GSTR‑2B Place of Supply mismatch & ITC Eligibility

Table of Contents

GSTR‑2B Place of Supply (PoS) Mismatch & ITC Eligibility

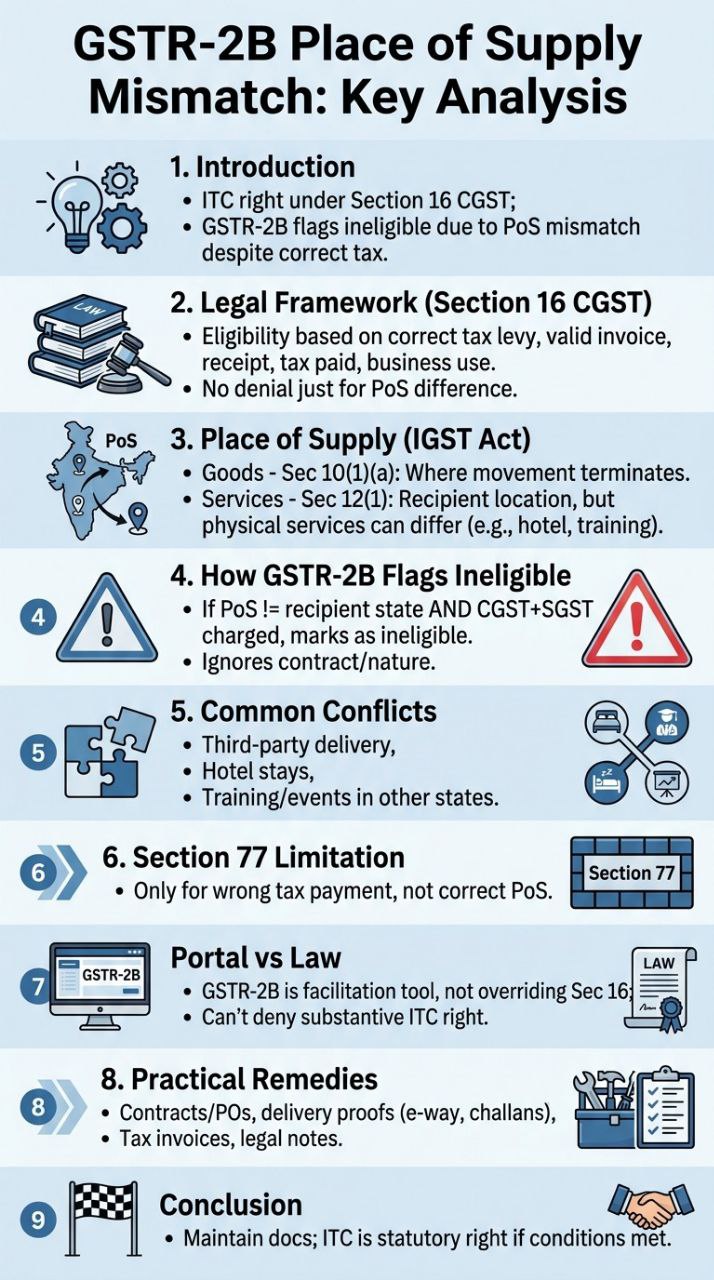

The issue of GSTR‑2B marking input tax credit as “ineligible” due to a place of supply mismatch has become one of the most frequent triggers during GST audits, departmental scrutiny, and internal reconciliations. While the GST portal follows a mechanical rule‑based flagging system, the law (Sections 16 & 17 of CGST Act + PoS rules under IGST Act) gives a much broader and more substantive basis for ITC entitlement.

Introduction—Why place of supply mismatches are misunderstood:

Taxpayer GSTR‑2B may mark input tax credit as ineligible even when The supplier has charged the correct tax, the supply is genuinely used for business, and all Section 16 conditions are satisfied. This happens because GSTR 2B’s algorithm tests GSTIN‑wise place of supply consistency, not the substance of supply. Key message: GSTR-2B is an advisory document; input tax credit eligibility flows from the Act, not the portal.

Legal Framework – Section 16 under the Central Goods and Services Tax Act, 2017:

Section 16 under the Central Goods and Services Tax Act, 2017 grants input tax credit if four conditions are met You possess a valid tax invoice. You have received the goods/services. Tax is actually paid by the supplier to the government. And The input is used in the course or furtherance of business. There is no ground in Section 16 under the Central Goods and Services Tax Act, 2017 allowing input tax credit denial only because PoS differs from your GST registration State. The law requires correct tax levy, not matching 2B flags.

