NRI Income Tax Help Centre

Table of Contents

NRI Income Tax Help Centre

- In many countries, income tax laws are complicated, and it is quite difficult to understand tax regulations. Many NRIs and foreign nationals working in India need to be aware of basic tax regulations that affect their tax compliance and, in certain cases, plan to lower their taxes.

- India Financial Consultancy Corporation has always been at the forefront of educational NRIs and foreign nationals as a leading portal for providing tax filing solutions and expert tax services. This website is an effort to assist you.

- A individual preferred to stay outside India and to work for years and decades day and night in the family and social circle. The aim is to improve living standards by earning more, looking at available opportunities in his home country. An individual who wants to become Non-Resident Indian (NRI) apparently intends to be able to more effectively meet family needs, education and a comfortable life after retirement.

- After years of living outside of India as the NRI, it is certain that the moment of thinking will emerge and let us return to India. It is the motherland’s call for a break from work and a life after retirement.

- The second reason is that before going back to India, there is plenty to be done. The planning and preparations take a lot of energy and time, particularly when they plan to return for the better.

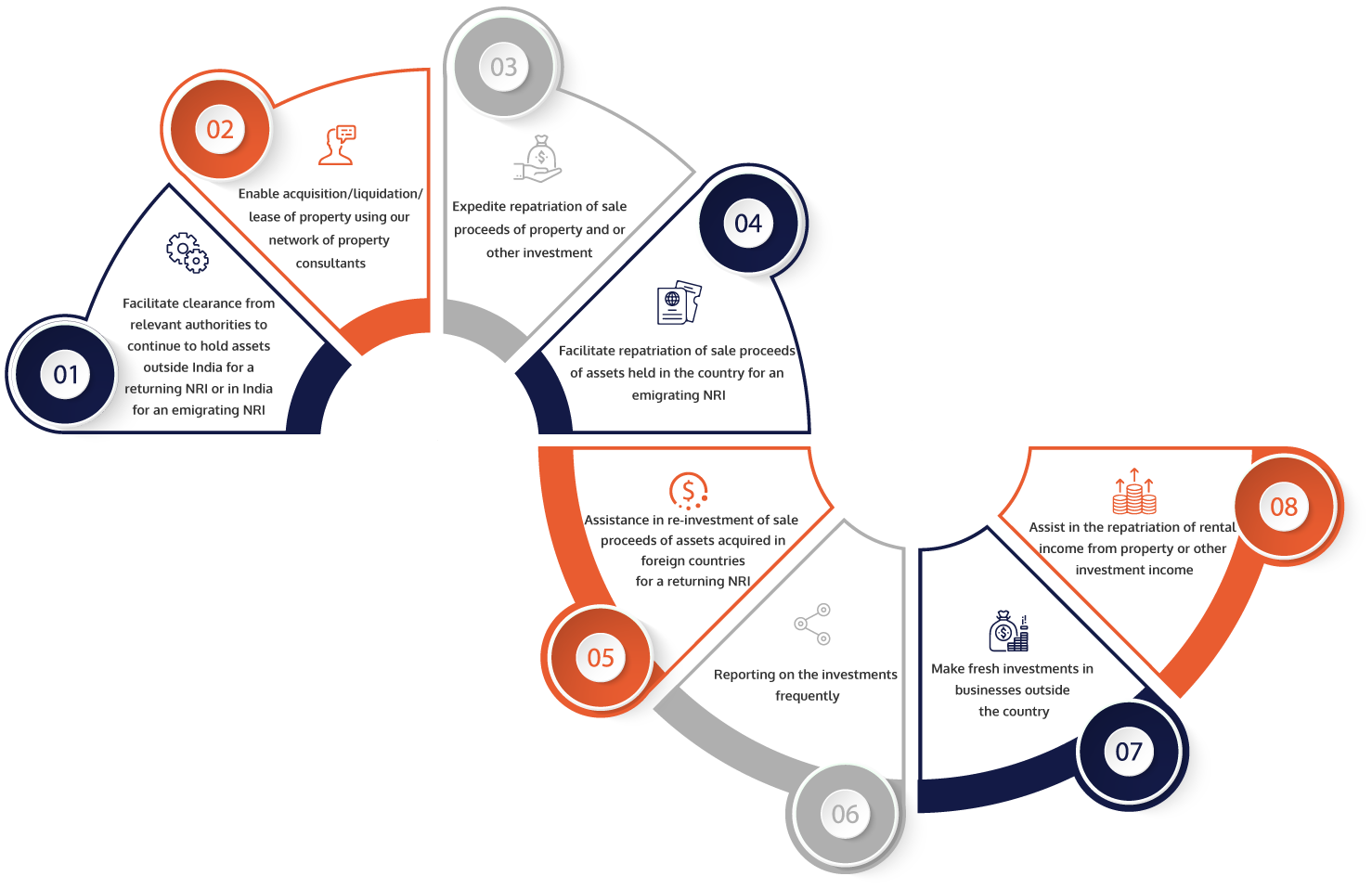

- NRI taxation is one of the issues to consider or be concerned about. It is critical to understand and be aware of the consequences that will arise once you return to India. All of the laws of the land, all of the compliances, and all of the problems that must be addressed.

- That is also important when someone is planning to return to India and has not filed NRI returns for years due to reasons such as lack of tax liability, lack of awareness, case requirements, or having been used to living in countries where there is no direct tax liability on income earned, such as the UAE or other Gulf countries. People are customary because of the income tax rules and because they are located in their comfort zone.

The points to be evaluated were briefly discussed on a daily basis:

1. Obtaining a PAN/TAN/DSC/DIN number

- Once contractors start or plan to start a new business, they start to hear these terms more frequently, like TAN, PAN, DIN, and DSC. While a businessman plans things and develops business approaches, the company also has legal obligations.

