TAXATION & COMPLIANCES GUIDE FOR FREELANCERS

Table of Contents

A guide to understanding your income and income tax returns

A 9 to 5 job does not attract to everyone. Some people prefer a bit of flexibility so that they can explore other interests, spend more time with family, or simply avoid a repetitive routine. That is why people freelance from the convenience of their own home, a trendy café, or a coworking space. According to income tax legislation, freelancers, like other salaried or business taxpayers, must pay taxes on the income they earn.

Freelancing income is earned when you are hired to work on certain assignments for a specified period of time and are paid for the work after it is completed and submitted. You will not be hired or placed on the company’s payroll. You will not be eligible for benefits stipulated by the Company Act (such as PF). You are not forced to attend the office; in fact, you can finish the work at your leisure (by a pre-determined deadline) from any location that is suitable to you.

According to Indian income tax legislation, any income earned by demonstrating your intellectual or manual talents is considered income from a profession. Profits and Gains from Business or Profession will be taxed on this income. The total of all receipts you receive in the course of performing your profession will be your gross income. If you have received all of your professional revenue through banking channels, you can rely on your bank account statement to provide this information.

Expenses allowed as a deduction

Freelancers can subtract the expenses of doing the job from their earnings. This might include anything from workplace furniture to cab fare to clients’ homes. These expenses must be directly tied to the work that you undertake.

Conditions to claim expenses as a deduction from freelancing income

- The expense is for the freelancing work that you are doing.

- It was incurred throughout the tax year.The expense is for the freelancing work that you are doing.

- It is neither a capital nor a personal expense for the freelancer.

- It is not incurred for the aim of committing a crime or violating a law.

EXPENSES THAT CAN BE CLAIMED AS A DEDUCTION AGAINST INCOME

Rent of the property: The rent paid can be subtracted if you rent a property to carry out your employment.

Repairs undertaken: These repair costs can be deducted if you agreed to pay for repairs to the rental property. If you own the business property and make repairs, you can deduct those costs as well. Repairs to your laptop, printer, or other equipment are also qualified for a deduction.

Depreciation: The benefit of a capital asset is typically expected to extend longer than a year when you acquire it. When such assets are purchased, they are capitalised rather than charged to expenses. A small proportion of the expenditure is expensed each year and can be subtracted from your income. Depreciation is the annual expense that is charged.

For example, if you spend Rs.60,000 on a laptop to undertake freelance work, the Rs.60,000 is considered an asset. Assuming a straight line depreciation of 33.33 percent per year, annual costs will be Rs.20,000. We’d consider the asset to be fully depreciated in the next three years. The types of assets, methods of depreciation, and rates of depreciation to be charged are all specified in the Income Tax Act and must be followed.

Office expenses: Expenditures incurred in the course of your work, such as the purchase of a printer, office supplies, monthly phone bills, internet costs, and transportation expenses, can all be subtracted.

Travel Expenses: Travel expenses to meet with clients within or outside of India can be reduced.

Meal, entertainment, or hospitality expenses: It can be claimed when you hold client meetings, take clients out to dinner, or go on other trips with the sole purpose of acquiring new business or retaining existing business.

Local taxes and insurance for your own business property

Registration of a domain and the purchase of software to test your product are also allowable expenses.

How to claim expenses common to both personal and professional purposes

When assets are claimed or expenses are incurred for both professional and personal uses, only a fair portion of the expenditure and depreciation can be deducted, not the entire amount.

For instance, you use your cell phone for both professional and personal calls. As a result, you’ll only be allowed to deduct a reasonable fraction of your cell expense that’s related to your freelance employment.

Expenses that are explicitly disallowed to be deducted from your income

Case Study:

Ram, a freelance photographer, uses the space held by his married sister to conduct his business. Ram’s rent is an expense that can be subtracted from his freelancing earnings. Because Ram’s sister owns the property, he decides to transfer some of his income to her by paying her a higher than market rent. The excess payment will not be subtracted from your taxes.

Will this come under the scanner of the I-T Department when he files his income tax return?

The following expenses are explicitly disallowed to be deducted from one’s income as per the Income Tax Act:

- You are responsible for paying income tax.

- For non-payment or late payment of income tax, any interest, penalty, or fine

- Payments paid to relatives may not be deducted if the following conditions are met:

- You have gotten products, services, or facilities.

- Payment has been paid to a relative (spouse, or any lineal ascendant or descendant of you or your spouse) or to a person who owns a substantial stake (20% or more in equity or profits) in your company.

- The payment is either

(a) not in accordance with the fair market value of the goods/facility/service.

(b)Your profession does not have a justifiable need for it.

