Strategic Planning for Payments by Firms to Partners

Table of Contents

A Paradigm Shift in Partner Taxation

Earlier Positions of Professional and trading firms Treat partner payouts

- Historically, payments by partnership firms to partners, such as interest on capital, remuneration, commission, or salary, were outside the scope of TDS due to the principle of mutuality and the unique partner–firm relationship.

- This position has changed with the introduction of Section 194T through the Finance Act, 2024, which brings such payments into the TDS framework. U/S 194T: Firms must now deduct TDS at 10% on specified payments made to partners.

- This marks a structural shift with direct implications for cash‑flow planning of partners, year‑end tax optimization strategies, and compliance and penalty exposure of firms. As a result, both professional and trading firms can no longer treat partner payouts as routine internal adjustments.

- They now require advance planning, accurate accounting, and strict attention to timelines to avoid interest costs and compliance risks.

Why Firms Must Watch Timely Compliance of TDS U/S 194T

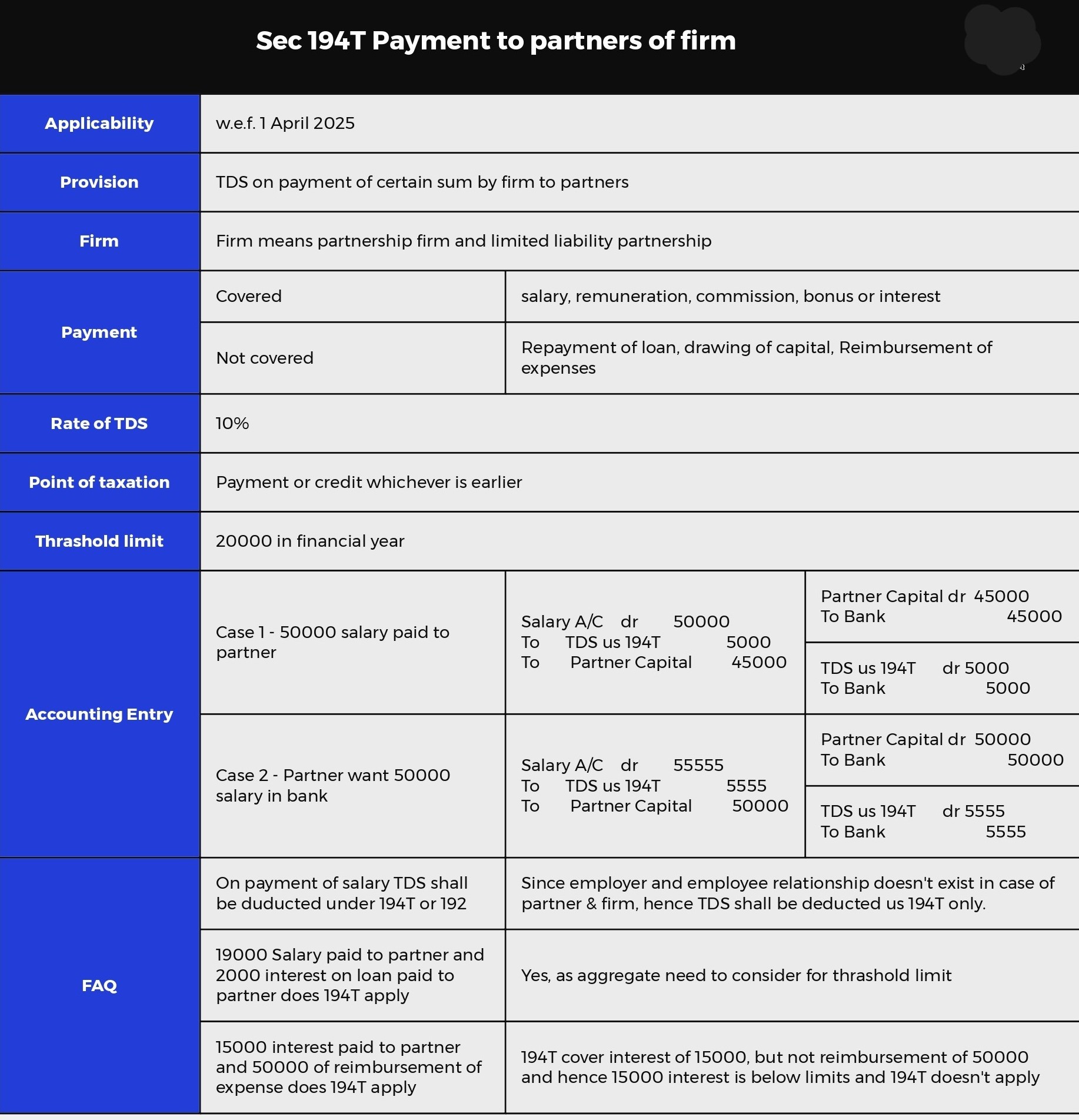

What Section 194T – Scope & Application of Section 194T

Section 194T was introduced by the Finance (No. 2) Act, 2024, to bring payments by firms to partners such as salary, remuneration, commission, bonus, and interest within the Tax Deducted at Source framework, overcoming earlier judicial rulings that kept such payments outside Tax Deducted at Source.

The provision applies from 1 April 2025 (transaction‑based, not assessment‑year‑based) and requires Tax Deducted at Source at 10% where aggregate payments to a partner exceed ₹20,000 in a financial year.