- These legalities are required at every stage of the business’s establishment and operation. As a result, it’s crucial to get to know them completely and get expert help with DIN/DSC/PAN/TAN.

What exactly is PAN?

- PAN (Permanent Accountant Number) is a unique identifier provided to all Indian taxpayers. Nonresidents with NRO/NRE accounts in India must update their PAN with the bank.

- Any financial transaction or remittance of funds abroad of India requires the use of a PAN number.

To apply for a PAN card online, you’ll need the following documents:

- A photo ID, ration card, passport, driver’s licence, or Aadhar card may be used as proof of identity.

- Address proof includes a copy of a recent electricity bill, landline telephone bill, water connection bill, and gas connection card, bank account statement, passport, spouse’s passport, voter ID card, Aadhar card, and a government-issued domicile certificate.

- Birth certificate issued by the Municipal Corporation as proof of date of birth.

What is TAN?

- When making a tax payment to the Central Government’s account, every tax deductor must quote the TAN (Tax Deduction and Collection Account Number). If non-residents sell their property in India, the buyer must file a TDS return in India for a withholding tax deduction. It is not possible to file this TDS return without first getting a TAN.

- The Tax Deduction and Collection Account Number begins with alphabets, then moves on to number digits before ending with another alphabet. There is no specific proof of identity necessary for registration. Form 49B must be completed and submitted online through the Income Tax Department’s system. NRI services can help you obtain a TAN in India quickly and securely.

What exactly is DSC?

- Most documents are now in electronic format, and DSCs (Digital Signature Certificates) aid in establishing the sender’s identity. It is necessary for income tax and MCA filings by Indian businesses.

- If you’re interested in understanding how to get a digital signature in India, NRI Services can help. We’ve made obtaining a DSC in India simple and convenient for everyone.

What exactly is DIN?

- Anyone who wants to be a director of a company needs to get a DIN (Director Identification Number). In order to obtain a DIN for a Director in India, you will need the help of professionals.

