FAQ on Payment for Good/Services Provided by MSEs U/s 43B(h)

Table of Contents

Frequently asked questions on Section 43B(h) of the Income Tax Act

Q: When will the amendment on on Payments for Goods or Services Provided by MSEs U/s 43B(h) of the Income Tax Act come into effect?

Ans. The amendment on on Payments for Goods or Services Provided by MSEs U/s 43B(h) has taken effect from April 1st, 2023 and is applicable for the financial year 2023-24 and onwards.

Q : The amount outstanding to an MSE Supplier as on March 31, 2024, is paid after the due date specified under the Ministry of Micro, Small and Medium Enterprises Act 2006, but just before the due date of furnishing the ITR u/s 139(1) of the Income Tax Act. Will such an amount be allowable as a deduction in the tax return of Financial Year 2023-24?

Ans. No, the first provision to section 43B of the Income Tax Act allows deduction of dues paid after the end of the financial year but before the due date of filing the income tax return. However, this benefit is not available for payments to Micro and Small Enterprises unless amount is paid within due dates specified in section 15 of the Ministry of Micro, Small and Medium Enterprises Act (15/45 days). so, amount will not be allowed as a deduction in the ITR of financial year 2023-24.

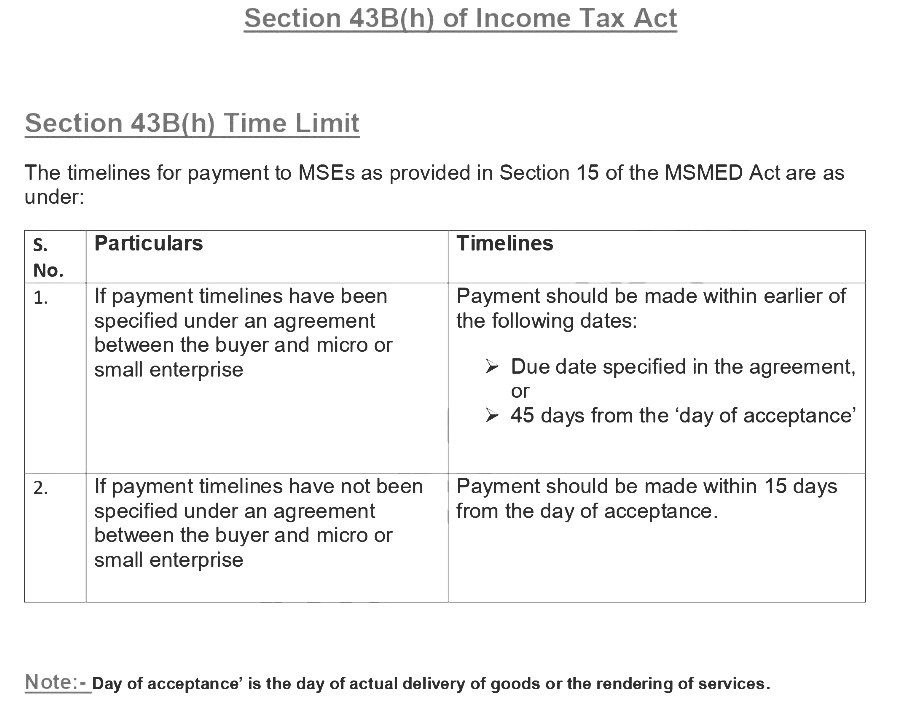

Q: What if there is no agreement between buyer & seller?

Ans. If there is no written agreement, the payment must be made within 15 days.

Q: What if interest is not paid within the time limit?

Ans. If payment is not made within the specified time limit, the taxpayer must pay compound interest with a monthly rate compounded to the supplier on the amount from:

-

- Appointed day, or

- the agreed-upon date, at three times the Bank Rate notified by the Reserve Bank of India

Q: Will any disallowance be attracted u/s 43B(h) if the payment is made beyond the time permitted under the MSMED Act but within the same financial year?

Ans. No, there will not be any disallowance since the payment is made within the same financial year and is not outstanding at the end of the year.

