CBDT Notifies Cost Inflation Index (CII) for TY 2026-27

Table of Contents

CBDT Notifies Cost Inflation Index for TY 2026-27: What It Means for Property Owners and Taxpayers

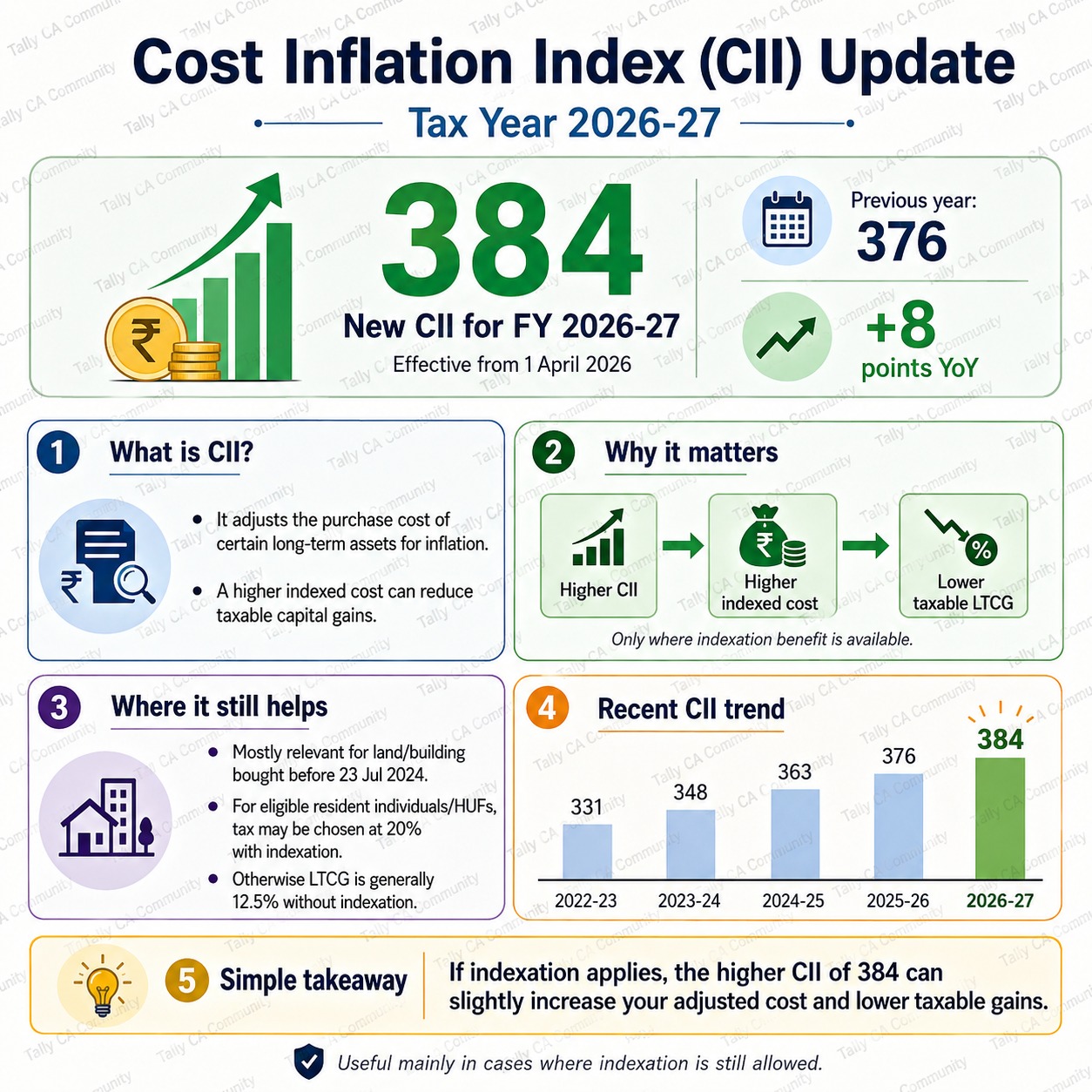

The Central Board of Direct Taxes (CBDT) has officially notified the Cost Inflation Index for Tax Year (TY) 2026-27 at 384, effective from 1 April 2026. This marks an increase from the previous year’s CII of 376, providing taxpayers with a higher inflation adjustment while computing long-term capital gains, wherever indexation benefits continue to be available.

