New Rules Against Mis-selling by Banks: RBI

Table of Contents

RBI’s New Rules Against Mis-selling by Banks: A Major Win for Customers

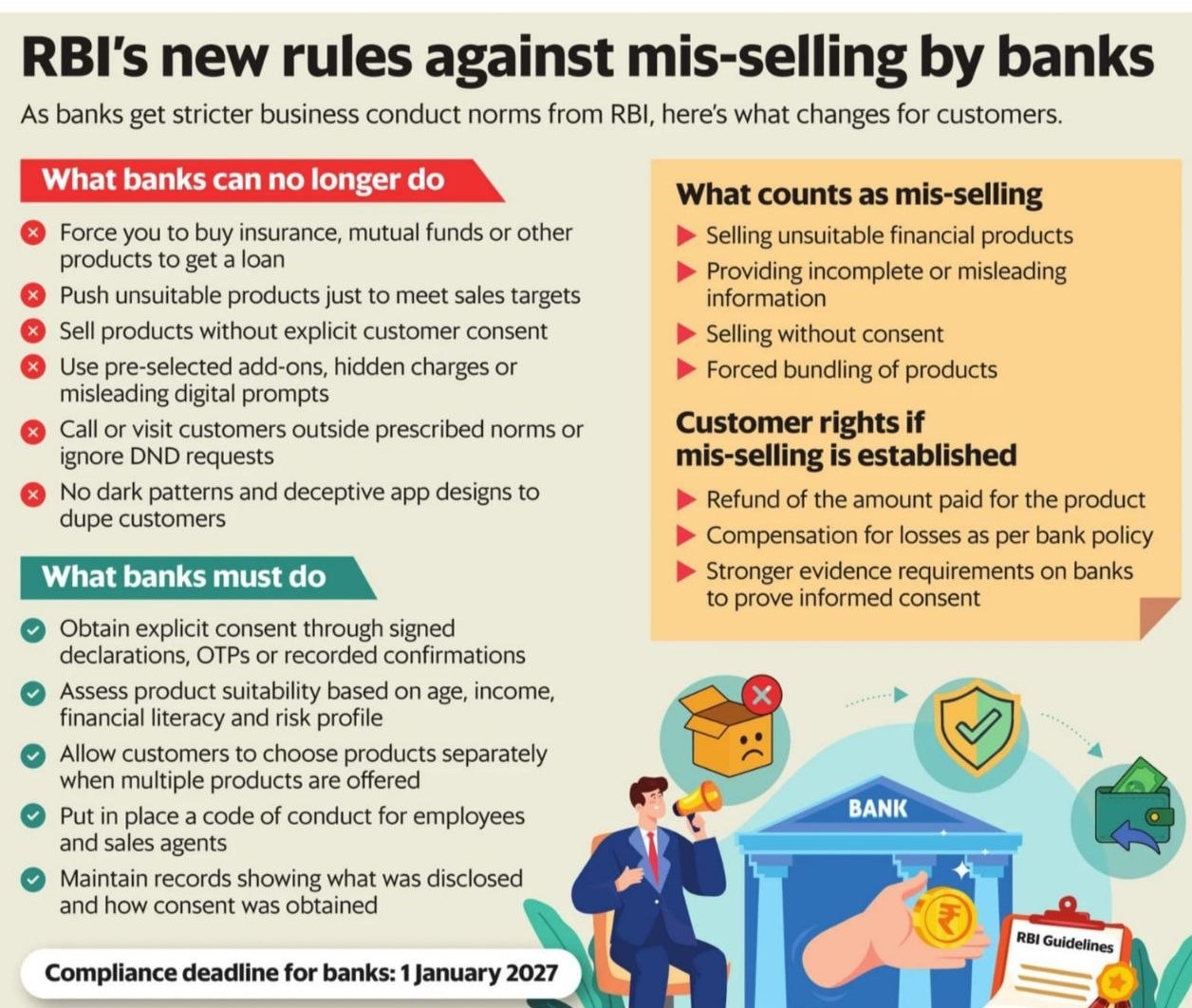

The Reserve Bank of India has introduced a comprehensive framework to curb the widespread issue of mis-selling of financial products by banks. The new regulations aim to ensure that customers purchase financial products only after receiving complete information, giving informed consent, and being assessed for suitability. The Reserve Bank of India rules will significantly strengthen consumer protection and enhance accountability among banks. The compliance deadline for banks is 1 January 2027.

Why Did The Reserve Bank of India Introduce These Rules?

