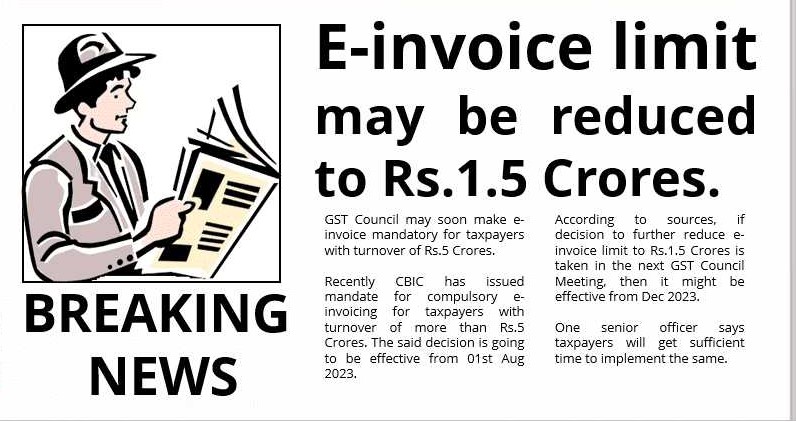

Is GST E-invoicing limit going to be can be decreased to INR 1.5?

Table of Contents

Is the GST e-invoicing limit going to be can be decreased to INR 1.5?

- The Goods and Services Tax Council may soon make e-invoicing compulsory for Goods and Services Tax taxpayers with a turnover of INR 50,000,000.

- Now the Central Board of Indirect Taxes and Customs has issued recommendations for mandatory new e-invoicing for Goods and Services Tax taxpayers with sales of more than INR 5,00,00,000. The above decision is going to be implemented with effect from 1.08.2023.

- As per sources, in the above case, the decision was to further decrease the e-invoice threshold limit to INR 1,50,00,000/-. is taken in the upcoming Goods and Services Tax Council Meeting, then it might be effective from 1st December 2023.

- One senior GST officer says Goods and Services Tax taxpayers will get sufficient time to implement the same.

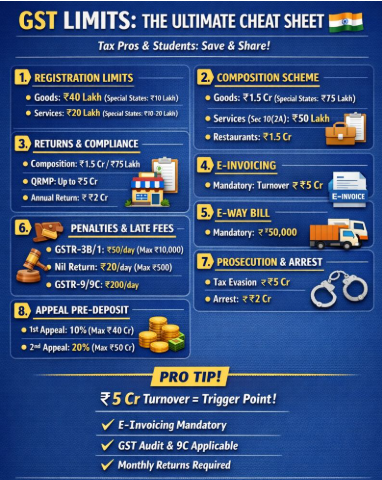

Who Must Generate e‑Invoices? (Turnover-based Phases)

| Phase | Applicable to taxpayers with AATO > | Effective From | Notification |

|---|---|---|---|

| I | ₹500 crore | 01‑10‑2020 | 61/2020, 70/2020 |

| II | ₹100 crore | 01‑01‑2021 | 88/2020 |

| III | ₹50 crore | 01‑04‑2021 | 05/2021 |

| IV | ₹20 crore | 01‑04‑2022 | 01/2022 |

| V | ₹10 crore | 01‑10‑2022 | 17/2022 |

| VI | ₹5 crore | 01‑08‑2023 | 10/2023 |

If turnover crosses the threshold in the current financial year, e‑invoicing applies from the next financial year.

Exemptions from e‑Invoicing under GST law

Regardless of turnover, the following entities are exempt:

- Notified Businesses : Insurers, Banks/Financial Institutions/NBFCs, Goods Transport Agencies (GTA), Passenger transport service providers, Cinema exhibition service providers (multiplex), SEZ units, Government departments & local authorities, and OIDAR service providers

- Documents/Transactions excluded : B2C supplies, Exempt/Nil-rated B2B or B2G supplies, Imports, High-seas/bonded warehouse transactions, FTWZ transactions and Reverse charge under section 9(4)

Time Limit for Reporting e‑Invoices under GST

- As per the advisory of 5 November 2024, the mandatory 30-day GST reporting time limit applies to AATO ≥ ₹100 crore. and extended to AATO ≥ ₹10 crore from 1 April 2025.

How e‑Invoicing Helps Prevent Tax Evasion under GST

- Real‑time reporting = immediate visibility of transactions

- No gap to manipulate invoices post-transaction

- Fake ITC becomes difficult due to system matching

- Audit trail improves transparency

Mandatory Fields of an e‑Invoice

The e‑invoice schema contains 12 sections + 6 annexures (total 138 fields), 5 mandatory sections like Basic details, Supplier details, Recipient details Invoice item details, Document total, and 30 mandatory fields, including Document type (INV/CRN/DBN), Supplier legal name & GSTIN, Address & State code, Invoice number & date, Item details, Tax amounts, and Original invoice reference (in case of amendments)

From 1 June 2025: IRP will treat invoice numbers as case‑insensitive and convert them to uppercase automatically.

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.