TDS u/s 194T applies to payments by a firm to its partner in the nature of interest on capital/loan, remuneration or salary, bonus, commission or fees, and any amount by whatever name called, provided it is taxable in the hands of the partner.

A partnership firm / LLP must deduct Tax Deducted at Source @ 10% on interest to partners or remuneration (salary, bonus, commission, etc.). If total payments exceed INR 20,000 in a year. Whichever is earlier payment or credit.

Key Threshold of Section 194T :

- No TDS if aggregate payment to a partner does not exceed INR 20,000 in a financial year

- Tax Deducted at Source rate: 10%, without surcharge or cess

- Even payments credited to partner’s capital/current account attract Tax Deducted at Source. Actual cash outflow is not required to trigger a deduction.

- The obligation applies to all firms, including Indian LLPs, irrespective of whether they are assessed as firms or AOPs, and covers payments to working and non‑working partners, including minors admitted to benefits. Tax Deducted at Source is triggered at the earlier of credit (including capital account) or payment, with no facility for lower/nil deduction under Sections 197 or 15G/15H; the absence of a Permanent Account Number attracts 20% Tax Deducted at Source.

Common Risk Areas:

- Year‑end provisioning of partner remuneration (March entries)

- Monthly interest accrual on capital balances

- Back‑dated partnership deed clauses

- Lump‑sum remuneration credited at year end Even a journal entry can trigger TDS liability.

Key timing rules:

- Tax Deducted at Source for March deductions must be deposited by 30 April

- Any part of a month is treated as a full month for interest purposes

- Tax Deducted at Source is attracted even on book entries or provisions, not just cash payments

- This provision applies to payments or credits made on or after 1 April 2025, marking the end of the long‑standing TDS immunity on partner payouts.

