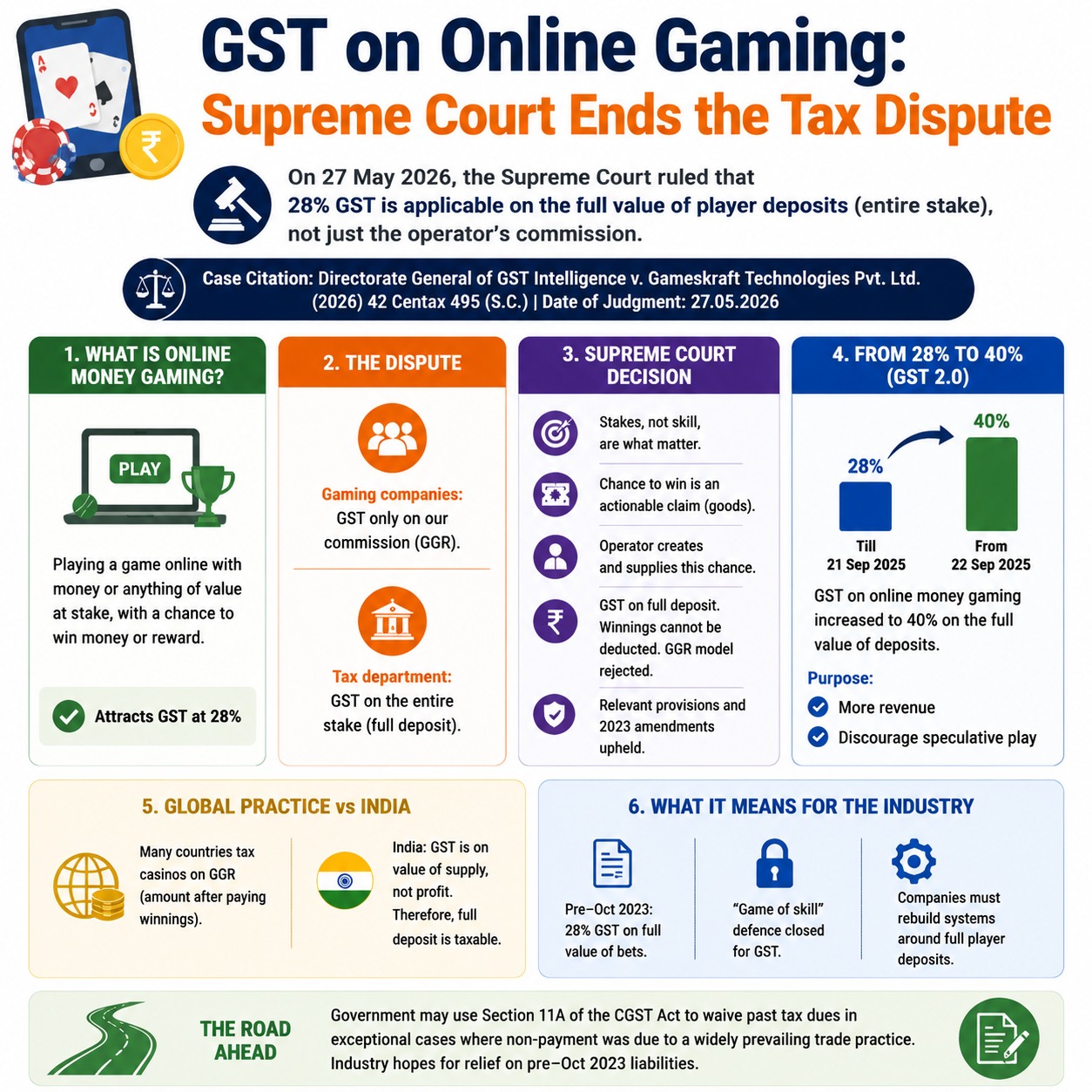

SC Stay ₹1.5 trillion of GST notice against online gaming Co

Table of Contents

Supreme Court: Stay INR 1.5 trillion worth of GST notices against Online Gaming Co.

The recent Supreme Court decision to stay INR 1.5 trillion worth of goods and services tax notices against online gaming companies has significant implications for both the gaming industry and tax authorities. Here’s a detailed breakdown of the developments

Key Details of the Supreme Court’s Order

- Stay on Tax Notices: The Supreme Court has stayed tax notices issued to gaming companies until a final decision is reached. The stay applies to notices potentially expiring soon, preserving their validity during ongoing litigation.

- Rationale for Stay: Prevents gaming companies from facing coercive recovery actions during the legal process. Protects the revenue department’s ability to collect tax by extending the timeframe for action on notices, which would otherwise lapse due to statutory limits.

- Hearing Scheduled: The matter is set for a detailed hearing on 18 March 2025.

Arguments from Both Sides

Gaming Companies:

- Actionable Claims: Argued that entry fees and prize pools should not be taxed as “actionable claims” since they are escrowed funds used for winnings, not revenue.

- Impact of Demands: highlighted that the tax demands far exceed net revenues over five years, potentially pushing the industry towards bankruptcy.

- Tax Applicability: Asserted that the 28% goods and services tax rate on “full face value” of bets should apply prospectively from October 2023, not retrospectively.

Revenue Department:

- Tax Clarifications: Claimed that the amendment made in August 2023 merely clarified the existing law, making the tax demand valid for prior periods.

- Preventing Lapses: Sought the stay to ensure time-sensitive notices do not become void during litigation.

Background and Legal Context

- Goods and services tax Amendments (August 2023): The Goods and Services tax Council imposed a 28% tax on the “full face value” of bets for online games, effective from October 2023. Previously, the tax was levied on platform fees, significantly lower than the total bet amounts.

- Transfer of Cases: The Supreme Court consolidated multiple cases across high courts, including the ₹21,000 crore notice against Gameskraft, ensuring uniform adjudication.

- Definition of Actionable Claims: The inclusion of actionable claims under goods and services tax laws for gaming has been a contentious point, as such claims were previously exempt for this sector.

Implications of the Stay of Supreme Court’s Order

- For Gaming Companies: Immediate relief from recovery actions, allowing continued operations during litigation. Potential for reduced financial distress and bankruptcy risks.

- For Revenue Authorities: Ensures that notices nearing expiration remain valid, preserving the possibility of tax recovery post-litigation.

- For the Gaming Industry: Brings attention to the need for clear regulatory frameworks, especially for skill-based games versus gambling. Highlights challenges posed by aggressive taxation in a nascent, high-growth industry.

- The stay order provides a balanced approach, addressing both the industry’s operational concerns and the revenue department’s legal challenges. Overzealous tax demands risk destabilizing a growing sector contributing to innovation, employment, and revenue generation.

Next Steps on GST for Online Gaming

- The Supreme Court will deliberate on retrospective applicability of the 28% goods and services tax rate. The inclusion of actionable claims under the goods and services tax for online gaming. The distinction between skill-based games and gambling for tax purposes.

- A final decision will have wide-reaching implications for taxation policies and the future of India’s online gaming sector.

This case underscores the importance of striking a balance between fair taxation and fostering a supportive environment for emerging industries.

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.