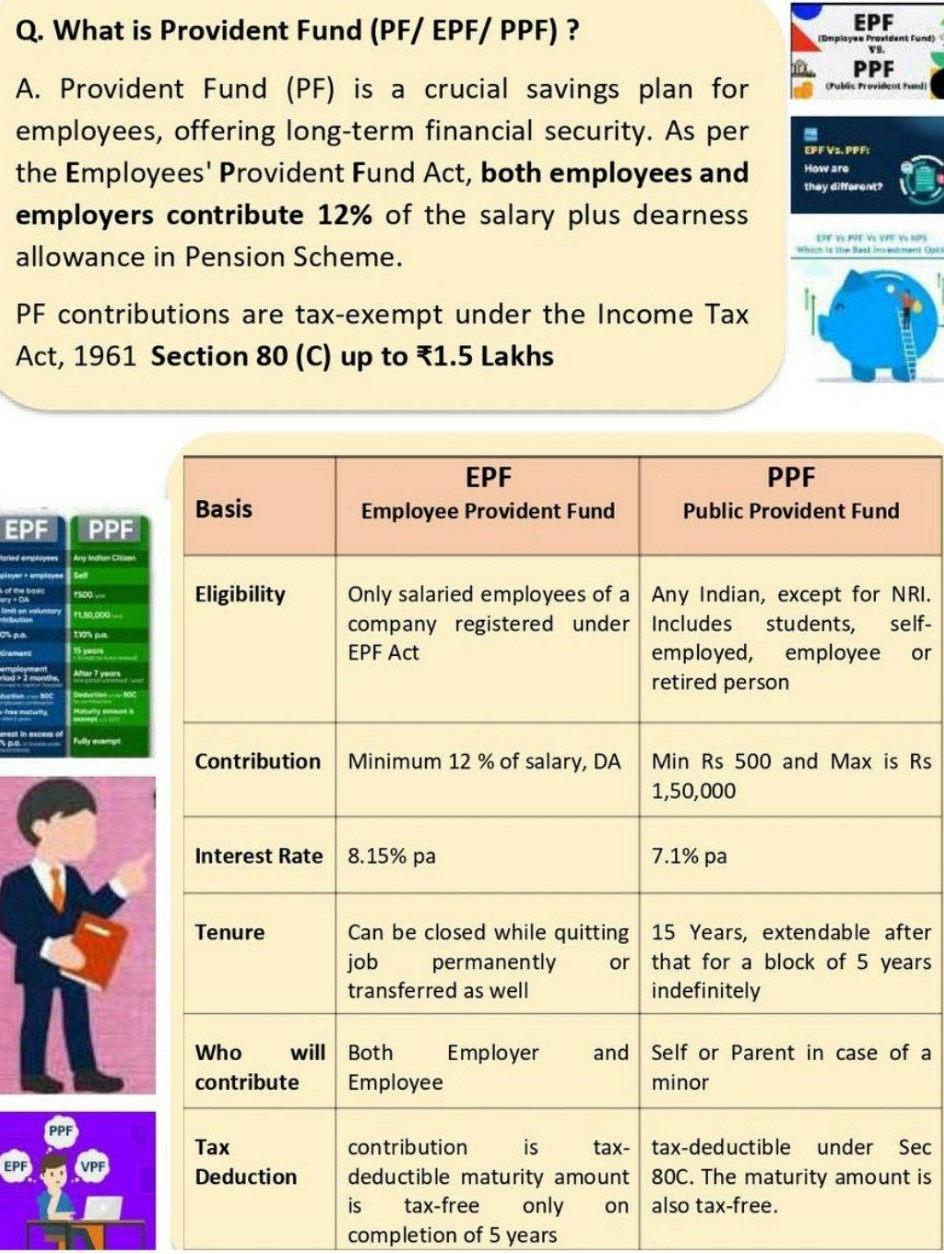

All About National Savings Certificate (NSC) & PPF

What are the differences and similarities between the National Savings Certificate (NSC) and PPF?

| National Savings Certificate (NSC) | Public Provident Fund (PPF) |

| Interest Paid: 8%, compounded half-yearly | Interest Paid: 8%, compounded annually |

| No monthly/yearly payments | No monthly/yearly payments |

| Minimum investment: Rs 100 Maximum investment: No Limit | Minimum investment: Rs 500 (required annually)Maximum investment: Rs 70,000 |

| Duration of investment: 6 years | Duration of investment: 15 years |

| Can be used as a security for mortgage and other purposes | Cannot be used for such purposes |

| Tax benefit under Section 80 ‘C’ available.Maximum limit: Rs 100,000 | Tax benefit under Section 80 ‘C’ available.Maximum limit: Rs 70,000 (limit of the investment in PPF) |

| Good medium-term investment option | Good long-term investment option |

| Interest if fully Taxable | Interest is fully Exempt |

Do consider opening a PPF account if you do not have one. You can put in as little as Rs 500 a year to keep it going.