(c)As a result of incurring that expense, you gain a benefit.

If you pay for an expense in cash that exceeds Rs.10,000, you will not be able to claim it as a deduction.

Case Study:

Ram, a freelance photographer, uses the property held by his married sister to do his business. Ram’s rent is an expense that can be reduced from his freelancing earnings. Because the property is held by Ram’s sister, he decides to transfer some of his income to her by paying her a greater rent than the market would allow.

Will this be scrutinised by the IT department when he files his tax return?

Ram deducted the rent payment from his overall earnings as a business expense. His sister, who has no other source of income, only paid a 10% tax on the rental earnings When the beneficiary is a relative, the Assessing Officer may refuse to authorise a rent payment that is not in keeping with the fair market value of the premises.

We can assist you with your income taxes and tax filing. Within 48 hours, Tax Experts can prepare and e-file your tax returns. For freelancers and consultants, plans start at Rs.3,700.

Accrual Basis of Accounting (also called Mercantile Basis)

Cash Basis of Accounting

| Accrual Basis of Accounting | Cash Basis of Accounting |

| When a right to receive arises, income is accounted for or recorded. | When income, is received it is recorded. |

| When a payment obligation occurs, expenses are accounted for or booked. | Expenses are recorded when they are paid. |

| When income is booked, tax is due; nevertheless, tax may be due even if income has not been received. | Tax liability occurs in the year in which income is received, obliging you to pay tax only when income is obtained. |

| This method can be used for all types of income, however it is required for salary, house property, and capital gains. | Only profits and losses from a business or profession, as well as income from other sources, are allowed to be calculated using this method. |

| Example 1: You issue your client an invoice for a transaction on February 2nd, but you don’t be paid until April 4th. Based on the date the invoice was sent to the client, the revenue will be recorded in your account. | Example 1: When the payment is received, revenue will be accounted for on April 4th (which will be the tax year after the year in which the invoice was raised or work was performed) |

| Example 2: Your cellphone bill from February 15th to March 15th has arrived. For accounting purposes, this bill will be recorded as an expense in March.

This applies regardless of whether you pay by the 31st of March or not (you may actually pay in the next tax year). When your books of accounts are closed on March 31st for tax purposes, the mobile bill for the remaining 15 days of March will be incurred using a reasonable basis, based on an estimate. |

Example 2: Your cell bill from the 15th of February to the 15th of March has arrived, and if you pay it before the 31st of March, it will be recorded as an expense in the month of March (therefore, gets booked in the same tax year).

If you pay it in April, it will be recorded as an expense in the following tax year (though the expense or mobile usage pertains to the previous tax year). |

It’s important to remember that the accounting method you chose must be followed for all clients, all revenues, and all expenditure.

How to choose an accounting method

Using the cash basis of accounting method may appear to lower your tax liability. However, it is probable that it will merely postpone your tax payment However, you will not be able to save any money on taxes

Once you’ve opted on an accounting method, you must follow it on a regular basis. If your goal is to save or avoid taxes, you are not allowed to change your accounting system frequently.

Unless your receipts are irregular, imprecise, or unpredictable, it appears more sensible to use the Accrual Basis. The Income Tax Act states that books of accounts must be maintained for the purposes of income taxation. Section 44AA and Rule 6F have made these mandatory.

Total taxable income and tax payable

Making full use of Section 80 deductions can help you save money on taxes. Section 80C of the Income Tax Act encourages taxpayers to save for the future by providing tax relief on specified expenditure (by giving deductions on investments in financial products).

Net Taxable Income = Gross Taxable Income – Deductions

By claiming a deduction for the amount actually invested/spent under this clause, you can lower your taxable income by up to Rs.1.5 lakh. If you are under the age of 60 and have a net taxable income of more than Rs.2.5 lakh, you must pay income tax.

Here is how tax will be calculated on your income:

Tax payable for a freelancer

If a taxpayer’s total tax burden for the year exceeds Rs.10,000, he or she must pay taxes every quarter. This is referred to as advance tax.

How to calculate advance tax?

Calculate your overall income by adding up all of your receipts.

Subtract only the expenses that are directly relevant to your job.

Include earnings from other sources, such as a rental property or a savings account.

Determine your tax slab and compute your tax liability.

Remember to deduct TDS

If your tax payment exceeds Rs.10,000, you must pay advance tax by the deadlines listed below.

Due date for Advance Tax

| On or before 15th June | Not less than 15% of advance tax |

| On or before 15th September | Not less than 45% of advance tax as reduced by the tax paid in the last installment. |

| On or before 15th December | Not less than 75% of advance tax as reduced by the tax paid till the last installments. |

| On or before 15th March | The whole amount (100%) of advance tax as reduced by the tax paid till the last installments. |

Which ITR to file? Need help from an expert to calculate and pay your advance tax? Reach out to us info@caindelhiindia.com Freelancers must file income tax returns on ITR-4.

