TDS & GST Provisions for Metal Scrap Transactions

Table of Contents

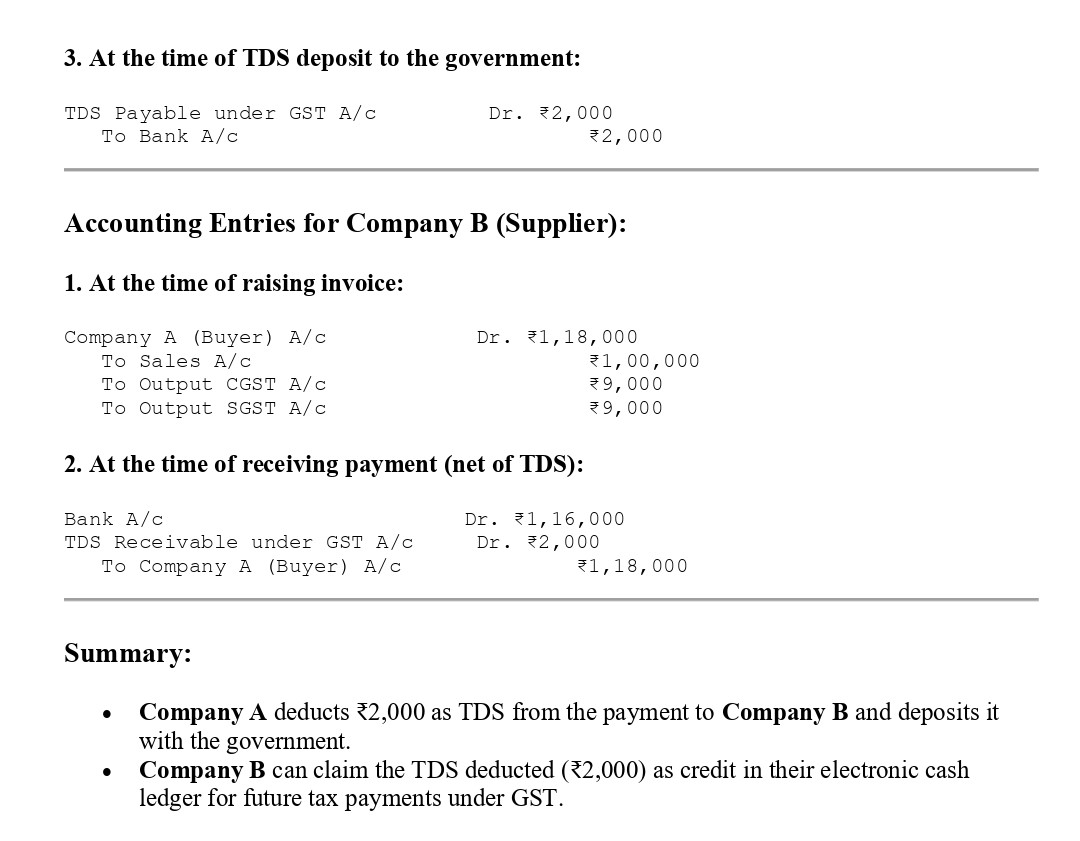

New TDS & GST Provisions for Metal Scrap Transactions and do this on GST Portal now

The amendments regarding the applicability of TDS on metal scrap transactions, effective from October 10, 2024, bring several key implications for businesses and the broader metal scrap industry: Overall, this amendment will significantly impact the metal scrap industry by increasing compliance obligations, improving tax tracking, and contributing to the government’s goal of curbing tax evasion in the scrap supply chain. With the provisions introduced by Notification No. 25/2024-Central Tax, companies have limited time to ensure compliance before the TDS requirements become effective. Immediate action is required to align accounting systems, train staff, and ensure proper record-keeping and reporting mechanisms for metal scrap transactions.

The Notification No. 25/2024-Central Tax, issued by the Ministry of Finance on October 9, 2024, introduces amendments to Notification No. 50/2018-Central Tax dated September 13, 2018, under the provisions of Section 51 of the Central Goods and Services Tax Act, 2017. These changes specifically focus on the TDS provisions under the GST regime, with a clear emphasis on businesses dealing in metal scrap.

1. TDS Applicability on Metal Scrap Transactions:

- The inclusion of clause (d) now mandates TDS compliance for businesses dealing with metal scrap, covering metals categorized under Chapters 72 to 81 of the Customs Tariff Act, 1975.

- This ensures that registered recipients of metal scrap must deduct tax at source under the CGST Act, increasing transparency and accountability throughout the supply chain.

- Businesses receiving supplies of scrap metal will need to assess each transaction to determine TDS applicability, ensuring they remit the correct tax amounts.

2. Exemptions for Specified Persons:

- The revised third proviso continues to grant exemptions from TDS for specific transactions involving entities outlined under Section 51(1) of the CGST Act. However, an exception is made for metal scrap recipients, ensuring that this sector is included under the TDS framework.

- This indicates a targeted focus on the metal scrap industry to improve tax compliance while maintaining flexibility for other specified entities.

3. Enhanced Compliance for the Metal Scrap Industry:

- Bringing metal scrap transactions under TDS will require businesses to adopt stricter compliance practices, such as:

- Maintaining proper documentation of transactions.

- Ensuring timely tax deductions at source.

- Regularly filing TDS returns.

- The amendment promotes better monitoring and compliance within the sector, which is often considered high-risk for tax evasion due to the nature of cash-based or informal transactions.

4. Operational Impact on Businesses:

- Businesses engaged in the purchase and sale of scrap metal must review their internal processes and systems to integrate the TDS deduction process.

- Failure to comply with the new requirements could result in penalties, interest, and other legal consequences under the CGST Act.

FAQ on TDS to be deducted when metal scrap is purchased from registered suppliers.

Effective Date: October 10, 2024:

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.