No House Rent Allowance, 80GG Can Still Help Save Tax

Table of Contents

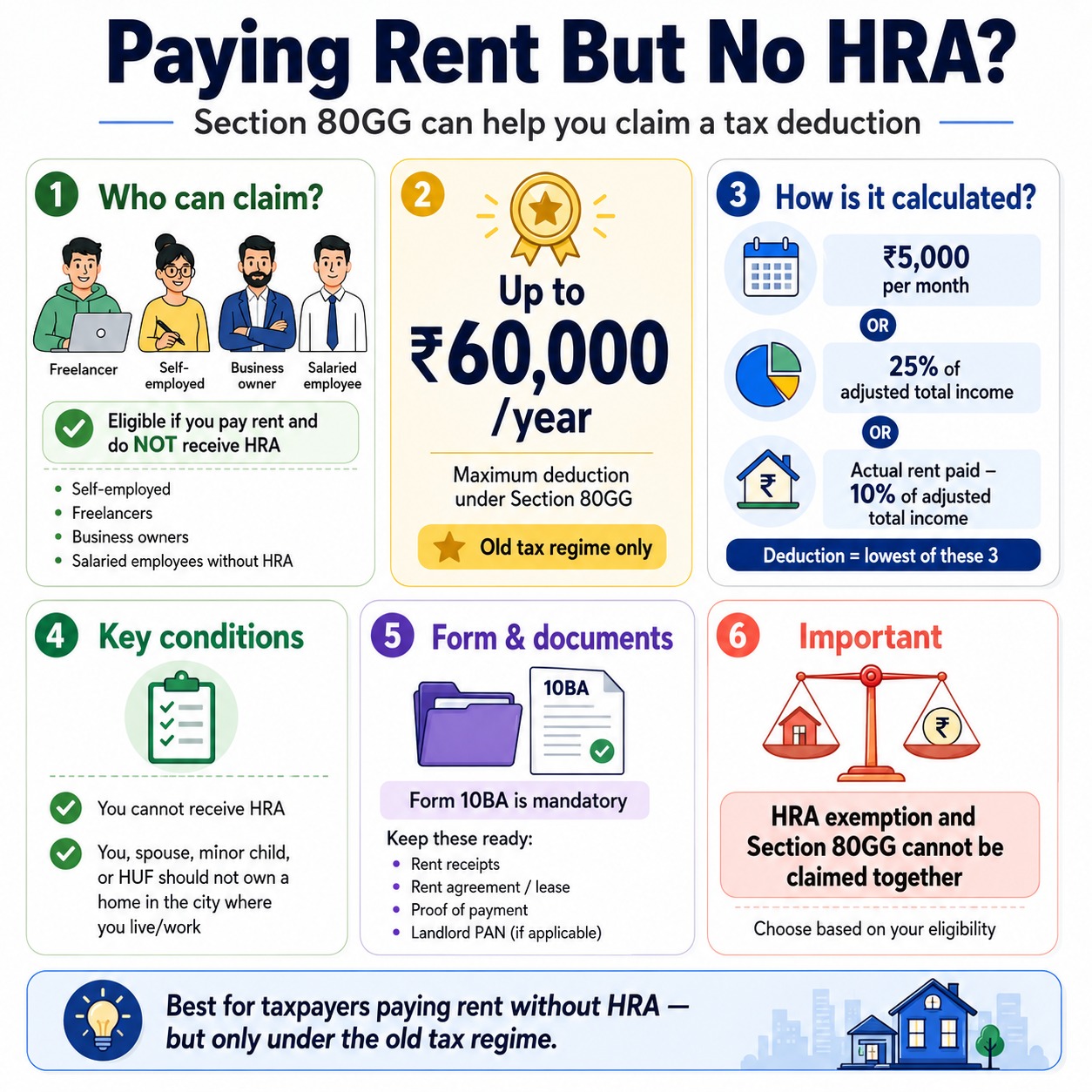

No House Rent Allowance? Section 80GG Can Still Help You Save Tax

Many taxpayers who live in rented accommodation but do not receive House Rent Allowance often miss out on an important tax benefit available u/s 80GG of the Income Tax Act, 1961. This deduction is specifically designed for taxpayers paying rent but not eligible for a house rent allowance exemption.

Who Can Claim Section 80GG?

- Self-employed individuals

- Freelancers and consultants

- Business owners and professionals

- Salaried employees who do not receive House Rent Allowance as part of their salary package

Deduction Available U/s 80GG

The deduction is restricted to the least of the following three amounts:

- INR 5,000 per month (INR 60,000 per year)

- 25% of Adjusted Total Income

- Actual Rent Paid minus 10% of Adjusted Total Income

Taxpayers cannot claim both a house rent allowance exemption and a deduction u/s 80GG for the same period. For taxpayers paying rent without a house rent allowance exemption, especially self-employed professionals and freelancers, Section 80GG can be an effective tax-saving provision while filing the Income Tax Return under the old tax regime.

Basic Key Conditions Available U/s 80GG

Section 80GG deduction is available only under the Old Tax Regime. To claim the deduction, taxpayers are required to file Form 10BA and satisfy the prescribed conditions. The taxpayer, spouse, minor child, or Hindu Undivided Family must not own a residential property at the place where the taxpayer ordinarily resides, is employed, or carries on a business or profession. Additionally, the taxpayer must have actually paid rent for the residential accommodation occupied.

What are the documents to keep ready?

To support the claim under Section 80GG, taxpayers should maintain rent receipts; a rent agreement or lease deed; proof of rent payment (such as bank transfer, UPI transaction, check, etc.); and the landlord’s PAN, wherever applicable. Maintaining proper documentation and ensuring timely filing of Form 10BA can help taxpayers claim the deduction smoothly and avoid issues during return processing.

- Consistent Rent Payments : Rent should be paid regularly and supported by proper documentary evidence.

- Form 10BA is Mandatory : Failure to file Form 10BA may result in denial of the deduction claim.

- No Double Benefit : taxpayer cannot claim an house rent allowance exemption u/s 10(13A) and a deduction u/s 80GG for the same period.

- Property Ownership Restriction : Taxpayer, spouse, minor child, or HUF should not own a residential property at the place of residence or business.

- Landlord’s PAN : If annual rent exceeds INR 1 lakh, it is advisable to obtain and report the landlord’s PAN while filing the return.

Example: Suppose a self-employed taxpayer has:

- Adjusted Total Income: INR 6,00,000

- Annual Rent Paid: INR 1,20,000

Calculation:

- INR 5,000 × 12 = INR 60,000

- 25% of INR 6,00,000 = INR 1,50,000

- INR 1,20,000 – 10% of INR 6,00,000 = INR 60,000

Eligible deduction = INR 60,000 (being the lowest of the above three amounts).

Conclusion

House rent allowance exemption u/s 10(13A) and deduction u/s 80GG cannot be claimed simultaneously for the same period. Taxpayers must choose the benefit applicable to their circumstances. Paying rent but no house rent allowance ? Don’t miss Section 80GG. Filing Form 10BA, maintaining proper rent records, and claiming the deduction correctly in your ITR can help reduce your tax liability and maximize your tax savings.

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.