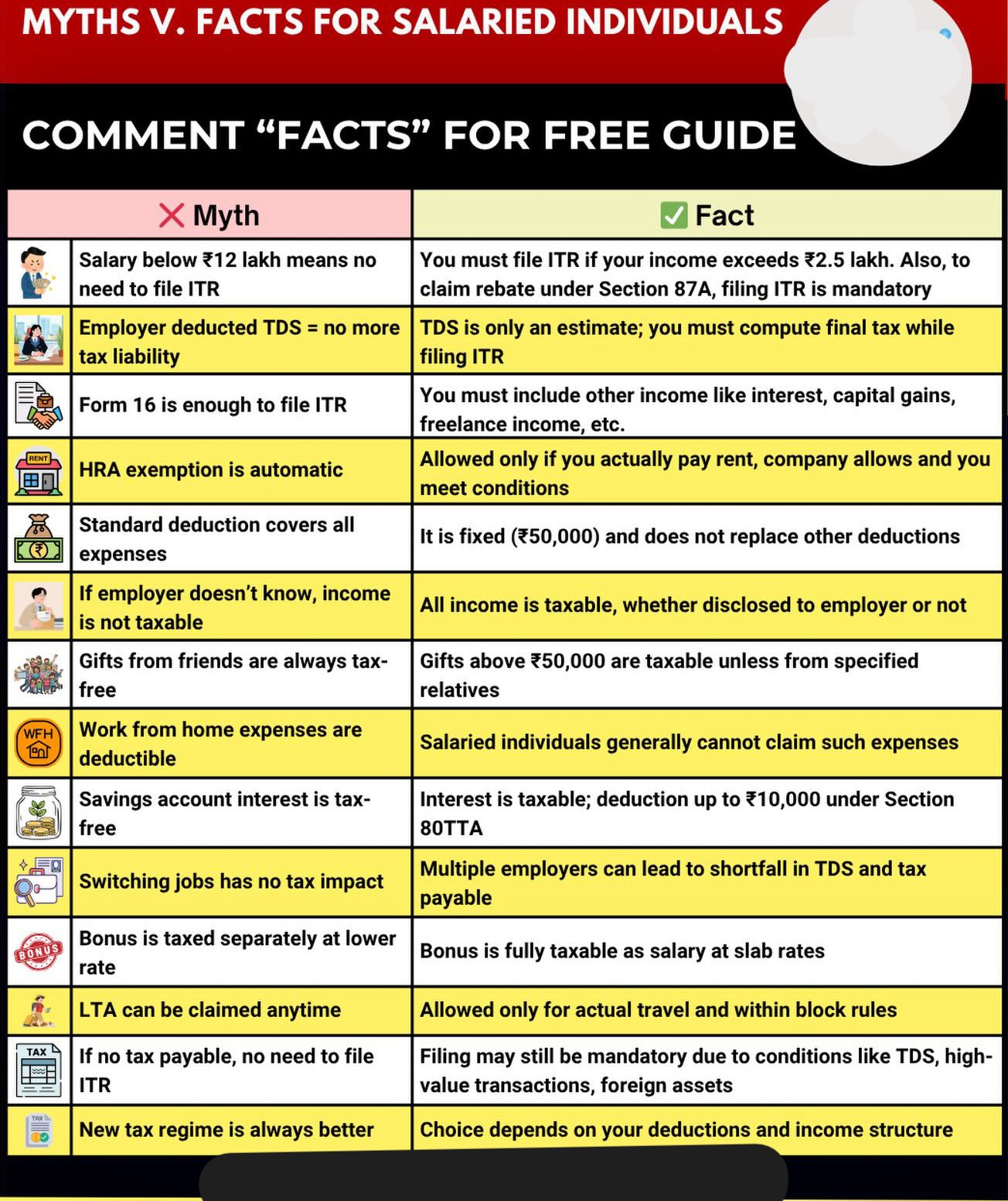

Myth: Low Income Means No Need to File ITR : Not True

Table of Contents

Myth: Low Income Means No Need to File ITR : Not True

Many people believe that if they don’t “earn enough,” they don’t need to file an income tax return (ITR). This myth is widespread — but incorrect. The Truth: Filing Depends on Your Gross Total Income, Not Your Final Taxable Income. You must file your ITR if your Gross Total Income (GTI) before deductions exceeds the basic exemption limits:

- INR 250,000 – Individuals below 60

- INR 300,000 – Senior Citizens (60–80)

- INR 500,000 – Super Senior Citizens (80+)

Even if your final taxable income becomes zero after claiming deductions (like 80C, 80D, NPS), you may still be legally required to file.

Income Tax Filing Thresholds – Summary

Income tax filing thresholds are the income limits specified under the Income Tax Act, 1961, that determine whether an individual must mandatorily file an Income Tax Return (ITR). These thresholds are based on a person’s Gross Total Income (GTI) before claiming deductions under Chapter VI‑A (such as 80C, 80D, etc.).

Basic Filing Thresholds (AY 2026–27)

You must file your ITR if your gross total income exceeds the following:

- INR 2,50,000 – Individuals below 60 years

- INR 3,00,000 – Resident senior citizens (60–80 years)

- INR 5,00,000 – Resident super senior citizens (80+ years)

Even if your final taxable income becomes zero after deductions, the filing requirement is determined before deductions.

You can check official rules and file returns on the Income Tax Department portal: incometax.gov.in

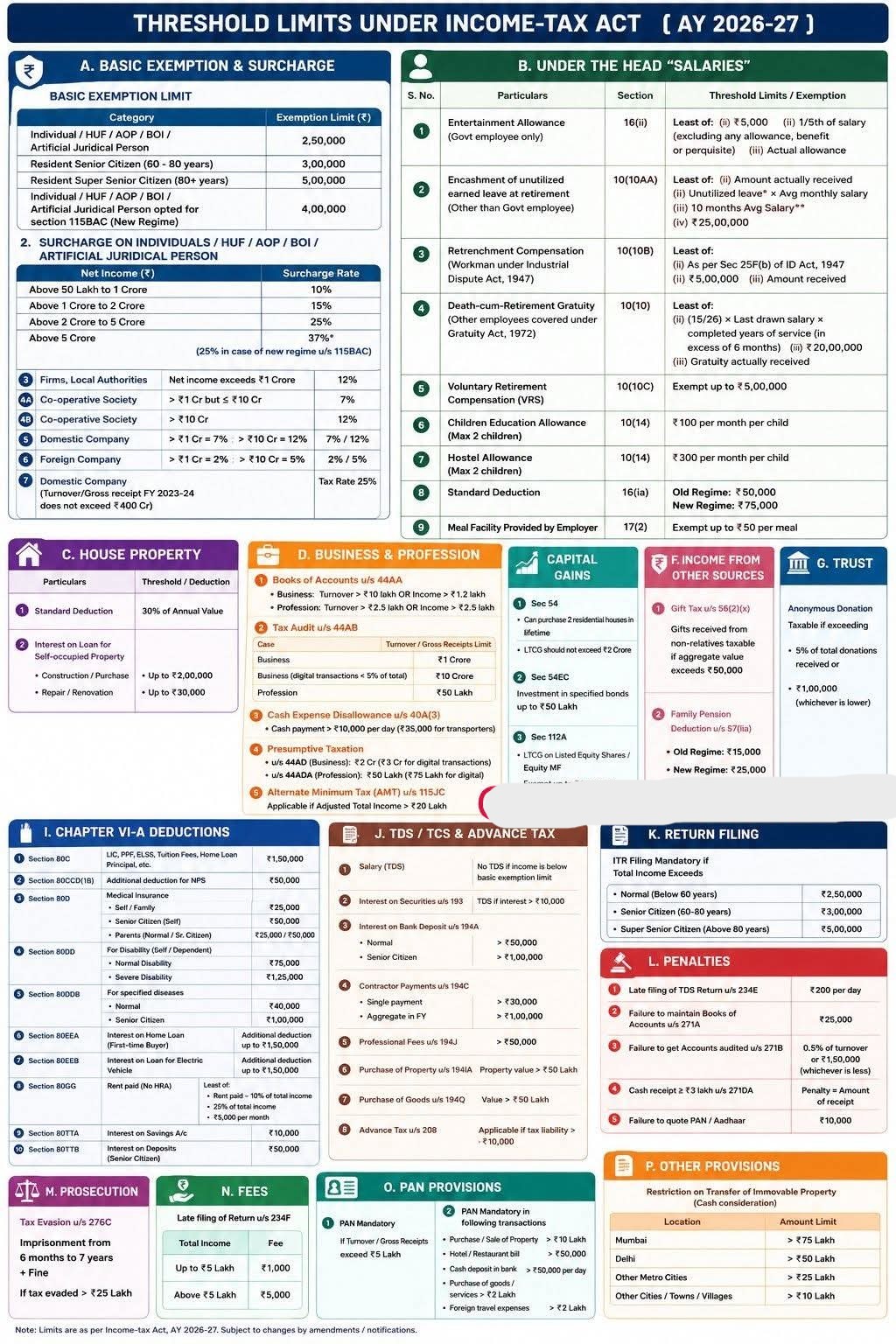

Threshold limits under Income Tax ACT for AY 2026-27

The Income-tax Department has published consolidated Important threshold limits for AY 2026–27 covering exemptions, deductions, TDS, audits, penalties, and filing requirements and deductions under the Indian Income-tax Act for AY 2026–27. few entries require clarification or caution because actual applicability depends on the Finance Act, notifications, and specific conditions. Key highlights are mentioned here under :

