Frequently Asked Questions on form 16 & 16A

Table of Contents

Frequently Asked Questions on form 16 & 16A

Q.1: What is the procedure to get Form 16?

There is no specified procedure for it. The employer will directly issue the receptive Form 16 to the employee and even in case an employee leaves their job, the employer will then also provide the Form 16.

Q.2: How to file ITR in case we are not in receipt of Form 16?

As discussed earlier, it is an important document for filing the ITR and specially the section of Income from Salary. But in case, Form 16 is not available due to one or the other reason, such a person can still file their ITR.

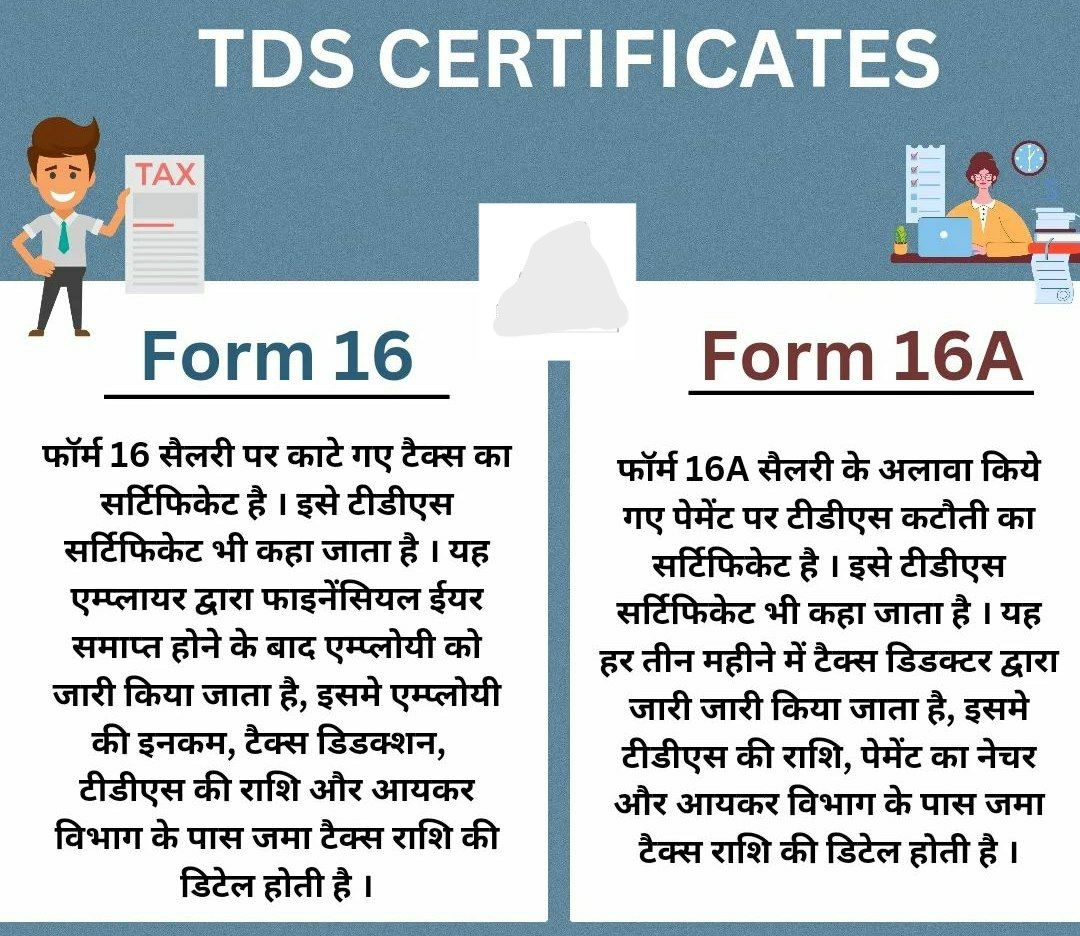

Q.3: Can there be a scenario, where the employer deducts TDS, but does not issue Form 16?

As provided in the rules and regulations, any employer paying salary to its employee, is under an obligation to deduct TDS on the same and deposit the amount deducted, with the Government of India, within the prescribed time period. Where such TDS is deducted, the employer is required to file the return of the same and provide a certificate of such TDS deducted to the respective employee. Thus, it is compulsory for every employer deduction TDS to provide a certificate in Form 16 to its employees.

Q.4: Does non issuance of Form 16 signify, no obligation to pay tax and file ITR?

As discussed above, even though a Form 16 be issued, where TDS is deducted on salary received, the responsibility of paying income tax and filing income tax return is upon the employee. Even when the employer fails to issue the Form 16, one must file an income tax return and pay off the taxes that are due. If the employer does not issue Form 16 within the stipulated time, the same is liable for penalty under Income tax Act. And the employee may raise a grievance to the Income tax department in this regard by contacting their local branch of Income office or through the Aaykar Sampark Kendra.

Q.5: What are the components of salary income?

Generally, the amount of salary includes basic salary, dearness allowance, wages, other allowances, bonus, leave encashment, gratuity, pension and any perquisite received by the employer from the employee, either without any payment or at a lower cost.

Q.6: What is the due date for issuance of Form 16 by the employer?

Every employer is required to issue Form 16 to their employees, on or before 15th June every year, immediately after the financial year in which TDS is deducted.