Place of Supply—The Root of Confusion: The IGST Act governs Place of Supply:

- Goods – Sec 10(1)(a): Place of Supply = where movement terminates.

Example: Third‑party delivery, bill‑to/ship‑to. - Services – Sec 12: Sec 12(1): Default Place of Supply is the location of the recipient. But specific services override this (hotel, training, event, and performance‑based services), where the place of supply is tied to the location of actual performance or immovable property. Hence, the Place of Supply and your GSTIN State need not match in legitimate scenarios.

Why GSTR‑2B Flags ITC as Ineligible:

The portal marks input tax credit ineligible when the Place of Supply is your state, but the supplier charges CGST + SGST of another state.

Example: You (GSTIN in Delhi) attend a training in Mumbai. Vendor correctly charges MH CGST+SGST (since service is performed in MH). GSTR 2B flags this as ineligible, but it is genuinely ineligible—since state-specific SGST/CGST cannot be availed in another state. However, 2B also erroneously flags eligible IGST services performed in another state because it doesn’t interpret the nature of service. Conclusion: GSTR 2B looks only at state codes, not the contractual nature of supply.

Common Conflicts Leading to Place of Supply Mismatch Flags:

- Third‑party delivery (bill‑to/ship‑to). Goods were delivered to another state on your instruction; IGST is correct, but 2B may disagree.

- Hotel stays / immovable property services: Correctly taxed as State CGST + SGST of hotel state; input tax credit is actually ineligible unless you have registration or ISD mechanism.

- Training or events in another state: The supplier charging IGST is correct if the contract is with HO; GSTR 2B often misflags it.

- Repairs/AMC at site : Often IGST is the correct tax but portal mismatches the consumption state.

- Multi‑State vendor billing errors: Vendor uses wrong PoS code → GSTR 2B shows it’s ineligible.

Section 77 – Limited Scope

Section 77 allows correction only when the wrong tax head is paid, IGST instead of CGST+SGST or CGST+SGST instead of IGST. It does NOT apply when the place of supply itself is correct but different from the GSTIN state. Many taxpayers mistakenly try to use Sec. 77 under the Central Goods and Services Tax Act, 2017, for Place of Supply disputes. It applies only to the wrong head, not the wrong place of supply determination by the portal.

Portal vs. Law—The Crucial Legal Stand:

GSTR‑2B is a facilitation tool, NOT a statutory document. It cannot override Section 16 or the IGST Place of Supply rules. During an audit or SCN, your stance should be “Eligibility of input tax credit is determined by the CGST/IGST Acts. The 2B flag is advisory and cannot deny substantive input tax credit where the supplier has correctly charged tax and Section 16 conditions are satisfied. No circular, rule, or law makes GSTR-2B conclusive.

How to Defend ITC & Avoid Litigation

- Evidence to maintain: Purchase order / contract clearly defining nature of supply, Delivery challans, e‑way bills (for goods), Attendance proofs, work completion reports (services) and Supplier’s GSTR‑1 and tax payment in GSTR‑3B, also a legal note linking the supply to correct Place of Supply section

- Procedural safeguards: Build internal Place of Supply review checkpoints in AP team. For hotel/training invoices → pre‑check GSTIN state; for third‑party delivery → retain bill‑to/ship‑to evidence. The taxpayer must ask vendors for correct Place of Supply and credit notes if misclassified

- ISD registration for multi‑state service consumption : Useful for corporates consuming services across many states.

- When input tax credit is actually ineligible: Hotel CGST+SGST of another State, Event/immovable property services away from your GSTIN state, and Purely local services that require registration in that State

- When input tax credit is defensible despite 2B mismatch : IGST charged correctly on services rendered out‑of‑State, third‑party deliveries, Online/electronic services consumed by HO and AMC/work performed in another State but billed to HO under Sec 12(1) under the Central Goods and Services Tax Act, 2017

Conclusion

- Always maintain documentation—it wins cases. Taxpayers should not rely on GSTR 2B, as law relies on Section 16 + Place of Supply rules. Input tax credit cannot be denied merely due to a 2B “ineligible” Place of Supply flag. Correct tax + correct Place of supply + business use = input tax credit eligible (unless specifically restricted). Treat the GST portal as a tool, not as a legislative authority.

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.