Guidelines on Section 194R of the Income Tax Act

Introduction to Section 194R

Section 194R was introduced to streamline the deduction of Tax Deducted at Source on benefits or perquisites provided in the course of business or profession. This section mandates that any person providing a benefit or perquisite to a resident must deduct tax at a rate of 10% on the value of such benefit or perquisite. Section 194R of the Income Tax Act, addresses the deduction of tax at source on any benefit or perquisite provided to a resident arising from business or profession. Section 194R introduces a structured framework for the deduction of TDS on benefits or perquisites provided in the course of business or profession. Compliance requires careful identification, valuation, and timely deduction of TDS to avoid penalties and ensure adherence to the Income Tax Act. Businesses and professionals should familiarize themselves with the guidelines and integrate them into their financial processes. Below details for TDS on reimbursements to service providers under this section:

Table of Contents

Scope & Coverage of Section 194R

- Applicability:

- Who is Covered? Applies to any person (deductor) providing benefits or perquisites to a resident (deductee) arising from business or profession. The section covers all benefits or perquisites, whether in cash or in kind, provided to a person, if these are part of their business or profession.

- Types of Benefits or Perquisites:

- Wholly in Cash

- Wholly in Kind

- Partly in Cash and Partly in Kind

- Capital Assets: Benefits can include capital assets like cars, land, etc.

- Liability:

- The deductor does not need to verify whether the benefit or perquisite is taxable in the recipient’s hands.

- There is no requirement to check the taxability of the amount itself.

- Applies to benefits or perquisites paid or credited on or after July 1, 2022.

- Purpose of Section 194R:

- It requires the deduction of tax at 10% on the value of any benefit or perquisite provided to a resident in the course of business or profession.

TDS on Reimbursements:

- TDS Rate u/s 194R

-

- Standard Rate: 10% TDS on the total value of gifts or perquisites provided to a recipient during a FY.

- Threshold Limit: Tax Deducted at Source is applicable only if the total value exceeds INR 20,000 per recipient in a FY.

- Invoice in the Name of the Recipient: If the invoice for the expenses (such as travel or accommodation) is issued directly in the name of the service recipient, it is treated as the service recipient’s own expense. In this case, no Tax Deducted at Source is required u/s 194R, as no benefit or perquisite has been provided by the service recipient to the service provider.

- No TDS u/s 194R on Directly Invoiced Expenses: If the reimbursement of expenses is billed directly to the service recipient (i.e., the invoice is made in the name of the service recipient), no TDS is required u/s 194R as there is no benefit or perquisite being provided to the service provider.

TDS on Reimbursements

-

- As per Circular No. 12/2022, if a person incurs expenses on behalf of another in the course of business or profession, it is considered a benefit or perquisite. Hence, Tax Deducted at Source at 10% applies on such reimbursements. Examples:

-

-

- Travel Expenses: If a service provider incurs travel expenses while performing services and these are reimbursed by the recipient, TDS u/s 194R is applicable on the reimbursed amount.

- Invoice in Recipient’s Name: If the expense invoice (e.g., travel, accommodation) is issued directly in the name of the service recipient, it is treated as the recipient’s own expense. No Tax Deducted at Source u/s 194R is required.

-

-

Additional Clarifications (Circular No. 18/2022, dated 13-09-2022):

- Consolidated Invoices: If reimbursement expenses are included in the same invoice as the primary service or goods, and TDS has been deducted under another section (e.g., 194C, 194J), no additional Tax Deducted at Source u/s 194R is required.

- Directly Invoiced Expenses: No Tax Deducted at Source u/s 194R if reimbursement expenses are billed directly to the recipient.

- This circular provided additional clarification regarding the application of Section 194R on reimbursements. If the expenses are already included in the invoice for services or goods (such as u/s 194C or 194J), and Tax Deducted at Source has been deducted under those sections, there is no need for further TDS deduction u/s 194R.

- Consolidated Invoice: If out-of-pocket expenses are included in the same invoice as the primary service or supply of goods, and TDS is deducted under another applicable section (e.g., Section 194C for contracts or Section 194J for professional services), no additional TDS is required u/s 194R.

-

Valuation of Benefits or Perquisites

-

- Fair Market Value: The Fair Market Value of the benefit or perquisite is generally used for Tax Deducted at Source calculation.