How much interest do I earn by investing in PPF scheme?

Since the year 2003-04, the rate of interest on PPF saving scheme is 8% p.a. compounded annually.

How does PPF stand vis-à-vis NSC?

Investing in PPF certainly scores over investing in NSC. For more details see: Which is better between the PPF and the NSC?

How can I make the most of my PPF account? What are the considerations to be kept in mind while investing in PPF?

There are certain tips and tricks you can use to make the most of your PPF account such as opening PPF account at the earliest, investing on regular basis rather than waiting till the end of the year, and investing before 5th of every month. For more of such tips see: 10 Practical Tips for investing in PPF.

How do I calculate the interest on PPF?

Use PPF interest Calculator to calculate your PPF interest and maturity value.

Why should I invest in PPF?

You must invest in a PPF because it is the best debt option after PF:-

- 8% p.a. tax-free returns in addition to section 80C deduction on deposits.

- Option to invest regularly for long term and can be continued indefinitely even after maturity.

- Highest safety as it is a government- backed saving scheme.

- Can’t be attached by any court.

- Flexibility to invest varying amounts. You’re allowed to deposit in lump sum or in installments. Further, you can vary amount of installments as per your convenience and it is not necessary to deposit every month.

What is the maximum ceiling on deposit in PPF?

As per Section 80C of Income Tax –> no ceiling

As per PPF Rules –>Rs 70,000

How many numbers of times can I make deposits in PPF account during a year?

You can deposit money in your PPF account either in lump sum or in installments which need not be of same amount. However, total number of deposits during a financial year can’t exceed twelve.

Am I required to deposit money in my PPF account every year? What if I don’t?

Yes, a minimum deposit of Rs 500 is required every year. If you don’t, then your account will become inoperative.

What are the tax benefits available on PPF scheme?

There are two benefits: first when you deposit money in your PPF account, you get entitled for tax deduction u/s 80C and as a result your taxable income stands reduced to that extent. The second tax benefit is that the interest earned on your PPF deposits is completely exempt from tax.

Is it possible to avail Rs 1 lakh deduction under section 80C though we’re allowed to deposit maximum of Rs 70,000 under PPF rules?

Actually under the IT Act, there is no limit and even under PPF rules Rs 70,000 limit is meant for self a/c and minor a/c. It doesn’t include the contribution to the a/c of spouse and major children.

In other words, as per PPF rules, the total deposit in your own account and in the account of your minor child can’t exceed Rs 70,000 in a FY. But PPF rules doesn’t bar you from making additional deposit beyond the limit of Rs 70,000 in the account of your spouse or your major children and accordingly you can claim Rs 1 lakh tax deduction u/s 80C of IT Act.

Who can claim section 80C benefit: the person in whose name the PPF a/c stands or the person who deposits money in the PPF account?

The person who makes the contribution to PPF is entitled for tax benefit. For example, if you invest your money in the PPF account of your spouse, you’ll be entitled to claim section 80C deduction instead of your spouse.

Can I contribute to the PPF account of my parent’s and claim section 80C tax benefit?

No, you’re not allowed to claim tax benefits on the contribution made by you in the PPF account of your mother or father.

Is it possible to avail section 80C benefit without making deposits in the PPF account?

Yes, but only from 7th financial year onwards. The trick is to make partial withdrawals (as mentioned below) and redeposit it in your PPF account.

Loan Against PPF

-

Eligibility: After 1 full financial year from account opening

-

Can be availed: Before completion of 5 full financial years

-

Loan Limit: 25% of balance at end of 2nd FY preceding loan application

Partial Withdrawals

-

Eligibility: After 5 full financial years from account opening

-

Withdrawal Limit: Lower of 50% of Balance at end of 4th FY preceding withdrawal year, Balance at end of preceding FY

Hope the information will assist you in your Professional endeavors. For query or help, contact: info@caindelhiindia.com or call at 9555 555 480

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.