All about the reverse charge mechanism on property rent

Table of Contents

All about the reverse charge mechanism on property rent

goods and service tax under the Reverse Charge Mechanism on property rent, especially after recent goods and service tax notifications affecting residential and commercial properties. This blog is essentially a compliance guide for determining who pays GST on rent and when the Reverse Charge Mechanism becomes applicable under goods and service tax law.

What is the reverse charge mechanism?

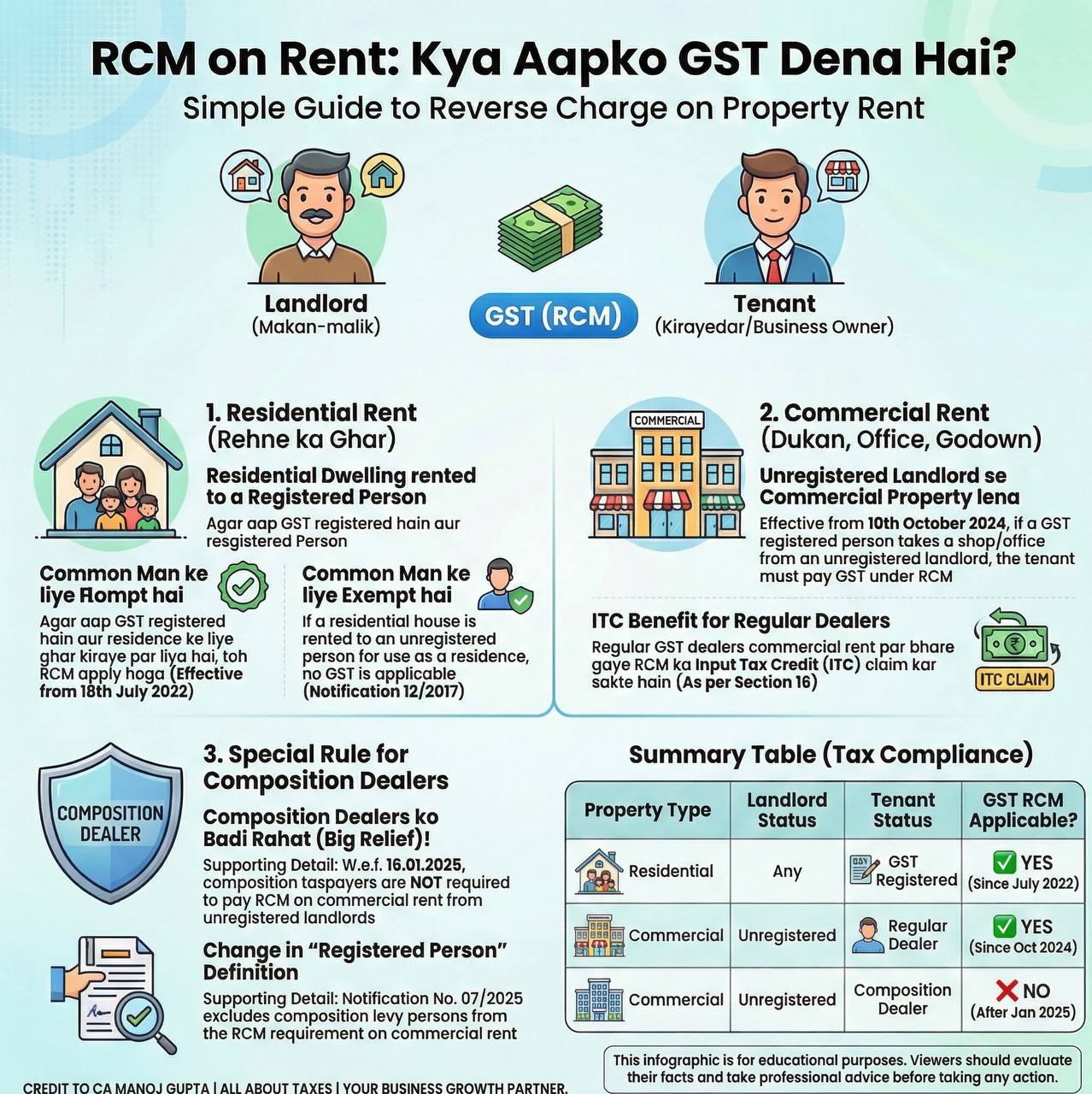

Normally, the supplier (landlord) collects and pays goods and service tax to the government. Under RCM, the responsibility shifts to the recipient (tenant).

- Normal GST: Landlord → Collects goods and service tax → Deposits to Government

- Reverse Charge Mechanism: Tenant → Pays GST Directly → Government

| Situation | GST Applicable? |

|---|---|

| A salaried individual rents a house for residence | No |

| An unregistered individual rents a house | No |

| Unregistered landlord to unregistered tenant | No |

| The company rents residential dwelling for employee accommodation | No |

| goods and service tax-registered business takes residential house on rent in its own capacity | Yes, under the reverse charge mechanism. |

| GST-registered professional takes house on rent for business use | Yes, under the reverse charge mechanism. |

Residential Property Rent

Case 1: Residential House Rented by a GST Registered Person

- GST Implication: Even though the property is residential and used for residence, if the tenant is a registered person, goods and services tax under RCM applies.

