Comparison of ITR-U & Condonation of Delay u/s 119(2)(b)

Table of Contents

Differences Between Updated Return (ITR-U) and Application for Condonation of Delay u/s 119(2)(b):

Amendments in Budget 2025 for ITR-U

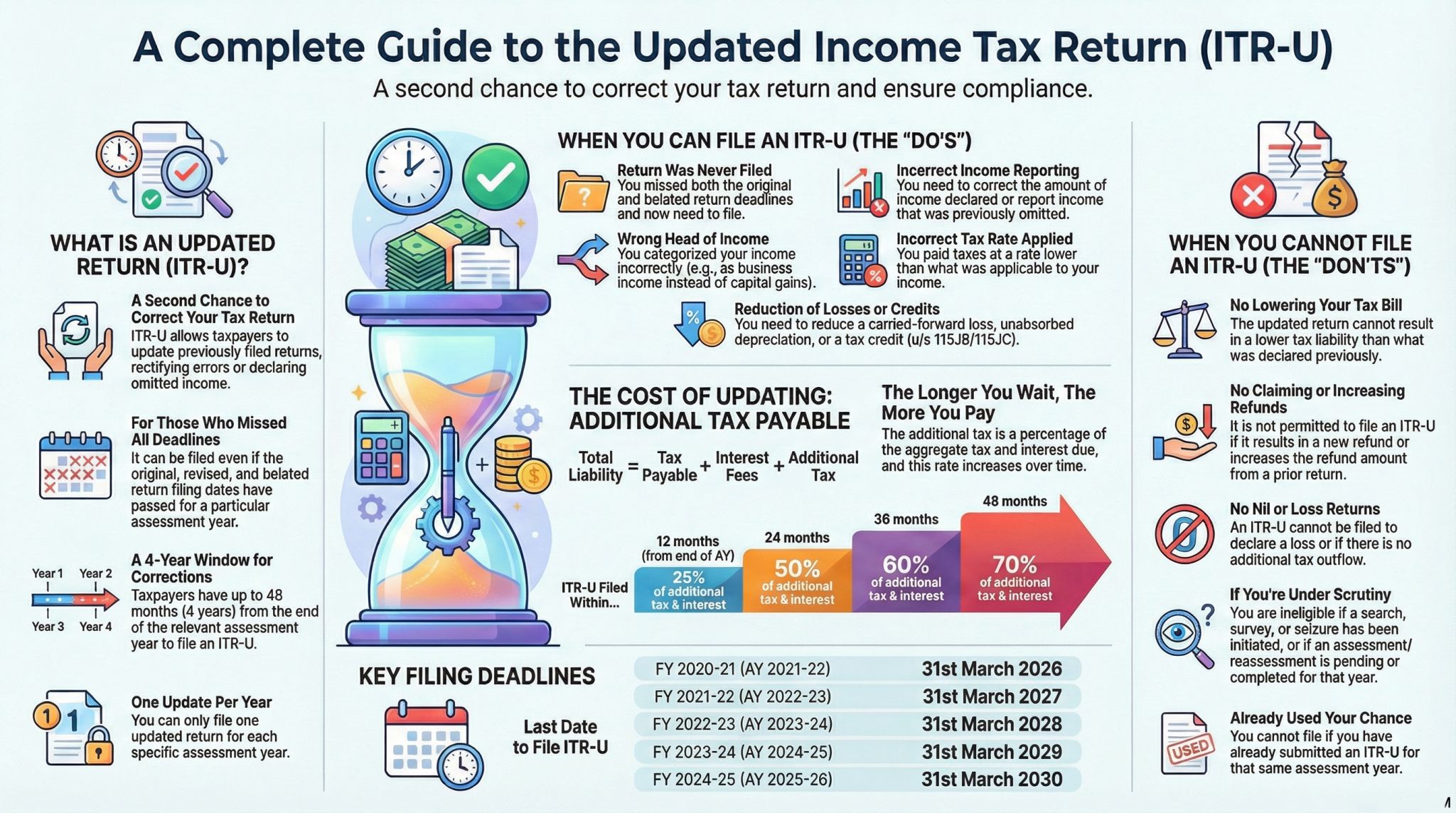

Previously, taxpayers had 2 years from the end of the relevant assessment year to file an updated return (ITR-U). Budget 2025 extends this period to 4 years, providing more time for taxpayers to correct omissions and errors. The extension to 4 years allows taxpayers more flexibility to rectify errors. However, the penalty structure discourages excessive delay by imposing higher additional tax for late filings. The ITR-U mechanism, introduced in Budget 2022, now becomes a stronger compliance tool under Budget 2025, helping taxpayers avoid scrutiny while regularizing past income disclosures. Revised Additional Tax Structure: The additional tax liability now increases progressively based on the delay in filing:

- Within 12 months: 25% of the additional tax and interest due.

- Within 24 months: 50% of the additional tax and interest due.