Threshold Limits – Income Tax Act (AY 2026–27)

New Tax Regime Slabs – AY 2026–27

| Taxable Income | Tax Rate |

| Up to INR 4 lakh | Nil |

| INR 4 lakh – INR 8 lakh | 5% |

| INR 8 lakh – INR 12 lakh | 10% |

| INR 12 lakh – INR 16 lakh | 15% |

| INR 16 lakh – INR 20 lakh | 20% |

| INR 20 lakh – INR 24 lakh | 25% |

| Above INR 24 lakh | 30% |

Resident individuals under the new regime may get rebate u/s 87A up to INR 60,000 where taxable income does not exceed INR 12 lakh. Salaried taxpayers may effectively have nil tax up to INR 12.75 lakh because of the standard deduction.

Basic Exemption Limit

- Individuals / HUF / AOP / BOI: INR 2,50,000(old regime)

- Resident Senior Citizen (60–80 years): INR 3,00,000

- Resident Super Senior Citizen (80+ years): INR 5,00,000

- New Regime (Section 115BAC): INR 4,00,000 New Regime u/s 115BAC: INR 4 lakh shown in chart (verify with latest Finance Act/official slab notification before use)

Surcharge on Individuals / HUF / AOP / BOI / Artificial Juridical Person

- Income above INR 50 lakh up to INR 1 crore: 10%

- INR 1–2 crore: 15%

- INR 2–5 crore: 25%

- Above INR 5 crore: 37%

(25% cap under new regime in certain cases) - Health & Education Cess: 4% extra

Salaried Individuals – Salary-Related Thresholds

- Entertainment Allowance (Govt employees): Least of INR 5,000 or 1/5th of salary or actual allowance

- Leave Encashment (non-govt): Leave Encashment Exemption: For non-government employees: Least of Actual amount received, 10 months’ average salary, Cash equivalent of leave and Statutory limit : Max INR 3,00,000

