All about TDS Lower Deduction Certificate provision

Table of Contents

Completed Understanding the Lower Deduction Certificate of TDS

A Lower Deduction Certificate of Tax Deducted at Source is a certificate issued under Section 197 of the Income Tax Act, 1961. It allows a taxpayer to have tax deducted at a lower rate or not at all, under specific conditions. Here’s a detailed breakdown of Section 197 Lower Deduction Certificate of TDS provision:

Objective of Section 197 Lower Deduction Certificate of TDS :

Section 197 enables a taxpayer to receive payments with either a lower rate of Tax Deducted at Source or no Tax Deducted at Source at all. The Lower Deduction Certificate of TDS provision is particularly beneficial for taxpayers who anticipate that their total income tax liability for the financial year will be lower than the rate at which tax is normally deducted at source.

Income Covered U/s 197 of the Income Tax Act

- Taxpayers whose income falls under the following categories can file an application under Section 197 for Nil or lower deduction of Tax Deducted at Source (TDS) i.e Salary Income, Interest on Securities, Dividends, Interest Other than Interest on Securities, Contractors’ Income, Insurance Commission, Fee for Professional or Technical Services, Compensation on Acquisition of Immovable Property, Income with Respect to Units of Investment Fund, Commission/Remuneration/Prize on Lottery Tickets, Commission or Brokerage, Rent, Income of Non-Residents, Income in Respect of Investment in Securitization Trust.

Application of Lower Deduction Certificate of TDS

Any person can apply for a Nil or Lower Tax Deducted at Source certificate. Common scenarios where applications are made include:

- Loss-making businesses that do not have taxable income.

- Businesses with profit margins lower than the standard rate of tax deduction.

- Taxpayers carried forward losses that can offset future income.

Application Process of Lower Deduction Certificate of TDS

Step 1 : Taxpayer has to apply for a Lower Deduction Certificate to respective AO, the taxpayer must furnish various details and documents, such as:

- Scan Copy of PAN and address proof of the deductee.

- Copy of TAN and PAN of the deductor.

- Signed and filled Form 13 (the application form for a lower/NIL Tax Deducted at Source certificate).

- Copies of ITRs for the last three years.

- Original Letter of Authority (if applying via a representative).

- Copies of the Balance Sheet, Statement of Profit & Loss Account, and Audit Report for the last three years.

Step 2 : The Assessing Officer reviews the application to determine the existing and estimated tax liability.

Following basic step involves to be taken by AO to close the Lower Deduction Certificate of TDS.

- Assessing Officer make appropriate assessing the taxpayer’s existing and projected income for the current FY.

- AO Considering any tax payable on the estimated income of taxpayer.

- Assessing Officer reviews & Disposing of the application within 30 days of receipt.

Usage & Validity of Lower Deduction Certificate of TDS

- Once issued, the Lower Deduction Certificate must be attached to the invoices raised to the deductor. This justifies the lower rate of tax deduction or nil deduction when payments are made.

- The Lower Deduction Certificate of TDS certificate is only valid for the assessment year mentioned on it. Taxpayers must reapply each year if they wish to continue receiving the benefit of lower or nil Tax Deducted at Source in subsequent years.

This provision helps taxpayers manage their cash flows more efficiently by reducing the immediate tax outgo and aligning the Tax Deducted at Source with their actual tax liability.

What are the Situations Where a Lower Deduction Certificate is Beneficial or recommended?

Obtaining a Lower Deduction Certificate u/s 197 of the Income Tax Act, 1961, can be highly beneficial in various situations. Here are some common scenarios where an LDC can provide significant advantages:

- Businesses that are incurring losses may not have any taxable income for the year. An Lower Deduction Certificate prevents unnecessary Tax Deducted at Source deductions, improving cash flow and reducing administrative burden.

- Assessees who have carried forward losses from previous years to offset against future income can benefit from an Lower Deduction Certificate. It ensures that tax is not deducted on income that will be set off against these losses.

- Assessees with a net total income below the applicable basic exemption limit (e.g., senior citizens, individuals with no significant income) can avoid Tax Deducted at Source deductions that they would otherwise have to claim back through a refund.

- Non-resident sellers of property in India can benefit from an Lower Deduction Certificate when receiving payments from Indian buyers. This avoids high TDS rates and potential cash flow issues, as the non-resident might have lower tax liability or might be eligible for capital gains exemptions.