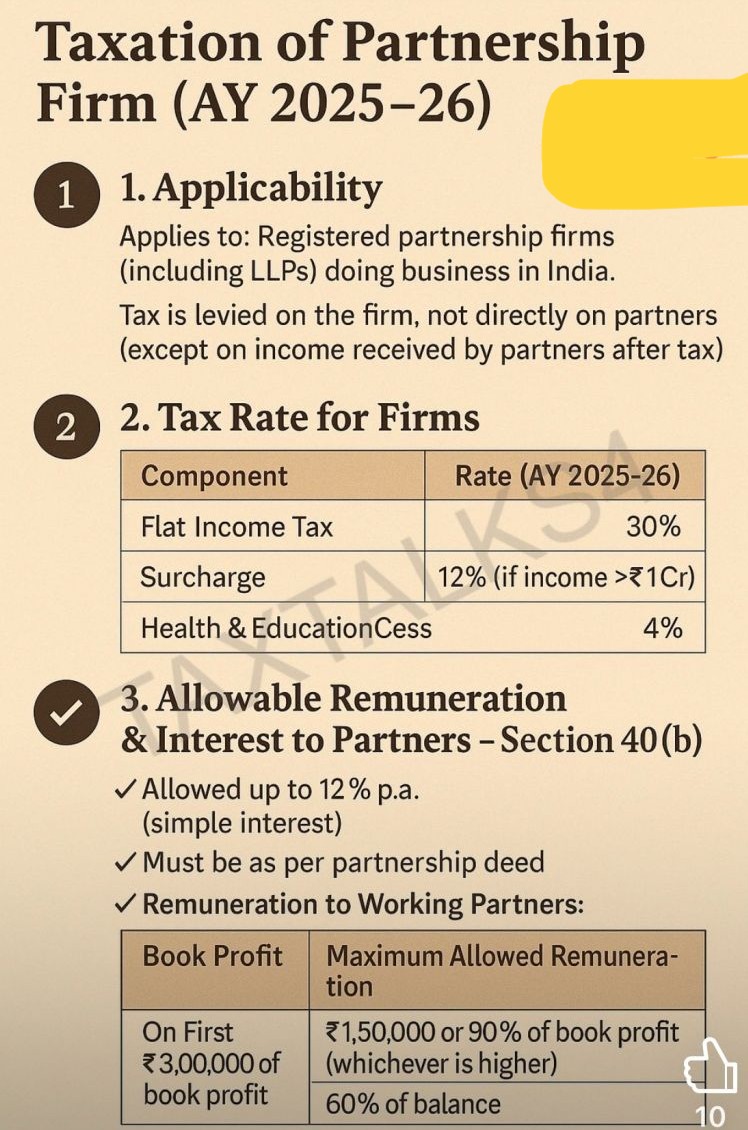

Interest & Remuneration: Interaction with Section 40(b): Dual Compliance Pressure :

Firms must now simultaneously satisfy two independent conditions:

| Provision | Key Requirement |

| Allowability u/s 40(b) | Limits on interest/remuneration, authorization indeed- : Authorization in partnership deed, and Monetary limits on interest and remuneration |

| Tax Deducted at Source compliance under Section 194T | Tax Deducted at Source deduction & timely deposit, Correct deduction, timely deposit, and Accurate reporting |

Crucially, compliance with Section 40(b) does not insulate the firm from consequences u/s 194T. A remuneration that is perfectly allowable u/s 40(b) may still attract interest, penalty exposure, or disallowance if TDS obligations are missed. Allowability under 40(b) does not protect the firm from disallowance due to non‑Tax Deducted at Source under 194T.

Strategic Choice: Retain Profits or Pay Remuneration?

- From a tax efficiency perspective, firms are subject to a flat tax rate (plus surcharge and cess); partners are taxed individually, often at lower effective average rates, and paying remuneration (within Section 40(b) limits) can reduce overall tax outflow, even after factoring in Tax Deducted at Source.

- However, the cash‑flow impact of Tax Deducted at Source deductions, refund timelines, and compliance discipline must now be factored into this decision. Section 194T therefore pushes firms to replace year‑end tax engineering with advance, structured planning.

- Decision Rule

Situation Decision Partner tax < Firm tax Pay remuneration Partner tax ≈ Firm tax Neutral (decide based on cash flow) Partner tax > Firm tax Retain profit

- Non‑compliance can result in interest, penalties, possible legal action, reputational damage, and disallowance of otherwise allowable partner payments, increasing the firm’s tax burden.

Why Strategic Planning Is Essential

- Firms without prior Tax Deducted at Source obligations must apply for a TAN in advance to avoid compliance delays. Challenges may include documentation gaps, verification issues, administrative delays, and resource constraints, especially for smaller firms. Accounting systems must be updated to identify partner payments exceeding INR 20,000, calculate Tax Deducted at Source at 10%, record deductions correctly, and generate Tax Deducted at Source returns and certificates, along with staff training.

- Cash‑Flow Impact on Partners: Partners who earlier received gross amounts must now factor in immediate Tax Deducted at Source deductions, dependence on refund cycles, or advance tax adjustments. This especially affects senior partners relying on firm income and firms with thin working capital or seasonal cash flows.

- Firms should forecast cash flows factoring Tax Deducted at Source, time partner payments carefully, maintain dedicated Tax Deducted at Source reserves, and actively track refunds to prevent liquidity pressure.