2. Tax incidence and residential status in India:

This year, we received numerous emails with questions about Indian residential status and taxation. That is because many people who have been in offshore projects could not return to India due to the suspension of flights because of the current pandemic situation, and while many NRIs working abroad have the possibility of work from home and so came back to India to stay with their families.

Their residential status for Indian tax purposes has changed this entire shuffle. In addition, there was an amendment to the Finance Act of 2020 that brought about a few changes in the provisions of residential status, which added to the confusion.

Let me attempt to clarify residence status so that you may appropriately calculate your tax incidence.

This article is divided into three sections:

- Resident Indian status, which is further separated into ROR (Resident and Ordinarily Resident) and ROR (Resident but Not Ordinarily Resident) (RNOR). If you do not meet the criterion of a resident Indian, you will be classified as a nonresident (NR). To proceed, determine your residency status.

- Tax incidence based on residence status- Once you’ve determined your residence status, you may see if your only Indian income is taxable or if your international income is also taxable in India.

- FAQs – A few frequently asked questions and answers from this financial year.

Please keep in mind that I am only discussing individuals in this article. It means that we are not discussing the residential status of a company, partnership firm, or other entity.

Residential Status Resident – According to the Income-tax Act of 1961, an individual is considered a Resident of India if he meets either of the following conditions:

(i) Stay in India for at least 182 days in the previous year; or

(ii) Stay in India for at least 60 days in the previous 4 year and at least 365 days in the four preceding years.

The following relaxation is provided:

- Let me try to clarify residence status so you can figure out your tax liability. I An Indian citizen or a Person of Indian Origin (PIO) who leaves India for work or who lives outside India and visits India during the preceding year shall only be considered a resident of India if he stays in India for 182 days or more, rather than the 60 days indicated in point (ii) mention above.

Nonresident-

- If a person does not meet any of the aforementioned fundamental requirements; he is classified as a nonresident.

- If a person is a resident, he must determine if he is a Resident and Ordinarily Resident (ROR) or a Resident but Not Ordinarily Resident (RNOR) (RNOR).

ROR – Resident and Ordinarily Resident

An individual is said to be ROR if he meets the following two conditions:

- he has lived in India for at least two of the ten previous years immediately preceding the relevant previous year; and

- he has spent 730 days or more in India in the seven years preceding the relevant previous year.

Resident but Not Normally Resident (RNOR)

If an individual is a resident but does not meet both of the additional conditions listed above, he will be RNOR.

An amendment to the Finance Act of 2020 added two additions/exceptions to the preceding rule:

If an individual meets either of the following two conditions, he will still be considered RNOR:

- If he meets all four of the following criteria:

(i) He is an Indian citizen or an individual of Indian ancestry.

(ii) During the preceding year, his total income, excluding income from overseas sources, exceeded Rs 15 lakhs.

(iii) He is not subject to taxation in any other nation or territory due to his domicile, residence, or any other comparable criterion.

- If he meets all four of the following criteria:

(i) He is an Indian citizen or a person of Indian ancestry. (ii) During the preceding year, his total income, excluding income from foreign sources, exceeded Rs 15 lakhs.

(iii) He arrives to India on a prior year’s visit

(iv) He stays in India for 120 days or more but not more than 182 days.

Tax incidence based on Residential status

| Type of Income | ROR | RNOR | NR |

| Indian Income | Taxable in India | Taxable in India | Taxable in India |

| Foreign income | Taxable in India | Only two types of Foreign income is taxable in India:

1. Business income from the business controlled wholly or partly from India 2. Professional income from the profession set up in India |

Not taxable in India |

Only those individuals who have two categories of foreign income, namely business revenue from a business controlled from India and professional revenue from a profession set up in India, will be affected by the amendments to the Finance Act, 2020 regarding presumed residency and RNOR.

3. 15ca/15cb Assistance with Non-Resident Payments or Repatriation of Own Funds

What is the difference between 15ca and 15cb?

A person making a payment to a non-resident must file a 15ca form and obtain a 15cb certificate from a Charted Accountant. These forms are filed online, and copies of these forms are submitted to the bank where money is transferred out of India.

