All about VPF (Voluntary Provident Fund)

Table of Contents

Lesser-Known Facts About VPF (Voluntary Provident Fund)

Key Features of VPF:

- Extension of EPF, Not a Separate Scheme : Voluntary Provident Fund is not a separate fund — it is an extension of the Employee Provident Fund (EPF). Only salaried employees contributing to EPF can opt for Voluntary Provident Fund. Contributing to a VPF account is not mandatory; it’s entirely at the discretion of the employee. Unlike EPF, employees can contribute up to 100% of their Basic Salary + Dearness Allowance to the VPF account.

-

Government-Declared Interest Rate: The Government of India revises the VPF interest rate at the beginning of each financial year. It may increase or decrease based on macroeconomic factors.

-

Transferable Between Employers: VPF balances can be transferred from a previous employer to the current employer, ensuring continuity of the account.

- Full Withdrawal at Maturity: The total accumulated amount (contributions + interest) can be withdrawn at the time of resignation or retirement.

- No Automatic Enrollment : You must request in writing to your employer to start VPF. It can typically only be modified at the start of a financial year, depending on company policy.

-

Nominee Benefits: In the unfortunate event of the account holder’s demise, the nominee/legal heir receives the entire accumulated corpus.

- Visible in EPFO Passbook: VPF contributions and interest appear in your regular EPF passbook, making tracking easy.

- 🇮🇳 Safe & Government-Backed: Since EPF/VPF is managed by the EPFO under the Ministry of Labour, it is considered one of the safest investment options.

- Can Be Stopped or Changed (But Limited Window): Once opted in, you may not be able to alter the VPF contribution mid-year, unless the employer’s policy allows it. Some companies lock the contribution amount for the year.

Voluntary Provident Fund (VPF) – Rules & Regulations

- Tax Benefits (EEE Regime): VPF enjoys Exempt-Exempt-Exempt tax treatment: Contribution: Deductible under Section 80C (within INR 1.5 lakh limit). Interest: Tax-free (up to a limit, see below). Maturity: Fully tax-free if criteria are met.

- Tax on Interest for High-Income Earners: From FY 2021–22 onwards, if your annual employee contribution to EPF + VPF exceeds INR 2.5 lakh, interest earned on the excess is taxable. If there is no employer contribution (e.g., government employees with GPF), the threshold is INR 5 lakh.

- Account Opening Window: VPF accounts can be opened anytime during the financial year.

