What Changes on the TDS Portal from April 1, 2026?

Table of Contents

Tax Deducted at Source Framework Changing from 01.04.2026

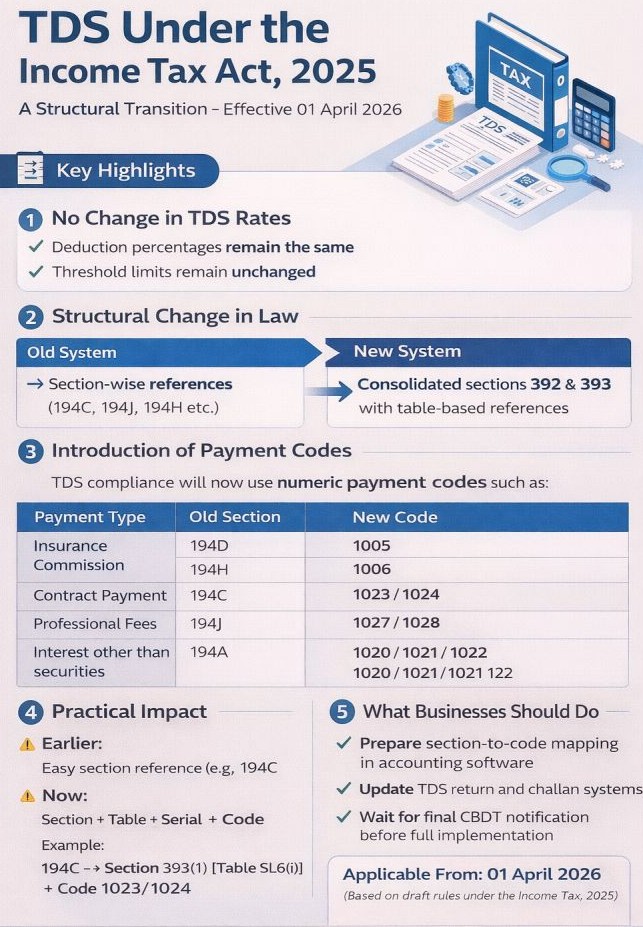

Under the Income Tax Act, 2025, the government is implementing a complete reorganisation of the Tax Deducted at Source framework effective 01 April 2026. The Income Tax Act, 1961 stands repealed w.e.f. 01.04.2026, and the Income Tax portal has already begun displaying transition-related updates. This shift is less about visual redesign and more about a new compliance backbone that will affect terminology, processes, filing structures, and correction timelines. This is a structural and compliance-level overhaul, not a change in tax liability. Key Highlights of the New Tax Deducted at Source System

- No change in existing tax-deducted-at-source rates

- No change in threshold limits

- Major overhaul of section references.

- Traditional sections like 194C, 194J, 194H, etc. will be replaced by table-based referencing

- Deductors will refer to new classification tables instead of existing section numbers

New Payment Code Structure (1001–1067) :

The new Tax Deducted at Source system uses numeric payment codes instead of section numbers. Purpose of New Codes

- Used for Tax Deducted at Source challans, Tax Deducted at Source return filing, and reporting.

- Replaces the earlier section-wise identification.

- Ensures alignment with the new table-based structure.

- Examples mentioned in draft rules codes like 1001, 1005, and 1023 appear in draft compliance formats for use in e-payment and reporting.

- The Income Tax Act, 2025, takes effect from 01.04.2026. The Tax Year replaces the AY/PY; 31.03.2026 is the final cutoff for old Tax Deducted at Source or Tax Collected at Source corrections. Updated return utilities are already available on the portal. Portal changes reflect a new compliance architecture, not a UI redesign. Early preparation helps avoid irreversible issues

- Before April 1, 2026, check if any older Tax Deducted at Source or Tax Collected at Source correction statements are pending, evaluate whether an updated return is applicable, Keep an eye on official portal announcements, and understand the new “Tax Year” structure. The goal is not panic but only timely preparation.

TDS Reporting Changes for FY 2026–27 :

- All organisations, finance teams, accountants, and ERP vendors should prepare for a smooth migration to the new framework by early 2026. India’s income tax system enters a new legal era from April 1, 2026. Tax Deducted at Source Return Filing Will Use New Codes & Table References. Tax Deducted at Source statements will no longer use 194-series sections. Challans/Q Tax Deducted at Source statements (Form 24Q/26Q equivalents) will shift to the new numeric codes. The government will initially operationalize 54 new forms under the Income Tax Act, 2025, starting April 1, 2026.

- The Income Tax Act, 2025, becomes operational from April 1, 2026. Key intent of the new Act Simplified language, Removal of obsolete provisions, and a more streamlined compliance structure. Introduction of “Tax Year.” One of the most significant conceptual changes is replacing “Assessment Year” and “Previous Year” with a single term—Tax Year.

TDS Return Filing Due Dates Revised : Starting Tax Year 2026–27:

- 31 July – Individuals (simple returns)

- 31 August – Non-audit businesses & partners

- 31 October – Companies/audited cases

- 30 November – Special cases

TDS Old vs. New Section Mapping

The Income Tax Act, 2025 removes the traditional Tax Deducted at Source sections (e.g., 194C, 194J, 194H) and replaces them with consolidated sections supported by table-based classifications. Structural change is like the old law (ITA 1961), which had individual TDS sections for each payment type. New law (ITA 2025) consolidates deductions mainly under sections 392 and 393, with payments defined by table no. & serial number. Examples of Mapping

| Old Section (ITA 1961) | Description | New Reference (ITA 2025) |

| 194C | Contract payments | Section 392 – Table reference (specific Sl. No.) |

| 194J | Professional/technical fees | Section 392 – Table reference |

| 194H | Commission/brokerage | Section 392 – Table reference |

| 194IA, 194IB | Property purchase, rent | Mapped to specific serial numbers under consolidated sections |

Only the referencing format changes — rates & thresholds remain exactly the same.