- Foreign companies receiving payments from Indian customers, where the foreign company does not have a Permanent Establishment in India, can use an Lower Deduction Certificate to avoid higher Tax Deducted at Source rates u/s 195. This ensures compliance with Indian tax laws while avoiding excess tax withholding.

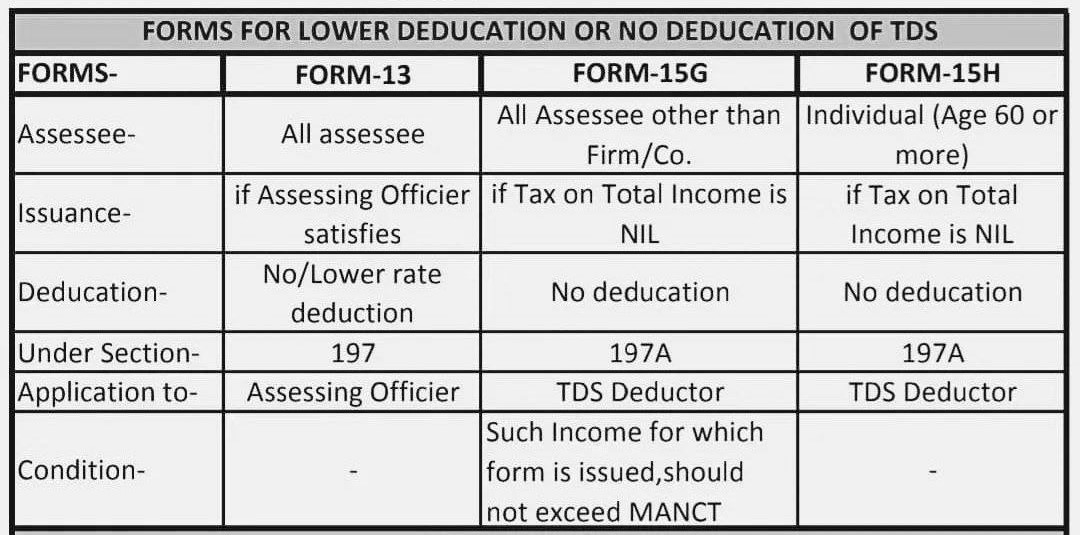

Forms for Lower Deduction and Non-Deduction of TDS

Non-Deduction of Tax Deducted at Source

- Income Tax Forms Required: Income tax Form 15G and Form 15H. Objective of filling if Form 15G & Form 15H is to declare that no Tax Deducted at Source should be deducted since individual’s total income is below the taxable limit. For filling Procedure of Form 15G & Form 15H, we needed to submit required form to the bank or financial institution where the fixed deposit or other income-generating account is held.

- Usage:

- Income tax Form 15G: For individuals below 60 years of age and HUF.

- Income tax Form 15H: In case an individuals who are 60 years and above (senior citizens).

Lower Deduction of Tax Deducted at Source

- Form Required: Form 13 – Objective of filling if form 13 is to apply for Nil/Lower deduction of Tax Deducted at Source (TDS). An application must be filed with the Income Tax Officer using Form 13. Upon satisfaction, the tax officer issues a certificate under Section 197 for lower deduction of Tax Deducted at Source.

- In Summary we can say that Lower Deduction of Tax Deducted at Source: Apply using Form 13 to the Income Tax Officer for a certificate under Section 197. Non-Deduction of Tax Deducted at Source: Submit Form 15G (for individuals below 60 and HUFs) or Form 15H (for senior citizens) to the bank or financial institution.

Expert Assistance with Lower Deduction Certificate Application

You may face navigating the complex process of obtaining an Lower Deduction Certificate can be challenging. Our team at Rajput Jain & Associates Chartered Accountants is equipped to help you through every step of this process. We ensure that you benefit from lower or nil Tax Deducted at Source rates, optimizing your tax position and improving your financial management. Our Services Include:

- Evaluating your financial situation to determine eligibility for an Lower Deduction Certificate.

- Assisting with the collection and preparation of required documents, such as PAN, TAN, Form 13, ITR copies, balance sheets, and profit & loss statements.

- Filing the application on your behalf and handling any follow-up with the Assessing Officer (AO).

- Providing ongoing support to ensure compliance with tax regulations and advising on best practices to minimize tax liability.

Contact us today to learn more about how we can assist you in obtaining a Lower Deduction Certificate and enhance your financial efficiency.

Comprehensive study about TDS & TCS chapter

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.