Do you have questions concerning the ITR-4 Form? Why not check out our in-depth guide on the ITR-4 Form? Take a look at our ITR-4 Guide.

How to pay advance tax?

It can be done in two ways.

You can make a payment via the IT Department’s website. A screenshot instruction to filing tax dues on the government website can be found here.

You can also visit your bank in person to fill out a paper challan and deposit tax.

Penalties for non-payment of advance tax

If you don’t pay your advance tax, you’ll be charged interest under Sections 234B and 234C. Pay advance tax when your tax due in a year is Rs. 10,000 or greater to avoid interest penalties under Section 234B and 234C.

Advance tax payments made until the 31st of March of the year should cover 100% of your overall tax liability.

Section 234B applies when Advance Tax is not paid, and as Advance Tax is due on the dates specified by the IT Department, section 234C applies when interest is not paid on the due dates. You may read more about 234B and 234C here.

Applicability of GST to freelancers

Previously, freelancers were subject to VAT and Service Tax. GST has now taken the role of these taxes.

If you sell goods

The GST has taken the place of the previously applicable VAT. The GST rate you pay will be decided by the things you sell. If you make and sell cakes to bakeries, for example, you must charge 18% GST. Presently, this is the GST rate that applies to cakes.

If you provide service

Most services are subject to an 18 percent GST. As a result, you must charge clients 18 percent GST for your freelancing services. To get the most up-to-date rates, use our simple GST Rate Finder.

Things to remember under GST

- GST is not applicable if the total revenue from freelance work does not exceed Rs. 20 lakhs.

- If you sell items, you may be qualified for the composition programme.

- The composition scheme is not applicable to services. You can, however, supply interstate services up to Rs. 20 lakhs without having to register for GST.

- On exports, the GST does not apply.

- For additional information, see our article on the GST’s effects on freelancers.

How to understand whether I need to apply for GST?

If your annual gross turnover is higher than Rs.20 lakhs, you must register for GST (Rs.10 lakhs for North Eastern and hill states).

How to calculate my aggregate turnover in a year?

To see if you need to register for GST, read our article on how to calculate aggregate turnover.

How to make GST payments?

Payments for GST can be made online. If your payments total more than Rs.10,000, you must make them online. GST must be paid to the government on a quarterly or monthly basis, depending on your turnover and composition scheme.For any delays in depositing service tax with the government, interest will be charged.

How to file GST returns?

GST returns are due quarterly or monthly, depending on your turnover and whether you’ve opted the composition scheme. Quarterly returns are available to composition dealers and those with yearly sales of less than Rs.1.5 crore.

Return filing is required once you get a GST Identification number.

Do you have a question about GST?

If you have any queries about whether GST applies to your income or if you need to register, please contact us at info@caindelhiindia.com.

Should Freelancers file TDS Return?

- Freelancers may be paid after TDS. Similarly, before making a payment, freelancers must Tax deduct at source. As an example, consider the following:

- Ram is a freelance graphic designer who works for a variety of clients. he is paid on a project-by-project basis rather than a monthly wage. Before paying out, the client deducts tax at source in each of these payments. He is, however, unaware of the tax she must deduct at the source.

- Many freelancers have a business name and a bank account designated for business activities, and they are taxed as small enterprises. When Ram is faced with tight deadlines, he appoints professionals to assist her meet them. In this instance, He must deduct tax from the sums payable to them at the time of payment.

- TDS is applied at a rate of 10% whenever a freelancer or a small business owner makes a payment to professionals that exceeds Rs.30,000 per transaction or in total throughout a financial year. The tax that was deducted at the source must be paid to the government.

- Furthermore, a freelancer is only required to deduct tax or TDS if he was audited during the preceding fiscal year. Only if a freelancer’s annual gross receipts reach Rs 50 lakh will he or she be audited. There is no need to deduct tax at source if this is not the case. TDS will be applied to different payments made by freelancers, including salary and contractual payments, if the yearly gross receipts exceed Rs 50 lakh and the freelancer’s accounts have been audited in the previous year.

- TDS would have to be applied to all payments covered by TDS requirements, which the freelancer would have to verify for. In addition, once the taxes have been deducted, freelancers must deposit the money and file TDS returns.