- Within 36 months: 60% of the additional tax and interest due.

- Within 48 months: 70% of the additional tax and interest due.

Comparison of Updated Return (ITR-U) u/s 139(8A) & Condonation of Delay u/s 119(2)(b).

Here are a few minor refinements for clarity and readability

Objective and Purpose Updated Return (ITR-U) & Condonation of Delay u/s 119(2)(b)

Basic Objective and Purpose ITR-U (Section 139(8A)) : Allows taxpayers to voluntarily update their income tax return if they missed reporting income or underreported earnings in previous filings. However Objective and Purpose Condonation of Delay (Section 119(2)(b)) is A relief mechanism that allows taxpayers to file an ITR after the due date if they have a valid reason for the delay.

Scope of ITR-U & Application for Condonation of Delay

- ITR-U : Can be filed by any taxpayer (individual, company, firm, etc.) to disclose additional income that was missed earlier. ITR U Can be filed even if no original, belated, or revised return was filed. Cannot be used if:

- It results in a refund or an increase in losses.

- The taxpayer is under assessment, reassessment, or investigation.

- The case involves search, survey, prosecution, or undisclosed income.

- Condonation of Delay : Condonation of Delay : Only applies when no ITR was filed at all within the prescribed time. Condonation of Delay Requires a valid reason for the delay. Condonation of Delay Approval is at the discretion of CBDT or Principal Chief Commissioner of Income Tax (PCCIT). Unlike ITR-U, a condonation request can be used to claim a refund. Common reasons include:

- Forgetting to file due to unavoidable circumstances.

- Wanting to claim a refund that was missed.

- Genuine hardship (e.g., medical emergency, natural calamities).

Time Limit for Filing of ITR-U & Application for Condonation of Delay

- ITR-U : Current limit: 24 months from the end of the relevant AY. And in the Proposed (Budget 2025), The Budget 2025 proposes to extend this to 48 months (4 years). ITR U Increase to 48 months from the end of the relevant AY.

- Condonation of Delay: As per CBDT Circular 11/2024 (not 5 years), the request can be made within 6 years from the end of the relevant FY.

Additional Liabilities in Filing of ITR-U & Application for Condonation of Delay

- ITR-U: Requires payment of additional tax. The additional tax is 25% if the return is filed within 12 months and 50% if filed after 12 months but before the due date. There is no 70% rate currently applicable. However Condonation of Delay application has No additional tax, but interest u/s 234A, 234B, & 234C and penalties may apply if tax is payable.

Authorities Involved for Filing of ITR-U & Application for Condonation of Delay

- ITR-U: Processed directly by CPC (Centralized Processing Center). And No manual approval required. If valid, it is automatically processed.

- Condonation of Delay: Requires approval from CBDT or PCCIT before filing the return. And Decision must be made within 6 months of the application.

Practical Scenarios on Filing of ITR-U & Application for Condonation of Delay

- Missed ITR deadline with a valid reason—correctly assigned to Condonation of Delay (Section 119(2)(b)). Use Condonation of Delay if: You failed to file your return on time due to a valid reason (such as a medical emergency or oversight) and need to seek approval before filing. However, approval is not guaranteed and depends on the taxpayer proving “genuine hardship.

- Failed to report additional income or correct an error – ITR-U (Section 139(8A)) is the only option, as condonation is not meant for underreporting cases. You missed declaring income and want to update your return, but be prepared to pay additional tax

- Business suffered losses and wants to carry them forward – It is correctly mentioned that ITR-U does not allow loss carry-forward. However, Condonation of Delay is correct, but the taxpayer must meet the conditions for loss carry-forward. condonation of delay allows it only if the taxpayer meets the conditions specified under the Income Tax Act.

- Excess tax deductions and wants a refund—condonation of Delay is correct, but approval depends on the justification for late filing.

- Willing to pay additional tax to update return quickly – ITR-U is correct, as it allows a taxpayer to voluntarily rectify errors without needing approval.

Which is more beneficial?

- Condonation of Delay is preferable only if the taxpayer qualifies and obtains approval. Otherwise, ITR-U remains the only available option for updating income.

CBDT Extends ITR Filing Deadline for AY 2025-26 Circular No.: 06/2025

The CBDT has extended the due date for furnishing the Return of Income under Section 139(1) of the Income-tax Act, 1961 for Assessment Year 2025-26. Dated: 27th May, 2025, Issued by: Central Board of Direct Taxes (CBDT) Reference: F. No. 225/205/2024/ITA-II

- Old Due Date: 31st July 2025

- New Extended Due Date: 15th September 2025

The extension applies to assessees referred to in clause (c) of Explanation 2 to sub-section (1) of Section 139—typically individuals, HUFs, and other non-audit cases.

Reason for Extension of CBDT Extends ITR Filing Deadline for AY 2025-26 is stated as the extension is understood to be due to Revised ITR Forms. And System Overhauls and Portal Updates

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.