- Retrenchment Compensation: Least of section limits or INR 5,00,000 or actual

- Death-cum-Retirement Gratuity: Max INR 20,00,000

- VRS Compensation: Exempt up to INR 5,00,000

- Children Education Allowance: INR 100 per child (max 2)

- Gratuity Exemption: For employees covered under Payment of Gratuity Act: Least of Actual gratuity received and INR 20 lakh and Formula-based calculation

- Hostel Allowance: INR 300 per month per child (max 2)

- Standard Deduction:

- Old regime: INR 50,000

- New regime: INR 75,000

House Property

- Interest on home loan (self-occupied): Up to INR 2,00,000

- Repairs / Renovation interest: Up to INR 30,000

- House Property: Self-Occupied Property Interest: Construction/Purchase: deduction up to INR 2 lakh and Repair/Renovation: up to INR 30,000

- Standard Deduction: 30% of Net Annual Value

Business & Profession

- Books of Accounts (Sec 44AA):

- Business: Turnover > INR 10 lakh or income > INR 1.2 lakh

- Profession: Receipts > INR 2.5 lakh

- Audit Limits (Sec 44AB):

- Business: Turnover > INR 1 crore

- If 95% digital transactions: limit INR 10 crore

- Profession: Receipts > INR 50 lakh

- Business: Turnover > INR 1 crore

- Presumptive Taxation:

- Business (44AD): Turnover ≤ INR 3 crore (if 95% digital)

- Profession (44ADA): Receipts ≤ INR 75 lakh

- Cash Transactions:

- Donations > INR 2,000 – not allowed

- Loans/Deposits > INR 20,000 – restricted

- Cash payments (43A/40A) > INR 10,000 disallowed (INR 35k for transport)

Business & Profession – Tax Audit u/s 44AB :

- In case Business: INR 1 crore normal limit and INR 10 crore where cash receipts/payments are within prescribed limits

- In case Profession: INR 50 lakh

Presumptive Taxation

- u/s 44AD: INR 2 crore (INR 3 crore for eligible digital transactions)

- u/s 44ADA: INR 50 lakh (INR 75 lakh for eligible digital receipts)

Capital Gains

- Section 54: Exemption available on reinvestment in residential house subject to conditions. Exemption u/s 54: Max INR 10 crore

- Section 54EC: Investment in specified bonds: Maximum: INR 50 lakh – NCD / Bonds (54EC): Max investment INR 50 lakh

- LTCG – Equity: Exempt up to INR 1,25,000

Income From Other Sources

- Gift Tax (Sec 56): > INR 50,000 taxable

- Family Pension: Deduction – INR 15,000 or 1/3rd (lower)

Trusts

- Anonymous donations taxable @ 30%

- Max exemption: INR 1,00,000 or 5% of donation (lower)

Chapter VI‑A Deductions

- Section 80C: INR 150,000- Maximum deduction: INR 1.5 lakh, Includes LIC, PPF, ELSS, Tuition fees, Principal repayment of housing loan

- 80CCC: INR 1,50,000

- Section 80CCD(1B): INR 50,000 extra – i.e Additional NPS deduction: INR 50,000

- Section 80D: Medical insurance: FOR Self/family: INR 25,000 AND FOR Senior citizens: INR 50,000

- Section 80DD / 80DDB: Disability and specified disease deductions subject to conditions and certification.

- Sec 80D: INR 25,000 (non-senior) / INR 50,000 (senior)

- Section 80G: Depending on category

- Section 80E – Education Loan: Actual interest

- Sec 80TTA/80TTB: INR 10,000 / INR 50,000

- Section 80U: INR 75,000 or INR 1,25,000 (disability)

(Subject to old regime only)

Limits on Property Purchase in Cash

- Mumbai: > INR 75 lakh

- Delhi: > INR 50 lakh

- Metro cities: > INR 25 lakh

- Other regions: > INR 10 lakh

TDS / TCS / Advance Tax

- Salary TDS: Based on slab

- Interest TDS (194A): If > INR 40,000 (INR 50,000 for seniors)