Q.7: Can the deductions not reflected in Form 16, be claimed while filing annual ITR?

Yes, even though there are deductions that are not mentioned in Form 16, by the employer, such deductions can be claimed at the time of filing the ITR, provided such deductions are within the allowed limit.

Q.8: Does pension received form part of salary and is subject to Form 16?

It is to be noted that pension received, arising due to earlier employment relation, be taxable as salary income. Where such pension is received through the banking channel, the employer is under an obligation to issue Form 16.

Q.9: Is there any liability to pay taxes in case of change of jobs and the taxable income exceeds the minimum income exempt from tax?

As discussed above, the employee shall pay the tax by performing self-assessment, even though TDS has been deducted or not by the employer. The main basis is that the income in that particular FY exceeds the minimum income exempt to tax.

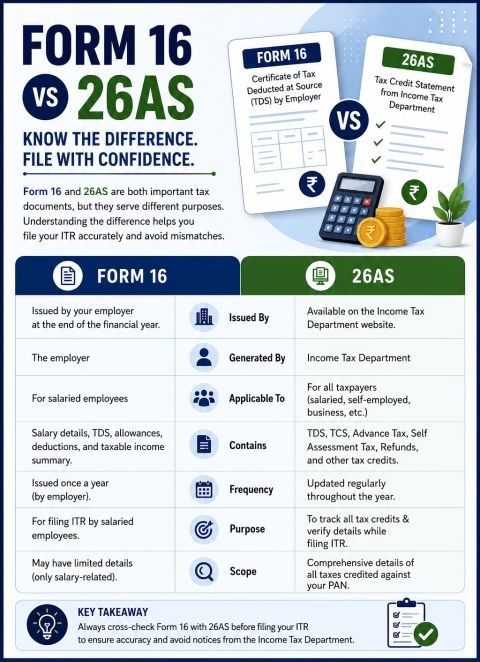

Q.10: What to do, where the original Form 16 is lost?

Where the employee loses the possession of original Form 16, due to any reason, may apply to their employer for issuance of a duplicate Form 16. Also, the employee can download Form 26AS, to get the details of TDS deducted and deposited, for the particular assessment year.

Q.11: What are the steps for uploading the Form 16 on the website?

The assessee is required to visit www.carajput.com.com. Two options will appear namely –

-

- Upload Form 16

- Start Your Return

- Select the option of Upload Form 16. The portal will ask for uploading of documents.

- The applicant to browse Form 16 from the given list of Forms.

- Upload the form and confirmation will be required. Click on “OK” to continue

- The applicant needs to create an account on the website, which will be required for further processing. Once the account is created, login with the login credentials.

- After logging in, the applicant needs to verify the personal details fetched using your Form 16.

- After that, enter the details pertaining to Date of birth, Father’s name, Mobile Number etc. and then click on the Submit button once details are entered.

- The software will automatically prefill the salary details, using the Form 16 uploaded.

- Also, the deductions, specified in Form 16 will be automatically provided in the ITR.

- The applicant needs to choose the residential status, determined on the basis of provisions prescribed in law.

- After completing the information, proceed with the filing of return.

- Update the latest details of all the Savings and Current Accounts in India.

- Click to view the final summary of the ITR.

- On the last step, the software will calculate the net tax liability/refund. In case of tax liability, the software will redirect to the payment gateway.

- Once the payment is successful, the return will be submitted and forwarded to the concerned authority. The applicant will also receive an e ITR-V Acknowledgement on their registered Email account

Q.12: What is the procedure after ITR filing?

After successful filing of return, the applicant needs to E-verify the return for further processing

Q.13: Is Filling Tax return without Form 16 is possible ?.

In the e-filing of income tax returns, Form 16 is a crucial document. You can still e-file your income tax return if you are a salaried taxpayer and do not have Form 16. Here’s a link to a similar guide.

Q.14: What should you do after you’ve e-filed your Tax return ?

After you have completed the e-filing of your income tax return, you must verify it so that the Income tax department can process it further. If for some reason, you cannot e- verify the income tax return then you required to send the signed copy of ITR acknowledgement V to CPC, Bengaluru.

Q.15: How Income tax filing via www.carajput.com?

Rajput Jain and Associates has created a question-and-answer-based return filing process in which you must answer a few easy questions and submit information about your income, tax-saving deductions, and other topics. As a result, the software will create your tax return. From Rajput Jain and Associates (www.carajput.com), you can learn how to file an income tax return.

Q.:16 Is family pension income taxable under the head as salary? Is Form 16 required?

Pensions paid to family members are taxable as Income from Other Sources. As a result, Form 16 is not necessary in this situation.

Q.17: Can an employer use Section 89 relief while calculating TDS on a salary?

Yes, the Company while deducting TDS, the employer can consider relief under Section 89 relief and issue Form 16 accordingly

Our comprehensive range of services includes:

1) GST Compliance and Advisory :

· Registration and Filling of GST Returns

· GST Audit and Assessment Supports

· GST Planning and Optimization

2) Income Tax Services :

· Income Tax Return Preparation and Filling

· Tax Planning and Advisory

· Income Tax Assessment Assistance

· Tax Audit

· TDS Return

3) Accounting Services :

· Bookkeeping Services

4) Accounting Audit :

· Financial Statement Audit

· Internal Audit

· Compliance Audit

Comprehensive study about TDS & TCS chapter

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.