- Exceptions:

-

-

- Purchased Benefits: If the provider purchased the benefit, the purchase price is used for Tax Deducted at Source.

- Manufactured Benefits: If the provider manufactures the benefit, the price charged to other customers is used for Tax Deducted at Source .

-

-

- Exclusions:

- GST is not included in the valuation for Tax Deducted at Source purposes.

-

Specific Considerations for Section 194R

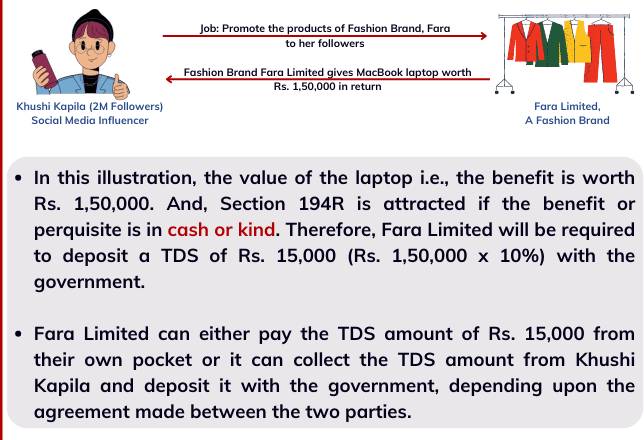

- Social Media Influencers:

-

- Returned Products: No benefit; no Tax Deducted at Source u/s 194R.

- Retained Products: Treated as a benefit or perquisite; Tax Deducted at Source applicable.

-

- Reimbursement of Out-of-Pocket Expenses:

- General Rule: If a person incurs expenses as part of their business and these are reimbursed, it is considered a benefit or perquisite. TDS at 10% applies.

- Exception: No TDS if travel bills are in the recipient’s name, paid by the consultant, and reimbursed by the client.

- Dealers’ Conferences:

-

- Non-TDS Scenarios: Expenditure for dealer/business conferences aimed at education, product launches, obtaining orders, teaching sales techniques, addressing queries, or reconciling accounts.

- TDS Applicable: If the conference includes incentives or benefits to select dealers/customers based on targets, Tax Deducted at Source is applicable.

- Leisure Components: Expenses for leisure trips, sponsoring family members, priority stays, or overstays are liable for Tax Deducted at Source.

-

- Benefits Provided to Employees of Recipient Entity:

- Benefits to employees, directors, or their relatives who are not engaged in business or profession require TDS by the deductor. Example: A company provides free medicine samples to a doctor employed by a hospital. The company must deduct Tax Deducted at Source u/s 194R in the hospital’s name.

- Benefits Provided by Employer to Employees:

- Treated as perquisites u/s 17.

- TDS u/s 192: Employers must deduct Tax Deducted at Source u/s 192 for employee benefits and can claim credit by furnishing tax returns.

- Benefits Provided to Consultants:

- Option 1: Deductor treats the entity as the beneficiary and deducts Tax Deducted at Source u/s 194R. The entity can further deduct TDS for the consultant.

- Option 2: Deductor can directly deduct Tax Deducted at Source for the consultant.

- Handling GST in Valuation

-

- Exclusion of GST: GST is not included in the valuation of benefits or perquisites for Tax Deducted at Source purposes u/s 194R.

- Managing TDS When Benefit Is in Kind or Partly in Kind

-

- Insufficient Cash for TDS: If the benefit is in kind or partly in kind, and the cash component is insufficient to cover the 10% TDS, the deductor has two options:

-

-

- Advance Tax Payment by Recipient: The recipient pays the tax as advance tax. The deductor relies on the recipient’s declaration and a copy of the advance tax challan.

- Grossing Up: The deductor deducts TDS by grossing up the benefit, treating the TDS as an additional benefit to the recipient.

-

- Computing the Rs. 20,000 Threshold

-

- Inclusion Period: Include benefits or perquisites provided on or before June 30, 2022, to assess the threshold for benefits provided on or after July 1, 2022.

- No TDS on Pre-July 1, 2022 Amounts: No TDS is required on amounts paid from April 1, 2022, to June 30, 2022.

Applicability of Section 194R on Lucky Draw Award Money:

- Section 194R of the Income Tax Act, 1961, deals with the TDS on benefits or perquisites arising from business or profession. It covers both monetary and non-monetary benefits provided to a resident.