Tax Deducted at Source or Tax Collected at Source Correction Deadline

The Income Tax portal prominently announces a hard deadline:

- The “change on the portal” is fundamentally a shift in the legal and reporting architecture, not a redesign of the website. Core priority is to File all old Tax Deducted at Source or Tax Collected at Source correction statements before 31.03.2026. From 01.04.2026. All historical years become completely unrectifiable. No correction will be accepted, even for genuine errors.

- 03.2026 for Tax Deducted at Source or Tax Collected at Source correction statements from FY 2018–19 Q4 to FY 2023–24 Q3. From 01.04.2026, corrections for these years become time‑barred because the 1961 Act is repealed. Under the new Act (Section 397(3)), corrections for future years will be allowed only within two years from the end of the relevant Tax Year. So Employers, businesses, clinics, deductors, and accountants must clean up old discrepancies before the deadline. After April 1, 2026, correction windows close permanently for all historical years. The real risk is not ignorance it is delay.

Common Mistakes related to TDS

Common Mistakes to Avoid like Assuming nothing changes except the portal UI, waiting for a visual redesign instead of addressing compliance, ignoring older Tax Deducted at Source or Tax Collected at Source mismatch cleanup and Mixing confirmed rules with proposed changes. The transition is legal + procedural, not just aesthetic.

Remaining forms will be rolled out gradually through FY 2026–27.

Introduction of New Payment Codes (1001–1067) : These will be used for Tax Deducted at Source challans, statements, and reporting. Accounting software and ERP systems will require timely updates. This transition does not alter tax-deducted-at-source obligations, rates, or exemptions. However, deduction, reporting, compliance, and software mapping methods will change significantly under the Income Tax Act, 2025.

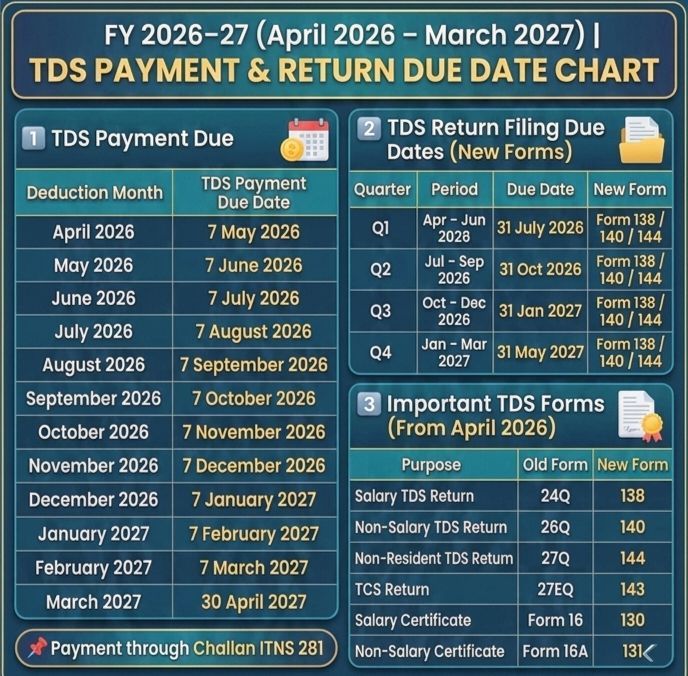

TDS Payment & Return Due Dates – FY 2026–27

Staying compliant with Tax Deducted at Source (TDS) deadlines is essential for businesses, employers, and professionals. Below is a clear and updated summary of TDS payment timelines, quarterly return due dates, and new TDS/TCS forms applicable from April 1, 2026 under the new Income Tax Act, 2025.

TDS Payment Due Dates

Monthly Due Dates : TDS deducted in any month must be deposited by the 7th of the following month using Challan ITNS 281.

Special Case – March 2027 : TDS deducted in March 2027 must be deposited on or before 30 April 2027.

Quarterly TDS Return Filing Deadlines (FY 2026–27)

| Quarter | Period | Return Due Date |

|---|---|---|

| Q1 | Apr–Jun 2026 | 31 July 2026 |

| Q2 | Jul–Sep 2026 | 31 Oct 2026 |

| Q3 | Oct–Dec 2026 | 31 Jan 2027 |

| Q4 | Jan–Mar 2027 | 31 May 2027 |

Timely filing ensures Correct credit in Form 26AS / AIS, Avoidance of late fees (₹200/day under section 271H) and No penalty risk for prolonged delay

New TDS/TCS Forms Effective from 1 April 2026

Under the Income Tax Act, 2025, TDS/TCS forms have been renumbered and simplified:

| Purpose | New Form (From Apr 2026) | Earlier Form |

|---|---|---|

| Salary TDS Return | Form 138 | Form 24Q |

| Non-Salary TDS Return | Form 140 | Form 26Q |

| Non-Resident TDS Return | Form 144 | Form 27Q |

| TCS Return | Form 143 | Form 27EQ |

| Salary Certificate | Form 130 | Form 16 |

| Non-Salary TDS Certificate | Form 131 | Form 16A |

These new form numbers will apply in Quarterly TDS/TCS filings, Certificates issued to employees & vendors and ERP & accounting system updates

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.