What is the significance of 15ca?

- The person in charge of making payments to non-residents submits information to the Income Tax Department using the 15ca form. 15ca comprises information such as the remitter’s and remittee’s pan numbers, contact information, remittance amount, TDS information, Lower/NIL TDS certificate information (if any), and so forth.

- It is divided into four pieces, with only one of them requiring filling, depending on the case. It can be filed online by logging into the remitter’s income tax account.

What exactly is a 15cb certificate?

- A certificate granted by the Institute of Chartered Accountants of India (ICAI) is known as 15cb. A CA verifies that applicable TDS is deducted by the remitter when sending payment to the remitee in 15cb. 15cb is also filed online and includes the Chartered Accountant’s digital signature.

- If you’re unsure how to obtain a 15cb certificate, you can reach out to Nricaservices. We have a team of experts who can help you from beginning to end, making the repatriation procedure as painless as possible.

When it comes to repatriating funds from India, why and when do we need 15ca and 15cb?

- When non-residents want to repatriate funds from their savings or income in India, the bank requires them to complete form 15ca and obtain a 15cb certificate from a CA.

- In all cases of repatriation, regardless of the amount or purpose, the bank generally requests 15ca and 15cb. This is because they want to ensure that all taxes are paid before any money is sent out.

- Form 15ca is a self-declaration that there is no outstanding tax liability on the funds applied for outward remittance.

Do you plan to sell a property in India? How can we help you?

- If an NRI plans to sell a property in India, the income tax provisions that apply to him differ from those that apply to residents. For example, the NRI seller’s withholding tax rate is substantially higher than the resident seller’s. In addition, the buyer must obtain a TAN and file a separate TDS challan.

- We can help you step by step by advising you on the best way to proceed. If necessary, we can also help you obtain a lower/NIL TDS certificate. If you’re not sure how to file a 15ca, we can do it for you. In addition, we will issue 15cb to you in the shortest possible time.

4. Assistance in Responding to Tax Notices Online

What is a notice of income tax?

The Income-tax Department processes an Individual’s / Assesse’s (also known as a taxpayer’s) income-tax return when he or she files it. If there is any ambiguity, error, or miscalculation in the income-tax return filed, the Assesse is notified by receiving an income-tax notice.