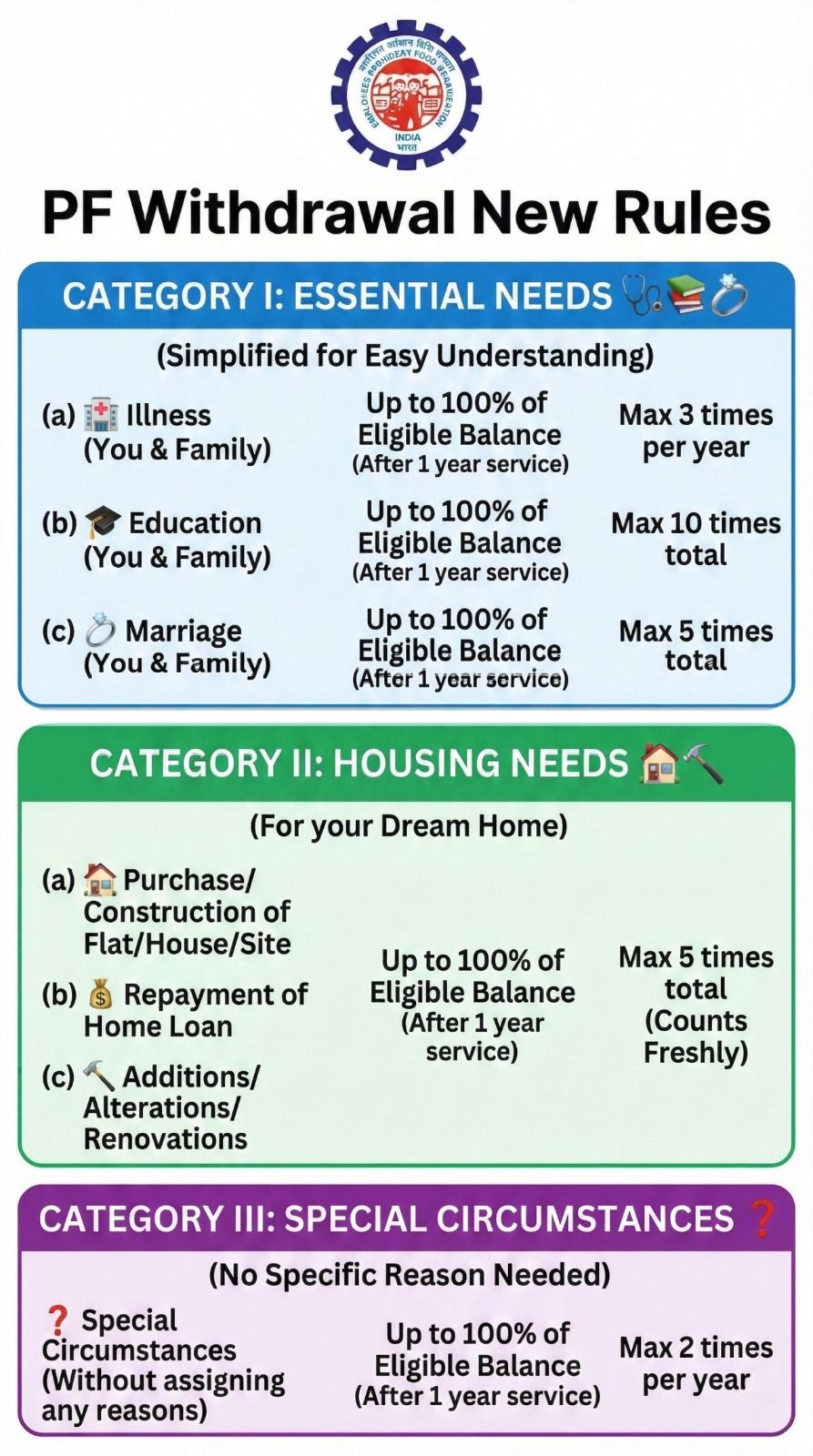

- Lock-in Period and Withdrawal Rules : Partial withdrawals are allowed in the form of loans. Premature withdrawal may attract tax liability on the interest earne, VPF has a 5-year lock-in for tax-free withdrawal. Premature withdrawals are allowed for Marriage Medical emergencies House purchase/construction Higher education, however, tax benefits may be reversed if withdrawn before 5 years. Once opted in, contributions to the VPF account cannot be discontinued for 5 years (to retain tax-free status).

- Interest Rate Same as EPF : VPF earns the same interest rate as EPF, which is decided by the EPFO every year (8.15% for FY 2023–24). Returns are compounded annually, making it more attractive for long-term, risk-averse investors.

-

You can contribute up to 100% of Basic + DA : Only salaried employees covered under the Employees’ Provident Fund Organisation (EPFO) are eligible. Individuals in the unorganised sector are not allowed to open a VPF account. You can contribute up to 100% of your basic salary and Dearness Allowance voluntarily (beyond the mandatory 12%). However, your employer is not obligated to match the extra contribution.

What is the difference between VPF and EPF?

| Feature | EPF | VPF |

|---|---|---|

| Contribution | Mandatory 12% of Basic + DA | Voluntary, up to 100% of Basic + DA |

| Employer Contribution | Mandatory | Not applicable |

| Flexibility | Fixed statutory contribution | Completely flexible (voluntary) |

| Tax Benefits | Under Section 80C (EEE status) | Under Section 80C (EEE status) |

EPFO Applicability under the Code on Social Security, 2020—Explained Clearly

PF compliance is not optional—it’s foundational. For HR and Payroll professionals, a correct understanding of wages, ceilings, and attendance-based calculations is critical to avoid errors, disputes, and penalties. Below is a simple breakdown based on the new wage definition under the Code on Social Security, 2020

PF (Provident Fund)—Key Concept Under the New Code

Rule: At least 50% of total remuneration must be treated as “wages.” Any allowance exceeding this limit is added back for PF calculation. Allowance-heavy salary structures will increase PF liability. PF contribution depends on earned wages, not just salary structure. Attendance directly impacts PF when wages fall below the ceiling. Accurate structuring today avoids future EPFO litigation. EPFO compliances require timely filing, accurate employee records, and adherence to due dates to avoid penalties.

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.