- Contractor (194C): INR 30,000 single / INR 1 lakh aggregate

- Professional Fee (194J): INR 30,000

- Purchase of Property: TDS u/s 194IA applicable if value > INR 50 lakh

- Advance tax applicable if liability > INR 10,000

- Bank Interest u/s 194A: Non-senior citizens: threshold INR 50,000 shown in chart And Senior citizens: INR 1 lakh. These limits should be cross verified with latest Finance Act amendments because TDS thresholds are frequently revised.

- Advance Tax : Applicable where total tax liability exceeds: INR 10,000

TDS Threshold Limits

| Section | Nature | Threshold |

| 194A | Bank Interest | INR 50,000 |

| 194A | Senior Citizens | INR 1,00,000 |

| 194C | Contractor – Single Payment | INR 30,000 |

| 194C | Aggregate Annual Payment | INR 1,00,000 |

| 194J | Professional Fees | INR 50,000 |

| 194IA | Purchase of Immovable Property | INR 50 lakh |

| 194Q | Purchase of Goods | INR 50 lakh |

Return Filing

PAN is mandatory in cases such as:

- Business turnover above INR 5 lakh

- Property transactions above INR 10 lakh

- Cash deposits above prescribed limits

- Foreign travel expenditure above INR 2 lakh

Return Filing Mandatory if:

- Income exceeds basic exemption

- Deposits > INR 50 lakh

- Foreign travel > INR 2 lakh, etc.

Mandatory filing thresholds shown:

- Normal individual: INR 2.5 lakh

- Senior citizen: INR 3 lakh

- Super senior citizen: INR 5 lakh

However, return filing may still be mandatory in cases involving:

- Foreign assets

- High-value transactions

- TDS claims/refunds

- Deposits/electricity/travel conditions under seventh proviso to section 139(1)

Penalties

Failure to quote PAN/Aadhaar INR 10,000

- Late TDS return: INR 200/day

- Failure to deduct TDS: INR 10,000

- Cash receipts > INR 2 lakh: Penalty = equal amount

- Late Filing Fee u/s 234F: Up to INR 1,000 for income up to INR 5 lakh and other INR 5,000 otherwise

- Failure to Maintain Books u/s 271A: INR 25,000

- Cash Receipt Violation u/s 271DA: Penalty equal to amount received in violation of section 269TH.

Do You Really Need to File Taxes?

Many people believe filing is optional if no tax is due. However, Filing is mandatory if GTI exceeds the basic exemption limit. Filing is also required under various special conditions, even when income is below the basic limit. (e.g., high-value transactions, foreign assets, TDS credits, business turnover, etc.). Filing voluntarily can also be beneficial for loan applications, visa processing, and claiming refunds.

Consequences of Not Filing

Ignoring your filing obligations can lead to:

- Late Filing Fees (Section 234F)

-

- INR 5,000 if total income exceeds INR 500,000

- INR 1,000 if total income is below INR 500,000

- Interest on Unpaid Tax: Interest under Sections 234A, 234B, 234C applies if tax remains unpaid.

- Loss of Refunds : If TDS/TCS was deducted but ITR is not filed, you cannot claim your refund later.

- Inability to Carry Forward Losses: Business loss, capital loss, and other eligible losses cannot be carried forward.

- Difficulty Getting Loans & Visas: Banks and embassies often require ITR copies as income proof.

- Higher Scrutiny Risk: Non-filing may trigger enquiries by the Income Tax Department, especially when AIS/26AS shows activity.