While the increase may appear modest, it can have a meaningful impact on the tax liability arising from the sale of eligible capital assets, particularly immovable properties acquired before the recent tax law changes.

New Cost Inflation Index for TY 2026-27

| Tax Year | Cost Inflation Index (CII) |

|---|---|

| 2025-26 | 376 |

| 2026-27 | 384 |

The increase of 8 points reflects inflationary adjustments recognized under the tax law and allows eligible taxpayers to increase the indexed cost of acquisition when calculating long-term capital gains.

What is the Cost Inflation Index?

The Cost Inflation Index is a measure notified annually by the CBDT to account for inflation in the value of capital assets over time. Indexation adjusts the original purchase cost of an asset to reflect inflation, ensuring taxpayers are taxed only on the real appreciation in value rather than gains arising merely from rising prices. The indexed cost is calculated using the following formula:

Indexed Cost of Acquisition = Cost of Acquisition × (Cost Inflation Index of Year of Transfer ÷ Cost Inflation Index of Year of Purchase)

A higher CII results in a higher indexed cost, which in turn reduces taxable long-term capital gains.

Why Does the Increase to 384 Matter?

The rise in the cost inflation index from 376 to 384 means that taxpayers selling eligible assets during TY 2026-27 can claim a slightly higher inflation-adjusted cost. This can lead to Higher indexed cost of acquisition, Lower taxable long-term capital gains, and potential reduction in overall tax liability. Although the annual increase is relatively small, the cumulative impact can be substantial for assets held over several years, particularly real estate.

Relevance Under the Income-tax Act, 2025

Following the changes introduced in capital gains taxation, indexation is no longer universally available for all long-term capital assets. However, it continues to hold significance in specific cases.

The revised cost inflation index is particularly relevant for Land and buildings acquired before 23 July 2024, Cases where indexation benefits remain available under the Income Tax Act, 2025, and resident individuals and HUFs eligible to choose between alternative LTCG tax regimes. For eligible property transactions, taxpayers may still be able to avail themselves of indexation benefits and reduce their taxable gains.

Choice Between 20% with Indexation and 12.5% Without Indexation

A significant relief available to eligible resident individuals and Hindu Undivided Families is the option to choose:

- Option 1: 20% Tax with Indexation: Compute capital gains after applying indexation benefit. and Tax payable at 20%.

- Option 2: 12.5% Tax Without Indexation: No inflation adjustment available. and Tax payable at 12.5%.

The optimal choice depends on factors such as Year of acquisition, original purchase cost, inflation-adjusted cost, sale consideration, and Holding period. For properties held for a long duration, indexation may significantly reduce the taxable gain, making the 20% regime more beneficial despite the higher tax rate.

Illustrative Impact of cost inflation index

Consider a property purchased several years ago for INR 50 lakh and sold in TY 2026-27. With the revised cost inflation index of 384, the indexed cost may increase compared to calculations using the previous year’s index. The higher adjusted cost reduces taxable capital gains, which may ultimately lead to lower tax outgo under the indexation regime.

Therefore, taxpayers should carefully compare Tax under 20% with indexation and Tax under 12.5% without indexation before finalizing their capital gains computation.

Trend in Recent cost inflation index

The Cost Inflation Index has steadily increased over the years:

| Tax Year | cost inflation index |

|---|---|

| 2022-23 | 331 |

| 2023-24 | 348 |

| 2024-25 | 363 |

| 2025-26 | 376 |

| 2026-27 | 384 |

The upward trend reflects continued inflation adjustments and reinforces the importance of considering indexation benefits wherever available.

Key Takeaway for Tax Professionals

The notification of the cost inflation index at 384 for TY 2026-27 may appear to be a routine annual update, but it can have a direct impact on LTCG computations for eligible taxpayers. Taxpayers should:

- Use the revised cost inflation index of 384 for transfers taking place in TY 2026-27.

- Recompute indexed cost for eligible capital assets.

- Compare the tax impact under both LTCG regimes where the option is available.

- Advise clients selling legacy real estate holdings to evaluate whether the 20% tax with indexation or 12.5% tax without indexation results in a lower overall tax burden.

The new cost inflation index of 384 reinforces the importance of accurate capital gains planning. For taxpayers selling eligible properties acquired before 23 July 2024, a simple comparison between the available tax computation methods could translate into significant tax savings. As always, a case-specific evaluation remains essential to identify the most beneficial tax treatment.

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.