- Consider monthly fixed payouts instead of year‑end lump sums and align remuneration with cash generation cycles. Avoid unnecessary interim credits, and bundle remuneration credits with Tax Deducted at Source‑ready payment cycles. Assist partners in adjusting advance tax liability against Tax Deducted at Source credits and prevent excess refunds or interest u/s 234B/C.

- Revaluate interest rates on partner capital and consider reducing or restructuring to minimize repetitive Tax Deducted at Source load. Ensure the deed clearly specifies the nature and quantum of remuneration, interest computation methodology, and periodicity of accrual/payment.

- Section 194T requires accurate reflection of Tax Deducted at Source deductions, proper disclosure of Tax Deducted at Source liabilities, revised accounting treatment of partner payments, and enhanced audit‑level reporting.

- Since part of a month counts as a full month, even a delay of a day or two can result in interest for multiple months. This transforms Section 194T into a high‑risk compliance provision, where casual accounting practices can quickly become costly.

Why Firms Must Treat Section 194T as a High‑Risk TDS Section :

- Legislative Signal of Section 194T: Section 194T clearly reflects the legislature’s intent to change taxpayer behavior, not merely add another compliance provision. It compels firms to plan partner payouts proactively, integrate accounting, taxation, and cash‑flow decisions, and strengthen internal controls over partner payments, which were earlier treated as internal adjustments.

- Firms that treat this as a routine Tax Deducted at Source requirement risk avoidable tax cost, while those adopting a strategic approach can convert compliance into certainty.

- Section 194T is a high‑risk Tax Deducted at Source provision where minor lapses in partner payment compliance can trigger disallowance, higher tax costs, and reputational damage despite the expenditure being otherwise allowable.

- Section 194T is not a routine withholding provision; it is a high‑risk compliance area where even minor procedural lapses can lead to disproportionate financial and reputational costs for the firm.

- To manage Section 194T efficiently, firms should spread remuneration payments across the year rather than back‑loading them; align partner payouts with cash‑flow planning; review interest rates on partner capital; audit partnership deeds for clarity on the nature, timing, and computation of payments; and educate partners on Tax Deducted at Source credit utilization and advance‑tax alignment.

- Payments to partners are no longer insulated from Tax Deducted at Source discipline. This change demands earlier decision-making, cleaner accounting practices, and a cohesive tax-cash-compensation strategy.

- Section 194T marks a decisive shift from informal partner payouts to disciplined, integrated tax, cash‑flow, and compensation planning, rewarding proactive compliance and penalising routine, last‑minute approaches with avoidable costs and disputes.

- Firms that adapt early will avoid interest costs and litigation, while delayed adaptation may turn routine year‑end entries into costly oversights.

Non-compliance of Section 194T :

- This transforms a compliance lapse into a direct tax cost. Unlike contractors or professionals, Tax Deducted at Source Partners are internal stakeholders. Errors are often noticed only at the assessment stage, and disallowance impacts profitability optics and partner confidence.

- The most dangerous scenario is when payment is allowed under 40(b) but disallowed under 40(a)(ia) due to missed Tax Deducted at Source.

- Section 194T operates independently of deductibility u/s 40(b), making Tax Deducted at Source compliance mandatory even where payments may be disallowable or allowable. Noncompliance can potentially trigger disallowance implications under Section 40, reinforcing that partner payments are no longer insulated from Tax Deducted at Source discipline and require strict procedural compliance

- Interest Liability: Late deduction attracts 1.25% per month, and late deposit attracts 1.5% per month. The consequences of delay are disproportionately severe when compared to the nature of the default. Interest u/s 201(1A) is levied at 1% per month for delay in deduction and 1.5% per month for delay in deposit.

- Expense Disallowance: 30% of partner payments may be disallowed under Section 40(a)(ia). Disallowance u/s 40(a)(ia): Failure to deduct or deposit Tax Deducted at Source leads to 30% disallowance of such expenditure in the firm’s computation and increased tax outgo despite payment being genuine and allowable under Section 40(b).

- Penalties & Prosecution: Penalty equal to the TDS amount not deducted may be levied under Section 271C, with possible imprisonment ranging from 3 months to 7 years.

- Late Certificate Fee: Failure to issue Form 16A attracts a penalty of INR 100 per day.

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.