Crypto Futures Taxation: Business Income or 30% VDA Tax?

Table of Contents

Taxation of Crypto Derivatives in India

- Crypto derivatives are financial contracts whose value is linked to cryptocurrencies. They allow traders to profit from price movements without owning the actual crypto assets.

- Common derivatives include crypto futures, crypto options, and perpetual futures contracts. These instruments are used for speculation, hedging risk, arbitrage, and leveraged trading

-

Taxation of Crypto Options:

- Cost basis is the original purchase price of an asset and is used to calculate gains or losses. Formula: Capital Gain/Loss = Sale Price − Cost Basis

- Crypto options give the buyer the right, but not the obligation, to buy or sell crypto currency at a predetermined price before a specified date. If Options are Capital Assets

- Gains are taxed as capital gains.

- Long-term capital gains (LTCG): Taxed as per LTCG provisions applicable.

- Short-term capital gains (STCG): Taxed at the individual’s income tax slab rate.

- Gains or losses are treated as business income/profit and loss.

- Taxed according to the individual’s applicable income tax slab rate.

-

Crypto Futures Trading:

-

- Hedging – Protect against adverse price movements.

- Arbitrage – Profit from price differences across markets.

- Leverage – Increase exposure using borrowed funds (higher risk and reward).

-

- This is the view adopted by many professionals when contracts are cash settled; No actual crypto is delivered, and settlement is in INR. And Trader only receives profit/loss difference. Under this interpretation: Futures Contract ≠ Crypto Asset

- The trader is not buying or selling Bitcoin. The trader is entering into a contract whose value depends upon Bitcoin price movements. Hence

- Underlying asset = Crypto

- Instrument traded = Derivative Contract

- Accordingly, professionals argue that income should be assessed as business income.