Over the years, customers have frequently complained that banks Forced them to buy insurance products to obtain loans. Sold unsuitable investment products merely to achieve sales targets. Added products without clear consent; used misleading app designs and digital prompts; and bundled multiple products together, making them difficult to refuse.

To address these concerns, RBI has tightened the conduct standards for banks and their sales representatives. The Reserve Bank of India’s new anti-mis-selling framework marks a significant shift from a sales-driven approach to a customer-centric approach in banking. Banks will now be accountable not only for obtaining consent but also for ensuring that products are suitable, fairly explained, and voluntarily chosen by customers. Customers will receive stronger protection through refund rights, compensation mechanisms, and enhanced transparency.

What Banks Can No Longer Do

Under the new framework, banks will not be allowed to:

- Force Customers to Purchase Other Products

A bank cannot insist that a customer buy Insurance policies, Mutual funds, Investment products and Third-party financial products. as a condition for obtaining a loan or any banking service.

- Sell Unsuitable Products

Banks must not recommend products that do not match the customer’s Age, Income, Financial literacy, Investment objectives and Risk tolerance. Simply achieving sales targets cannot justify a product recommendation.

- Sell Without Explicit Consent

Banks can no longer rely on vague authorizations or implied permissions. Every financial product must be sold only after obtaining explicit customer consent.

- Use Hidden Charges and Dark Patterns:

RBI has specifically targeted deceptive digital practices such as pre-ticked checkboxes, hidden fees, false urgency messages, misleading prompts, and difficult cancellation processes. Banks must ensure their websites and mobile applications are free from such practices.

- Compulsory Bundling:

If a customer wants a loan, the bank cannot make the loan conditional upon purchasing another unrelated product. Even where insurance is required as a risk mitigant, customers must be allowed to purchase it from a provider of their own choice.

What RBI Considers as Mis-selling

According to the new framework, misselling includes selling products that are unsuitable for a customer and providing incomplete, inaccurate, or misleading information. Banks are selling a product without explicit consent. And Bank has compulsory bundling of products. Any other activity categorized as mis-selling by the relevant financial sector regulator. Importantly, even if the customer has given consent, the sale may still be considered mis-selling if the product was unsuitable for that customer’s profile.

Practical Examples of Mis-selling by Banks

Example 1: Loan-Linked Insurance

- Old Practice: “Buy this insurance policy or your loan may not be approved.”

- New Rule: Such forced selling may be treated as mis-selling. The customer must be free to purchase insurance from any eligible insurer.

Example 2: Investment Product for Senior Citizen

- A conservative senior citizen seeking a fixed deposit is persuaded to invest in a high-risk market-linked product. This may constitute mis-selling because the product is unsuitable for the customer’s risk profile.

Example 3: Pre-Ticked Mobile App Consent

- A banking app automatically selects an additional insurance cover through a pre-ticked box. This may be considered a prohibited dark pattern and may not qualify as valid consent.

What must banks do for mis-selling avoidance?

- Obtain Explicit Consent

- Consent can be obtained via physical signatures, digital signatures, OTP-based approval, recorded voice confirmations, and clearly separated consent sections in agreements. Consent must be informed, specific, and properly recorded.

- Conduct Suitability Assessment

- Before selling any product, banks must evaluate whether the product is appropriate considering the customer’s age, income level, financial literacy, risk appetite, investment horizon, and product complexity. This shifts responsibility from customers to banks for ensuring suitability.

- Allow Independent Product Choice

- When multiple products are offered Customers must be allowed to select products individually. Consent for multiple products cannot be clubbed together, and separate consent must be obtained for each product.

- Maintain Records

- Banks will be required to maintain proper records showing What information was disclosed, How customer consent was obtained, and why the product was considered suitable. These records may be used during audits, complaints, and regulatory reviews.

- Strengthen Employee Conduct

- Banks must introduce codes of conduct for employees, sales agents, direct selling agents (DSAs), and direct marketing agents (DMAs). The objective is to discourage aggressive and misleading sales practices.

Customer Rights if Mis-selling is Established

- The most significant feature of the new framework is the protection available to customers. If a bank is found guilty of mis-selling,

- Refund of Amount Paid: The bank may be required to refund the entire amount paid for the product or service.

- Compensation for Loss: If the customer suffered financial loss due to the mis-selling, the bank may also have to compensate the customer in accordance with its approved policy.

- Enhanced Burden of Proof on Banks : Banks will need to demonstrate that proper disclosure was made, suitable products were offered, and explicit consent was obtained. This significantly strengthens customer rights.

The message from RBI to banks is clear: Selling financial products is no longer about meeting targets—it is about protecting customer interests and ensuring informed decision-making

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.