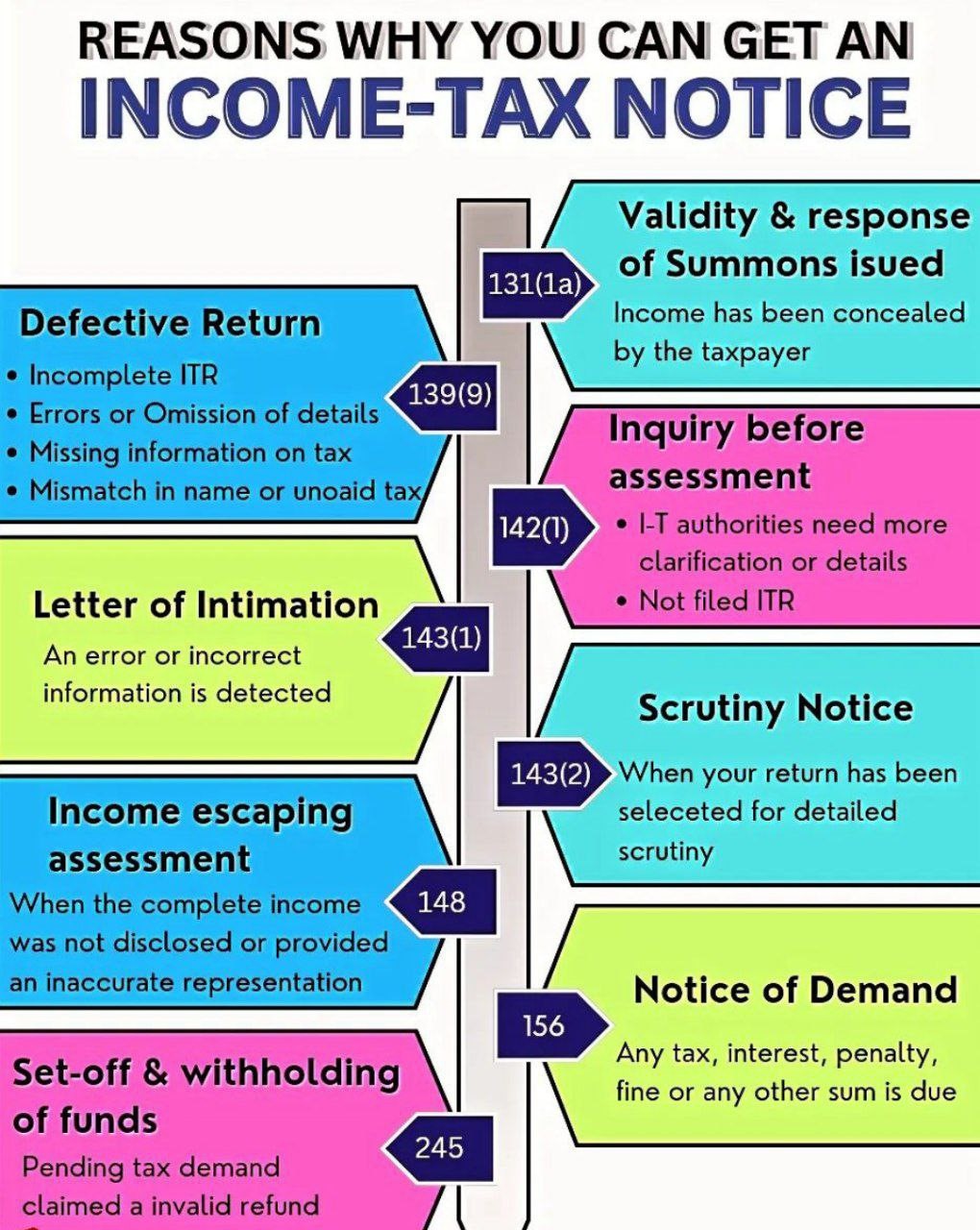

What types of tax notices does the Internal Revenue Service issue?

The Income Tax Department issues numerous forms of income tax notices under various sections such as section 139(9), 143(1), 143(2), 148, 156, and others. These notices can now be responded to online by uploading relevant documents along with an appropriate response.

What should I do about the Indian tax notice u/s 139(9)?

If the Assessing Officer believes that the return filed by the Assessee is defective, he may notify the Assessee by issuing an Income-tax notice under Section 139(9) of the Income-tax Act and allow him 15 days to correct the error. An income-tax notice under section 139(9) may be issued in the following circumstances:

- In cases where the Assessee is required to keep such details, the Balance Sheet and Profit & Loss Statement are not filed.

- An income tax return must be filed prior to the payment of self-assessment tax.

- Tax Deducted at Source (TDS) has been deducted and claimed as a refund, but no income details are provided in the return.

- Tax information (TDS Other) is provided, but no income information is returned. To fix the error, an income-tax return must be submitted within 15 days of receiving the Income-tax Notice. Otherwise, the return will be considered invalid.

How can we help you?

Are you uncertain how to respond to a notice from the Indian Income Tax Department? If so, we are here to assist you. We will request that you provide us your income tax notice so that we can better comprehend your situation. We will explain your situation to you and ask you to send us the necessary documentation so that we may respond to the notification via the income tax online portal. We will send you an acknowledgement of response for your records once the response has been filed. Our team also responds to questions about it, such as why I received a notice from the income tax department or how to set up an online income tax account.

Contact India Financial Consultancy Corporation to have your GST return filed online quickly and properly.

For query or help, contact: singh@caindelhiindia.com or call at +91 9555 555 480

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.