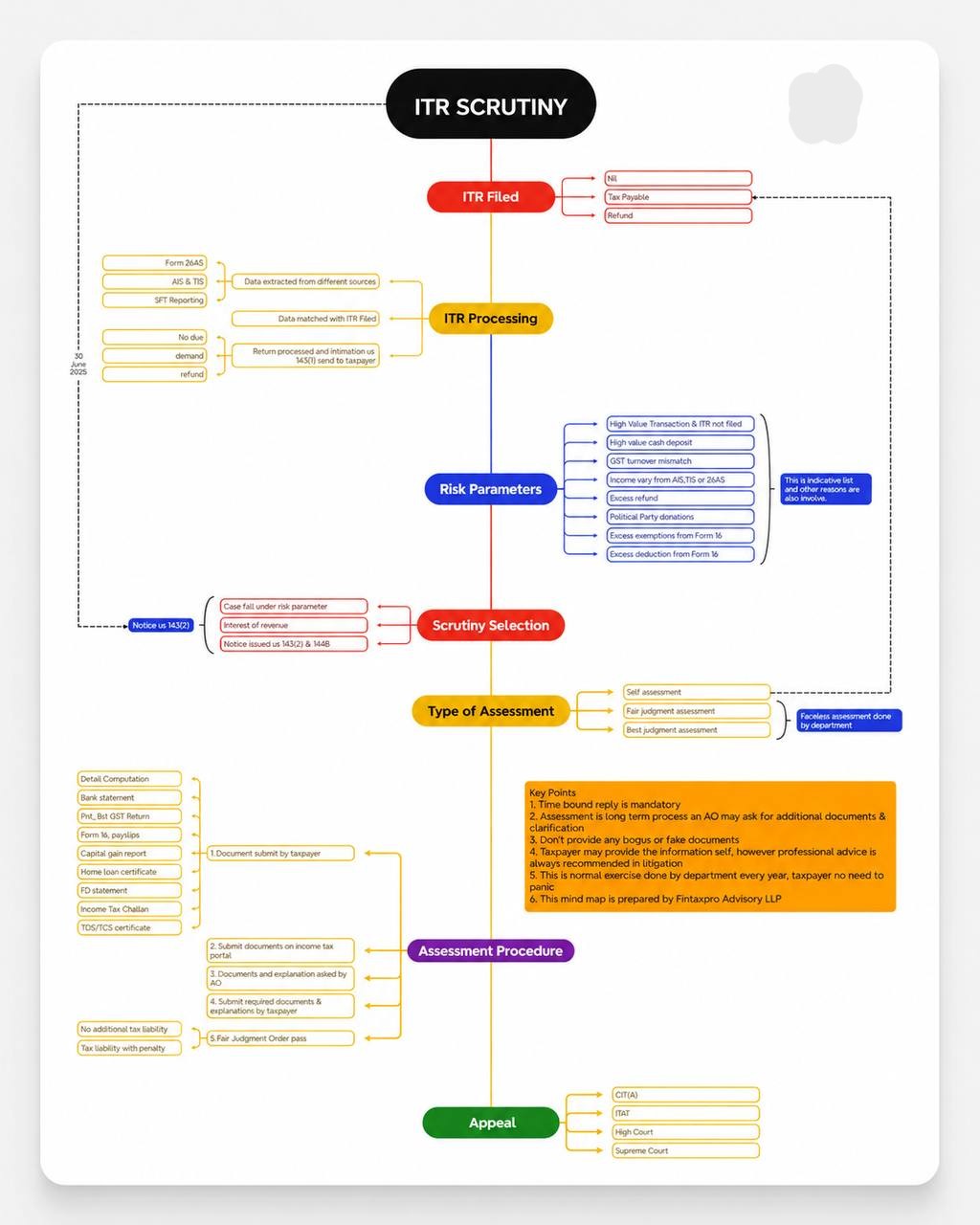

ITR Scrutiny

Why Filing Even at Low Income Is Smart

Filing should not be viewed only as a tax payment requirement. It helps you:

- Prove your income for loans, scholarships, and visas

- Claim refunds on TDS

- Avoid penalties and notices

- Maintain clean compliance records

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.