-

Perpetual Crypto Contracts

|

Feature

|

Crypto Futures

|

Perpetual Futures

|

|

Expiry Date

|

Yes

|

No

|

|

Settlement

|

On expiry

|

No settlement date

|

|

Price Basis

|

Future expected price

|

Tracks spot price closely

|

|

Holding Period

|

Limited

|

Indefinite

|

|

Funding Rate

|

Not applicable

|

Applicable

|

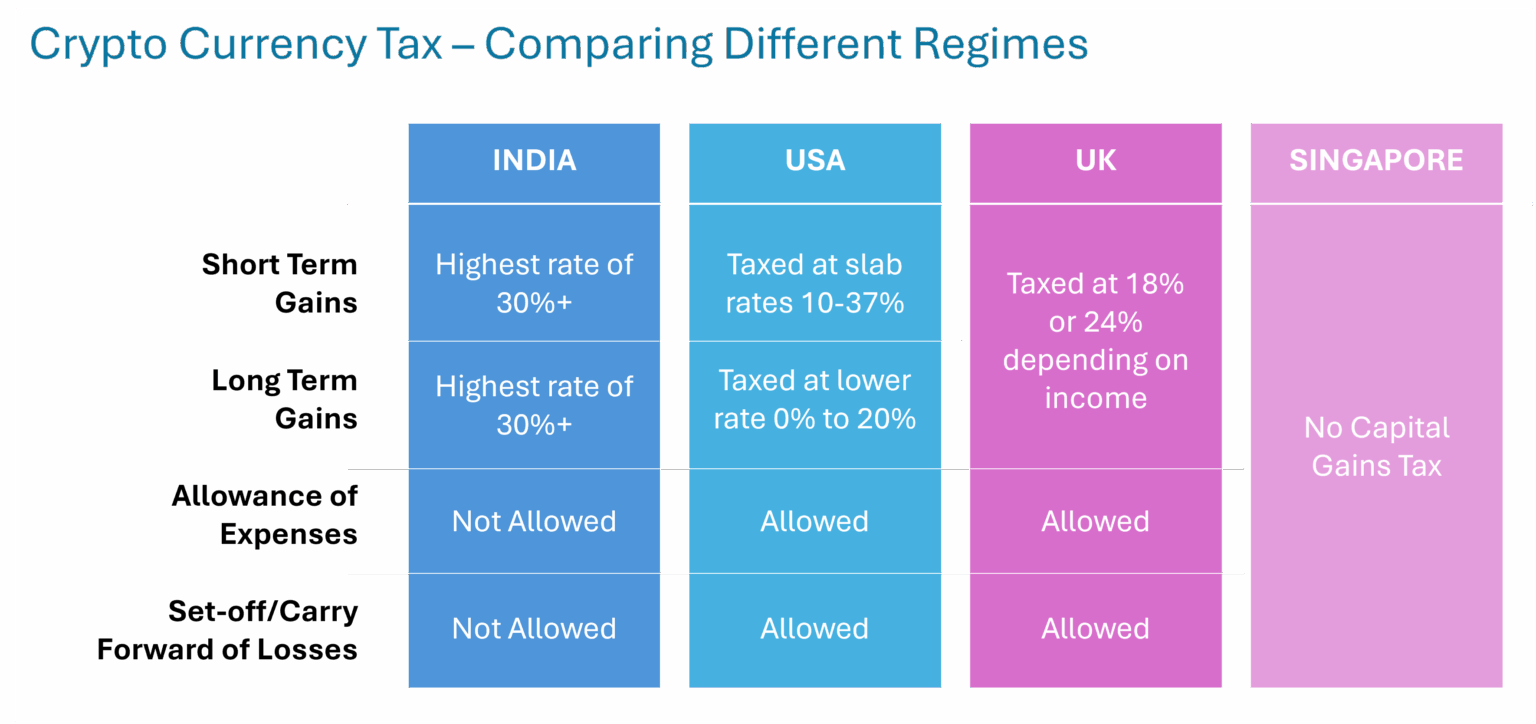

Taxation of Crypto Derivatives in the Different Countries

-

Transfer of a Virtual Digital Asset (VDA):

Section 115BBH applies if there is a direct transfer of a Virtual Digital Asset (VDA):

-

-

- Taxation Under Section 115BBH (Conservative Department View). In case of a derivative / speculative business transaction settled without actual transfer of crypto: If Section 115BBH is applied:

- Section 115BBH applies only where there is income from the transfer of a virtual digital asset. The section itself repeatedly uses the expression “transfer of any virtual digital asset.” Therefore, the first legal question is:

- Does an INR-settled crypto futures contract involve transfer of a VDA?

- If the answer is No, a strong argument exists that Section 115BBH may not apply.

- Section 115BBH applies only where there is income from the transfer of a virtual digital asset. The section itself repeatedly uses the expression “transfer of any virtual digital asset.” Therefore, the first legal question is:

- Conversion of INR to USDT: Buying USDT using INR does not trigger tax

- Tax on Conversion of USDT Back to INR : When converting USDT to INR:

- Principal Amount

- Taxable gain = Difference between USDT sale rate and purchase rate.

- Taxed under VDA provisions.

- Profit Amount: Additional gain arising from appreciation in USDT value after profit realization. Also, taxable.

- If the tax department considers the futures transaction as relating to a VDA and falling within the scope of Section 2(47A) read with Section 115BBH:

- Profit from Futures Trading: Profits are generally treated as business income and taxed according to the individual’s slab rate.

- If the department treats crypto futures as VDA transactions: The tax rate is a flat 30% tax. Plus applicable surcharge. And plus 4% cess. So income may be taxable at 30% plus applicable surcharge and cess.

- Profit and loss netting could be disputed.

- Each taxable gain may require independent consideration.

- Brokerage and transaction expenses may not be deductible except to the extent legally qualified as cost of acquisition (which is generally restrictive under Section 115BBH).

- No Deduction of Expenses: Brokerage Not allowed, exchange charges, Internet expenses, Advisory fees, Trading software expenses except cost of acquisition. No deduction is allowed except for the cost of acquisition.

- Loss Restrictions: No loss setoff, no carryforward, and no adjustment against salary, F&O, or business income.

- Set off of losses against other income is not permissible So, losses may not be available for set-off.

- Carry forward of losses is not allowed.

- This treatment could result in significantly higher tax exposure than the business-income approach.

- Reporting: Schedule VDA in ITR.

- This is generally the most conservative position from a tax litigation perspective.

- Taxation Under Section 115BBH (Conservative Department View). In case of a derivative / speculative business transaction settled without actual transfer of crypto: If Section 115BBH is applied:

-

TDS on Crypto Transactions: Relevant Sections

- Section 115BBH: Crypto gains taxed at 30%.

- Section 194S: 1% TDS on transfer of Virtual Digital Assets (VDAs), including cryptocurrencies and related transactions.

- TDS Thresholds: INR 50,000: Specified individuals/HUFs. And INR 10,000: Other taxpayers.