- Effective Date: 18 July 2022 This provision arose through GST notifications bringing residential dwellings rented to a registered person under RCM.

Case 2: Residential House Rented by an Unregistered Individual:

- GST Treatment: Fully Exempt, No goods and service tax, No RCM. No compliance.

- Legal Basis: A residential dwelling rented for use as residence remains exempt under goods and service tax for unregistered people.

Commercial Property Rent

- Earlier Position: Commercial property rented by an unregistered landlord generally did not attract GST under RCM.

- New Position: Effective 10 October 2024: If Landlord is Unregistered AND Tenant is GST Registered AND Property is Commercial Then goods and service tax is payable by tenant under RCM.

- Commercial Properties Covered: Shops, Offices, Godowns, and Commercial Establishments.

Input Tax Credit Benefit Available

- Input Tax Credit: A regular GST taxpayer paying GST under RCM can generally claim Input Tax Credit, subject to Business use, Payment of GST, Conditions under Section 16 and No blocked credit restrictions

- Special Relief for Composition Dealers: The most important part of the infographic is the relief given to composition taxpayers.

- Before Relief: Composition dealers were also falling within the scope of registered people. This created an additional burden.

- After Notification No. 07/2025: Effective 16 January 2025: Composition taxpayers are excluded from RCM on commercial rent taken from unregistered landlords. Result

- No GST under RCM

- No need to pay 18% GST

- This significantly reduces compliance burden.

Change in Meaning of “Registered Person”: Notification No. 07/2025 effectively excludes composition taxpayers from the definition for this RCM requirement. Practical Result: Two categories emerge:

- Regular goods and service tax Dealers: The reverse charge mechanism applies.

- Composition Dealers: Reverse Charge Mechanism does not apply (for commercial rent from unregistered landlords).

GST ON Rent – Exemption from Payment of GST

Many people believe that goods and service tax is payable on every house’s rent. This is incorrect. goods and service tax under Reverse Charge Mechanism generally becomes relevant only when a GST-registered business or professional takes a residential dwelling on rent in its registered-business capacity. In the following case, no GST is payable when:

- The tenant is a salaried individual.

- Tenant is not Goods and Services Tax registered.

- Both landlord and tenant are unregistered.

- A company rents residential accommodation for its employees.

Therefore, the common taxpayer, salaried employee, and ordinary residential tenant generally remain outside the goods and service tax liability on house rent.

Summary of reverse charge mechanism on property rent

| Property Type | Landlord | Tenant | RCM |

| Residential Property | Any | goods and service tax Registered Person | Yes |

| Residential Property | Any | Unregistered Person | No |

| Commercial Property | Unregistered | Regular GST Dealer | Yes |

| Commercial Property | Registered | Any Registered Tenant | Normal GST applies to the landlord. |

| Commercial Property | Unregistered | Composition Dealer | No (after Jan 2025) |

Key Takeaways on the Reverse Charge Mechanism on property rent

- Residential Rent: Residential dwelling to unregistered person → Exempt. And residential dwelling to a GST-registered person → Reverse Charge Mechanism applicable from 18-07-2022.

- Commercial Rent: Commercial property from unregistered landlord to regular GST dealer → Reverse Charge Mechanism applicable from 10-10-2024.

- Composition Dealer Relief: Composition taxpayers are not required to pay RCM on commercial rent from unregistered landlords w.e.f. 16-01-2025.

- ITC: Regular taxpayers can claim an input tax credit of goods and services tax paid under the reverse charge mechanism, subject to normal GST conditions.

- For a residential dwelling, the moment the tenant is a GST-registered person, goods and service tax becomes payable under the Reverse Charge Mechanism, irrespective of

-

- Whether the landlord is registered or unregistered;

- new question—Whether the property is used for residence or business purposes; and

- Whether the landlord charges GST or not.

- Only a residential dwelling rented to an unregistered person for use as a residence remains exempt from GST.

Quick Formula on Reverse Charge Mechanism on Rent

- Residential Property + Registered Tenant = RCM (Reverse Charge Mechanism)

- Commercial Property + Unregistered Landlord + Regular GST Dealer = RCM (Reverse Charge Mechanism)

- Commercial Property + Unregistered Landlord + Composition Dealer = No RCM (from Jan 2025)

Basic Key Principles for gst on rent

| Factor | Relevant for GST? |

|---|---|

| Is the Tenant goods and service tax Registered? | Most Important Factor |

| Is the Landlord GST Registered? | Not Relevant for Reverse Charge Mechanism |

| Residential Use or Commercial Use by goods and service tax Registered Tenant? | Not Relevant |

| Residential Dwelling Property? | Relevant |

| Unregistered Tenant? | Exemption available for residential use |

| Situation | GST Treatment |

|---|---|

| Residential Dwelling + Unregistered Tenant + Residential Use | Exempt |

| Residential Dwelling + Unregistered Tenant + Commercial Use | Taxable under Forward Charge |

| Residential Dwelling + GST Registered Tenant + Residential Use | Taxable under Reverse Charge Mechanism |

| Residential Dwelling + GST Registered Tenant + Commercial Use | Taxable under Reverse Charge Mechanism |

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.