Q: Who can enjoy the benefits under the Ministry of Micro, Small and Medium Enterprises Act?

Ans. To avail the benefits under the Ministry of Micro, Small and Medium Enterprises Act, the supplier must be registered with a Udyam Registration No under the Ministry of Micro, Small and Medium Enterprises Act, 2006, as a MSE engaged in manufacturing or providing services.

Q: A taxpayer has purchased and received goods from an micro or small enterprise Supplier on March 1, 2024. After verification, a dispute is raised on March 5, 2024, stating that certain goods were defective. The dispute is resolved on March 30, 2024. What would be the due date for payment if there is no written agreement specifying the due date?

Ans. The due date for payment would be 15 days from the date of receipt of goods, i.e., March 15, 2024. However, since the dispute was raised within 15 days, the payment must be made within 15 days from the date the issue was resolved, i.e., by April 13, 2024.

Q. In the above scenario, suppose the dispute is raised on March 20, 2024, after 15 days from the date of acceptance of goods. How would the provision of 43B(h) be construed?

Ans. If the due date for payment was 15 days from the date of receipt of goods, i.e., March 15, 2024, and the payment was not made by then, the amount should be disallowed u/s 43B(h) if it is outstanding as on March 31, 2024. Since the dispute was raised after the expiry of 15 days, the benefit of extension is not available.

Q. Will the provisions of Section 43B(h) of the IT Act be attracted if the buyer opts for presumptive taxation under section 44AD/ADA of the of the Income Tax Act.?

Ans. The provision of section 44AD of the IT Act overrides sections 28 to 43C. Therefore, if buyer opts for presumptive taxation, payments to MSE will not attract disallowance on on Payments for Goods or Services Provided by MSEs U/s 43B(h) of the Income Tax Act.

Q. If the buyer retains an amount of retention money in accordance with the agreement with the MSE Supplier, will disallowance be attracted on Payments for Goods or Services Provided by MSEs U/s 43B(h) of the IT Act for not paying the retention amount within the time permitted under the MSMED Act?

Ans. The MSMED Act requires payment within the specified time limit. Therefore, even if the amount is retained as per the agreement, it must be paid within the specified time limits.

Q. Will disallowance be on the amount inclusive of Goods and Services Tax or only on the principal amount?

Ans. Section 43B(h) uses the term “any sum payable by assessee.” Hence, the entire amount, including Goods and Services Tax will be subject to disallowance u/s 43B(h).

Q. What if the expenditure is capitalized in the books of the taxpayer and there is a delay in payment to MSE vendors which remains outstanding at year-end?

Ans. Only expenditures claimed as deductions to compute the taxpayer’s income are subject to section 43B(h). Since capital expenditure is not claimed in computing income, section 43B(h) does not apply to such expenses.

Q. What would be the treatment of interest in case of delayed payment to the supplier?

Ans. In case of delayed payments, interest will be applicable as per the Ministry of Micro, Small and Medium Enterprises Act, which would be disallowed to the buyer while computing taxable income. This disallowance is irrespective of whether the corresponding principal amount is paid in the same financial year.

Q. Will the provisions of 43B(h) apply to traders registered under the Ministry of Micro, Small and Medium Enterprises Act 2006?

Ans. No, the Micro, Small and Medium Enterprises Act defines an ‘enterprise’ as an undertaking engaged in manufacturing or providing services. Traders are not covered by this definition and are therefore outside the scope of the Ministry of Micro, Small and Medium Enterprises Act.

Q. Will Ministry of Micro, Small and Medium Enterprises registered entities who are micro and small enterprises having opening balances be covered under section 43B(h)?

Ans. No, opening balances due to such entities will not be covered during Financial Year 2023-24.

Q. Is section 43B(h) only applicable to entities audited under the Income Tax Act?

Ans. Section 43B(h) is applicable to all entities irrespective of whether their books are audited.

Draft Comments for section 43B(h) for Tax Audit Report Form 3CA-3CD and Form 3CB-3CD

Reporting by Auditor for 43B(h) in 3CD

All 3 situations explained with Audit Process 👇

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.