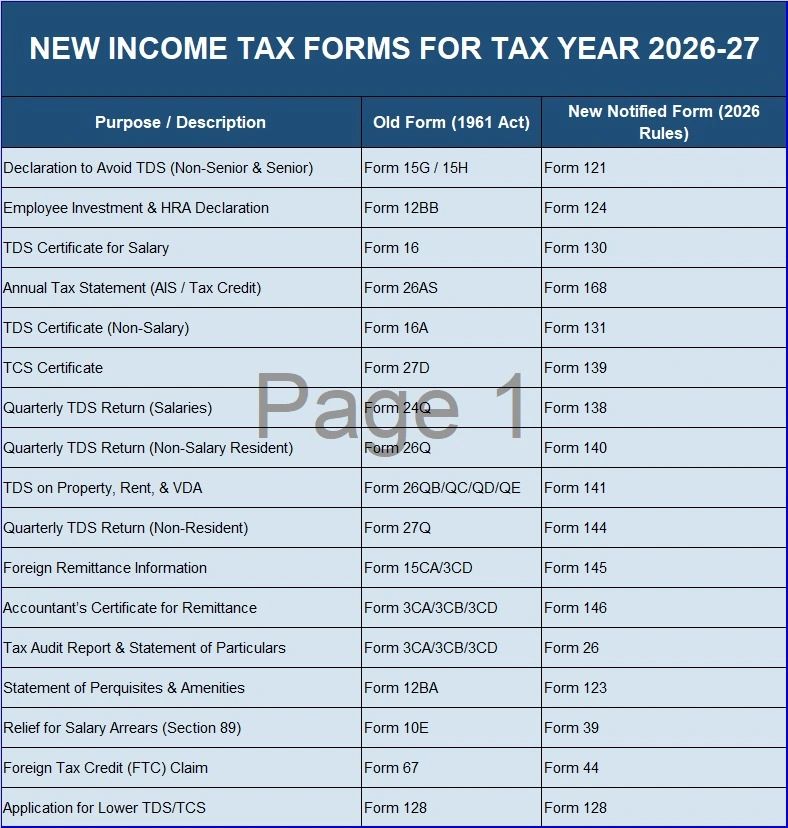

Below are the key Tax Deducted at Source-related changes every tax professional, employer, and business should be aware of New TDS Return Forms: Under the new Act, existing Tax Deducted at Source return forms are proposed to be renumbered as follows:

- Salary Tax Deducted at Source Return: Form 24Q ➝ Form 138

- Non‑Salary Tax Deducted at Source Return: Form 26Q ➝ Form 140

- Non‑Resident Tax Deducted at Source Return: Form 27Q ➝ Form 144

Practical Impact on TDS Tax Compliance Reform

Practical Impact on Tax Deducted at Source Compliance Reform on Taxpayers & Businesses are as follows:

- Increased compliance responsibility on deductees

- Higher penalties for incorrect / delayed Tax Deducted at Source

- Greater data matching with AIS / system analytics

- Impact on cash flows & take-home salary

New Tax Deducted at Source Certificates:

Corresponding changes are also proposed in Tax Deducted at Source certificates:

- Form 16 ➝ Form 130

- Form 16A ➝ Form 131

A detailed section‑wise comparison of Tax Deducted at Source rates (Old vs New provisions) and Forms (existing vs proposed) is provided in the reference images. This Means for Taxpayers & organizations a streamlined and modernized compliance framework, Improved reporting clarity and standardization and Alignment with the simplified structure of the new Act

Key TDS Rate Comparison—Tax Deducted at Source rates (Old vs New provisions)

| Nature of Payment | Old Provision (1961 Act) | TDS Rate | New Provision (2025 Act) | TDS Rate | Key Change |

| Salary | Sec 192 | Slab rates | Corresponding section | Slab rates | No change (better reporting) |

| Interest (other than securities) | Sec 194A | 10% | Rationalised section | 10% | Thresholds streamlined |

| Contractor Payments | Sec 194C | 1% / 2% | Simplified contractor provision | 1% / 2% | Classification clarity |

| Professional Fees | Sec 194J | 10% | Merged / simplified provision | 10% | Reduced disputes |

| Commission / Brokerage | Sec 194H | 5% | Rationalised section | 5% | Structural simplification |

| Rent (Land/Building) | Sec 194I | 10% | Simplified rent provision | 10% | Uniformity improved |

| Rent (Plant & Machinery) | Sec 194I | 2% | Same concept retained | 2% | No major change |

| Purchase of Goods | Sec 194Q | 0.1% | Continued with simplification | 0.1% | Compliance ease |

| Sale of Property | Sec 194IA | 1% | PAN-based simplified system | 1% | Process simplified |

| Cash Withdrawal | Sec 194N | 2% / 5% | Continued | 2% / 5% | Monitoring strengthened |

| Dividend | Sec 194 | 10% | Rationalised | 10% | No rate change |

Action Point of Key Tax Compliance Reform

Organizations should proactively update their payroll systems, compliance software, SOPs, and documentation to ensure a smooth transition once the new provisions are notified. These changes are based on the proposed Income‑tax Act, 2025 and will be applicable subject to final enactment and official notifications.

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.