GTA opt either for 5% (without ITC) or 12% (with ITC): GSTN

Table of Contents

Option provided to GTA to opt either for 5% (without ITC) or 12% (with ITC) under Forward charge

- Previously, the Central Board of Excise and Customs vide Notification No. 13/2017- dated June 28, 2017 (“Services Reverse Charge Mechanism Notification”), to notify the kind of categories of services on which tax will be payable under the Reverse Charge Mechanism.

- The Union Finance & Corporate Affairs Minister, Smt. Nirmala Sitharaman, presided over the 47th meeting of the GST Council, which was held in Chandigarh on June 28–29, 2022. After GST Council meeting recommendations were made to give the Goods Transport Agency the option to pay GST at a rate of 5 percent on RCM or 12 percent under a forward charge option that would be used at the beginning of the financial Year.

- The Reverse charge mechanism option was left intact. Additionally, to withdraw the exemption on services of renting of House property for residential purpose to business entities; and to bring all the taxable service of GST Dept of Posts under forward charge mechanism.

As per the changes the GST Council recommendation has been notified vide below notification:

The Central Board of Excise and Customs Notification on Goods Transport Agency:

The Central Board of Excise and Customs vide Notification No. 05/2022- dated July 13, 2022 has issued amendments in Services RCM Notification, w.e.f. July 18, 2022, in a below:

- CBEC deleted words “who has not paid central tax at the rate of 6%,” in Serial No 1 of the Services Reverse Charge mechanism Notification so as to provide an option to GTA to pay GST @12% under Forward charge or @ 5% (without ITC)

- The Central Board of Excise and Customs deleted words add new GST proviso in Serial No 1 of the Services Reverse Charge mechanism Notification, has been inserted to provide that No 1 of the Services Reverse Charge mechanism notification (i.e., for GTA) will not apply where the supplier has taken GST registration & has exercised the option to pay tax under forward charge mechanism & the supplier has issued a GST Tax invoice to the recipient charging applicable GST Tax & has made a declaration on such invoice issued.

- CBEC deleted words “by way of speed post, express parcel post, life insurance, and agency services provided to a person other than Central Govt, State Govt or local authority or Union territory” in Serial No 5 of the Services Reverse Charge mechanism notification, so as to bring such services under the forward charge mechanism.

- The Central Board of Excise and Customs provide the new Serial No 5AA has been added in the Services Reverse Charge mechanism Notification r.t. service by way of renting of house property to a registered person.

New Declaration by GTA required to be submitted :

- CBEC also add new Annexure III in the Services Reverse Charge mechanism Notification w.r.t. declaration by the GTA, opting to pay tax on services in relation to transport of goods under forward charge mechanism for an whole FY.

- New Declaration by GTA required to be submitted as of July 5, 2022, per Notification No. 14/2022, As mentioned in the Notification Sl No. 4:

- on an invoice issued by a GST registered person whose aggregate turnover exceeds INR 20 Cr but who is exempt from submitting an online invoice, example of Declaration are mention below :

We hereby declare that though our aggregate turnover in any preceding financial year from 2017-2018 onwards is more than the Total turnover notified under rule 48(4), we are not required to prepare an invoice in terms of the provisions of the said sub-rule.

- Considering the Declaration above, GTAs whose Turnover in any preceding FY from 2017–18 onwards exceeds Rs 20 cr and Declaration is particularly not coming purview of the issue & generation of e-invoice required to mention the above declaration in his Tax Invoice.

IFCCL Comments:

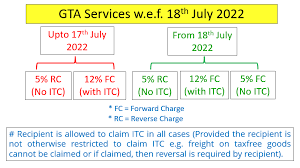

- Existing Goods Transport Agency who opt to pay GST @ 12% do not have the option to pay GST @ 5%. They have to pay GST at the rate of 12% on all their consignments under forward charge. GTA w.e.f. July 18, 2022 will be allowed to pay GST either at 5% (without ITC) or 12% (with ITC) on their consignments under forward charge.

- Moreover, Reverse Charge mechanism can be opted only if Goods Transport Agency has not opted to pay under forward charge and the option to continue under RCM @ 5% rate will also continue. Goods Transport Agencies will be able to switch from one option to the other at the beginning of the FY.

- As per above the conclusion that GST changes have been made in Notification No.11/2017- dated June 28, 2017 (“Services Rate Notification”) vide Notification No. 03/2022- dated July 13, 2022.

- Samer kind of Notifications have been made under IGST, 2017 and UTGST Act and implemented as Option provided to GTA to opt either for 12% (with ITC) under Forward charge or 5% (without ITC) via RCM.

Conclusion : GSTN allow Amendment under 47th GST Council Meeting for Goods Transport Agency to opt either for 5% (without ITC) or 12% (with ITC) under Forward charge.

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.