- Key Phrase – “Arising from Business or Profession”: The applicability of Section 194R hinges on whether the benefit or perquisite arises in the course of business or the exercise of a profession. This is a critical factor for deciding if TDS should be deducted.

- Lucky Draw and Personal Achievements: If award money is provided for a personal reason such as winning a lucky draw or a personal achievement that is not related to the individual’s business or professional activities, it is not connected to business or profession.

- In such cases, the award does not fall under the ambit of Section 194R. Therefore, TDS would not be applicable under this section, as the benefit is purely personal and does not arise from a business or professional relationship. However, other sections, such as Section 194B (which deals with winnings from lotteries or games), may apply depending on the nature of the prize.

Practical Steps for Compliance of Section 194R

-

- Identify Benefits or Perquisites: Assess all benefits or perquisites provided to residents in the course of business or profession.

- Determine Valuation: Calculate the FMV or applicable purchase/manufacture price, excluding GST.

- Check Threshold: Aggregate benefits per recipient for the FY & Apply TDS only if the total exceeds Rs 20,000.

- Deduct TDS: Deduct 10% TDS on the value exceeding the threshold. Ensure proper documentation and compliance with procedural requirements.

- Deposit and Report: Deposit the deducted TDS with the government. Report the Tax Deducted at Source in the appropriate returns.

- Maintain Records: Keep detailed records of all benefits or perquisites provided and TDS deducted.

Frequently Asked Questions on section 194R

- Do we need to check if this perquisite is taxable in the hands of the payee?

Answer: No. Tax Deducted at Source must be deducted irrespective of the taxability of the benefit or perquisite in the recipient’s hands. All benefits provided in the course of business or profession are deemed taxable.

- Should we deduct TDS on discounts or offers given to our customers?

Answer: No. Sales discounts, cash discounts, rebates, and similar offers do not attract TDS u/s 194R. However, free samples provided to customers are subject to Tax Deducted at Source.

- Can the recipient claim depreciation on the asset received as a benefit?

Answer: Yes. The recipient can claim depreciation based on the fair market value (excluding GST) of the asset, on which taxes have been paid.

- Is TDS applicable on cash discounts?

Answer: No. Cash discounts, rebates, and similar offers are excluded from Section 194R. Only benefits or incentives other than discounts or rebates (e.g., cars, electronics) attract TDS.

- Does a company manufacturing capital goods need to deduct Tax Deducted at Source u/s 194R on 2-year free maintenance services provided to the buyer?

Answer: No. Section 194R applies only when an actual benefit or perquisite is provided, not merely for providing maintenance services unless such services constitute a perquisite or benefit as defined under the Act.

- How should the valuation of benefit or perquisite be carried out?

Answer:

-

-

- Purchased Benefits: Use the purchase price.

- Manufactured Benefits: Use the price charged to other customers.

- Exclude GST from the valuation.

-

Summary Section 194R:

- TDS at 10% u/s 194R applies when a service provider incurs expenses and those are reimbursed by the recipient, as it constitutes a benefit or perquisite.

- No Tax Deducted at Source u/s 194R if:

- The expense invoice is in the recipient’s name (i.e., it is their liability directly).

- Reimbursement expenses are included in the same invoice as the service or goods provided, and Tax Deducted at Source has already been deducted under another section (e.g., 194C or 194J).

- The provider of the benefit does not need to ascertain if the amount is taxable u/s 28(iv) before deducting Tax Deducted at Source.

- Section applies even if the benefit is in cash or partially in kind.

- TDS applies even if the benefit is in the form of a capital asset.

- Sales discounts, cash discounts, and rebates are not considered benefits under this section.

- The valuation of benefits should be done based on the fair market value of the perquisite provided.

- Social media influencers provided with products to promote on social platforms are considered to have received a benefit.

- Reimbursement of out-of-pocket expenses is not considered a benefit.

- Dealer conferences for educating dealers about products are not considered benefits if they are purely educational and do not involve any leisure or recreational elements.

- If the benefit is in kind and there is no cash available for Tax Deducted at Source, the provider must ensure that Tax Deducted at Source has been deposited before releasing the benefit.

- Threshold is calculated for the entire financial year, including transactions before and after 1st July 2022, when the section became applicable.

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.