-

Impact on Filing of Your Income Tax Return

- ITR Reporting Requirement: Income from cryptocurrencies, crypto futures, crypto options, perpetual contracts, NFTs, and other VDAs must be reported in Schedule VDA while filing the Income Tax Return (ITR). Key Takeaways

- Crypto derivative taxation is complex and depends on the nature of the transaction.

- Futures profits are generally treated as business income.

- Gains from VDAs are typically taxed at 30% under Section 115BBH.

- 1% TDS applies on specified crypto transactions.

- All crypto-related income must be disclosed in Schedule VDA while filing ITR.

- ITR Reporting Requirement: Income from cryptocurrencies, crypto futures, crypto options, perpetual contracts, NFTs, and other VDAs must be reported in Schedule VDA while filing the Income Tax Return (ITR). Key Takeaways

-

-

Current Position on Taxation of Crypto Futures Trading-

Crypto Futures Be Treated as Speculative Business—Business Income from Derivative Trading:

-

- Derivative/contract settled in INR without actual delivery of cryptocurrency. in case it is considered business income, then the position will be. If crypto futures are treated as trading derivatives/business activity:

- The strongest technical argument currently available is Crypto Futures from

-

- A competing view is that where

- Contracts are INR-denominated,

- Settlement is in INR,

- No actual crypto asset is delivered or transferred,

- A competing view is that where

-

- Net profit and loss can be computed in accordance with normal business principles. Net profit may be taxable as business income.

- Normal business expenses may be claimed.

- Exchange charges and platform fees may be deductible.

- Combined analysis with your F&O activity would be required.

- Tax Rate Normal slab rates. Expenses Allowed and Deduction may be available for Platform charges, Internet, Professional fees, Data subscriptions, Trading software and Other legitimate business expenses.

- Loss Treatment: Speculative losses: Set off only against speculative profits. And carry forward possible up to 4 years.

- Tax audit applicability under Section 44AB needs to be examined based on account books, turnover computation, and profit ratios. Audit provisions may need examination.

- Presumptive taxation may generally not be appropriate considering the scale of transactions.

- ITR: Generally, ITR-3

|

Particulars

|

Amount

|

|

Profit Trades

|

INR 3.55 Cr

|

|

Loss Trades

|

INR 3.50 Cr

|

|

Net Profit

|

INR 5 Lakh

|

|

Charges

|

INR 15 Lakh

|

|

Gross Turnover

|

INR 7.05 Cr

|

Strong Legal Points Supporting Business Income Treatment

- For INR-settled CoinDCX Futures, if there is no crypto delivery occurs, Settlement is in INR, with No wallet transfer and no acquisition of BTC/ETH. No transfer of VDA as contemplated under Section 115BBH. And a transaction resembles a contract for differences (CFD) or derivative settlement. These are the principal arguments available in support of business/speculative income treatment.

- In case a trader with existing exchange F&O activity, it is regular trading frequency, large turnover, and INR-settled CoinDCX futures. There is a reasonably arguable position to disclose crypto futures under Business Income (Speculative Business) in ITR-3 with full disclosure and documentation.

CBDT Position: Important Finding: As of July 2026:

-

After reviewing the statutory provisions, current industry practices, and the absence of any specific CBDT clarification on crypto futures, the issue remains a grey area of Indian tax law.

-

The tax treatment depends on whether a crypto futures contract is considered: CBDT has not issued a specific circular clarifying taxation of INR-settled crypto futures. Therefore, no conclusive circular, No binding clarification, and no landmark judicial precedent directly on CoinDCX INR-settled crypto futures.

-

However, because Section 115BBH litigation is still unresolved for crypto derivatives, the position should be supported by exchange contract specifications, settlement mechanism, CoinDCX product documents, a legal note explaining absence of VDA transfer, and detailed working papers. Hence, the matter remains litigious.

- “India currently imposes one of the most stringent crypto tax regimes globally, with a flat 30% tax rate, no deduction of expenses, and no set-off or carry forward of losses. However, the taxation of crypto derivatives such as INR-settled futures, options, and perpetual contracts remains unsettled, creating an ongoing debate between treatment under Section 115BBH and taxation as speculative business income.”

ITR Filing Changes Checklist – AY 2026-27

Reporting and Compliance Considerations:

-

- CoinDCX product documentation.

- Whether actual crypto delivery occurs at any stage.

- Contract specifications of crypto futures traded.

- Settlement mechanism (cash settled vs. delivery settled).

- Annual transaction statement and ledger.

- Tax audit implications.

- Appropriate ITR schedule disclosure.

- Reconciliation with AIS/TIS information, if reported.

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.