About IFCCL

IFCCL is a trusted name in professional taxation services, offering specialized Income tax filing for freelancers and professionals with accurate compliance and strategic planning support. We understand the unique financial structures of consultants, doctors, architects, startups, and independent professionals, ensuring proper reporting of income, expenses, and tax optimization. Our experts design effective Tax strategies to reduce business tax liability, helping clients leverage deductions, depreciation benefits, presumptive taxation schemes, and lawful tax planning techniques. In addition, IFCCL provides dedicated Help with responding to income tax notices, including drafting replies, representation before authorities, assessment support, and handling scrutiny matters with confidence and clarity. With a proactive and compliance-focused approach, IFCCL ensures peace of mind while safeguarding your financial interests. Contact us at 9555 555 480 or Singh@carajput.com/singh@caindelhindia.com

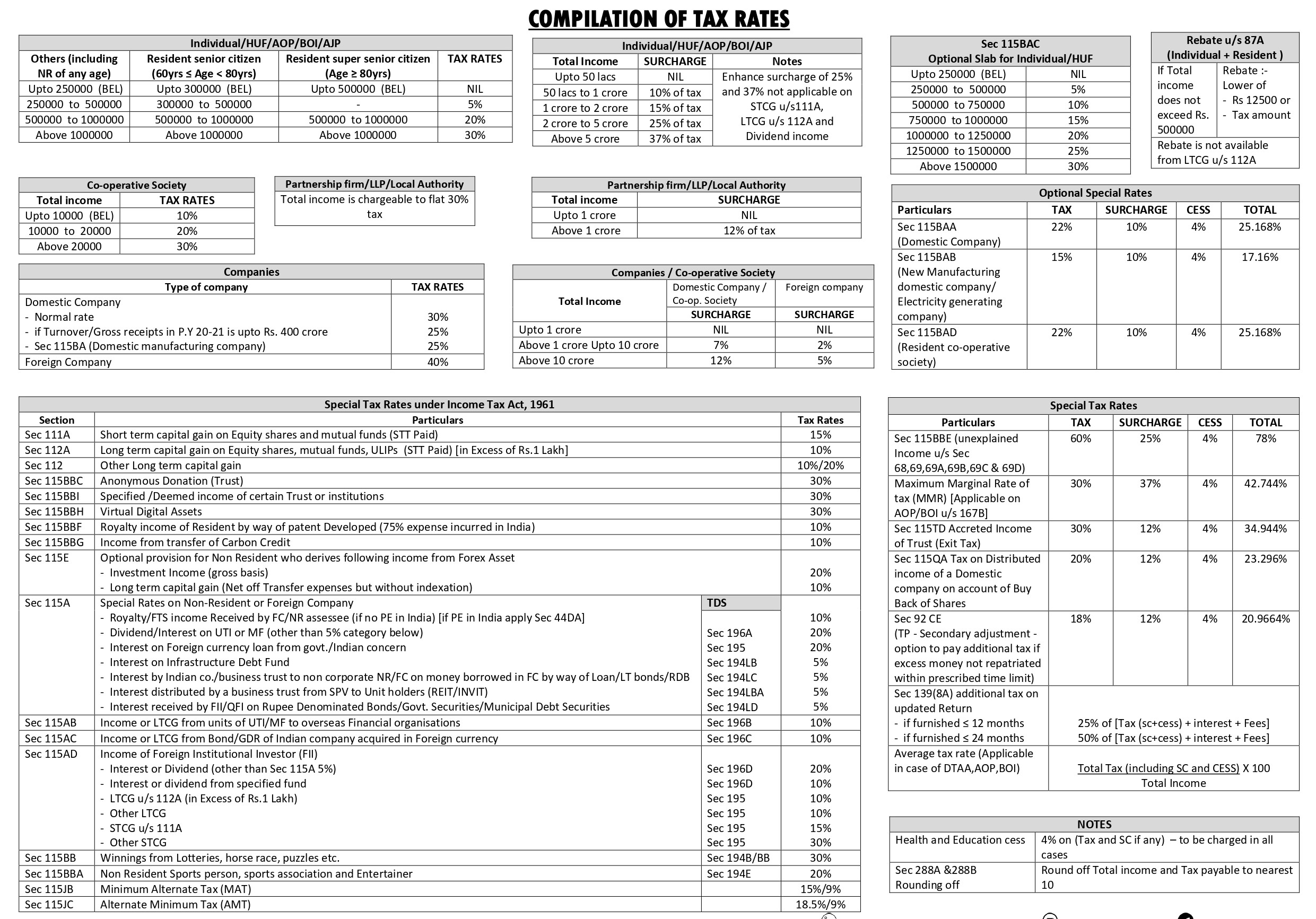

Latest Income Tax Slab & Tax Rates in India –

Compilation of all Tax Rates (revised)

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.