Misconceptions & Realities on Filing Income Tax Returns

Table of Contents

Common Misconceptions & Realities on Filing Income Tax Returns

A lot of people are concerned about the time of year when ITR Filling Due date is coming due. ITR filing process may appear difficult, confusing, or even intimidating. Moreover, there are Various ITR Return myths that may exacerbate these emotions. In this blog, we hope to separate reality from fiction by debunking some of the most popular tax fallacies and guiding you through the time-consuming process of properly completing your income tax. Understanding these misconceptions and their realities can help ensure compliance, avoid penalties, and make the most of the available tax benefits. Filing Income Tax Returns can be daunting, leading to various misconceptions. Here are some common misconceptions and the truths behind them:

Common Misconceptions and Realities on ITR filling

-

Only Salaried Individuals Need to File Income Tax Returns

Reality: Every individual with a total income exceeding the basic exemption limit, including self-employed, freelancers, and business owners, must file Income Tax Returns. Additionally, those with foreign income/assets, or who wish to claim tax refunds, must file Income Tax Returns regardless of income level.

-

No Tax Liability Means No Need to File Income Tax Returns

Reality: Filing Income Tax Returns is mandatory even if your tax liability is zero, particularly if your income exceeds the exemption limit or you meet other specific criteria (such as holding foreign assets). Filing also provides a record for loans and visa applications.

-

Filing Income Tax Returns is Required Only If Form 16 is Received

Reality: While Form 16 simplifies the process for salaried individuals, it is not the sole basis for filing Income Tax Returns. All sources of income must be considered, including rental, interest, and capital gains, irrespective of Form 16 issuance.

-

Interest Income from Savings Accounts is Tax-Free

Reality: Interest income from savings accounts is taxable. However, a deduction of up to Rs. 10,000 is available under Section 80TTA (for individuals below 60 years) and up to Rs. 50,000 under Section 80TTB (for senior citizens).

-

Filing Income Tax Returns is Voluntary for Pensioners

Reality: Pension income is taxable as salary, and pensioners must file Income Tax Returns if their income exceeds the basic exemption limit. Senior citizens (above 60) and super senior citizens (above 80) enjoy higher exemption limits, but filing remains mandatory above those thresholds.

-

Gifts are Always Tax-Free

Reality: While gifts from specified relatives are tax-free, gifts from non-relatives exceeding Rs. 50,000 in a financial year are taxable. Certain gifts, like those received on weddings, through inheritance, or as part of specified transactions, may be exempt.

-

Only One Form of Income Can Be Reported in Income Tax Returns

Reality: Multiple sources of income (salary, business income, rental income, interest, etc.) must be reported. The appropriate ITR form should be chosen based on the nature of all incomes.

-

Income Tax Returns Filing is Not Required If TDS is Deducted

Reality: Even if TDS is deducted, you must file Income Tax Returns if your total income exceeds the exemption limit. Filing Income Tax Returns also helps claim refunds for excess TDS deducted.

-

Losses Cannot Be Carried Forward Without Filing Income Tax Returns

Reality: To carry forward losses (like business losses, capital losses), Income Tax Returns must be filed before the due date. Unfiled returns result in the forfeiture of the right to carry forward such losses.

-

Filing Income Tax Returns is Difficult and Time-Consuming

Reality: With the advent of online filing and simplified processes, Income Tax Returns Filing has become more straightforward. Various resources and professional services are available to assist in accurate and timely filing.

Common Misconceptions About Income Tax Returns Filing for Futures & Options

Filing Income Tax Returns for Futures and Options trading can be complex, leading to various misconceptions. Key Points to Remember:

-

- Classification of Futures and Options trading Income: Non-speculative business income if traded through a recognized exchange.

- ITR Filing Requirement: Mandatory for all Futures and Options Traders, irrespective of profit or loss. Ensures losses can be carried forward for up to eight years and set off against future gains.

- Tax Audit Applicability: Required if turnover exceeds Rs. 10 crores or under specific conditions related to presumptive taxation.

- Turnover Calculation: Includes the absolute values of profits and losses, option premiums, and differences from reverse trades

By understanding these key aspects and addressing common misconceptions, Futures and Options Traders can ensure compliance with tax laws and optimize their tax filings. Accurate ITR filing helps avoid penalties and leverages potential tax benefits effectively. Few mention here under:

-

Futures and Options trading Income/Trades are Speculative

Reality: According to Section 43(5) of the Income Tax Act, 1961, transactions in F&O, if conducted through a recognized stock exchange, are classified as “Non-Speculative” business income. The nature and intention behind the transactions, along with factors like frequency, help determine if they are business transactions.

-

Income Tax Returns Filing is Only Required for Profits

Reality: Income Tax Returns must be filed regardless of whether there are profits or losses. Filing an Income Tax Returns even in the case of losses has advantages:

-

- Carry Forward Losses: Allows the taxpayer to carry forward the losses to future years, reducing taxable income in those years.

- Avoid Penalties: Income Tax Returns Filing on time helps avoid penalties of up to Rs. 10,00,000 for non-compliance.

-

Tax Audit is Mandatory for Net Loss in Futures and Options trading

Reality: A tax audit is required only if certain conditions are met:

-

- Turnover Threshold: If the turnover exceeds INR 10 Cr, a tax audit is mandatory due to the high percentage of digital transactions.

- Presumptive Taxation: If the income tax taxpayer has opted for presumptive taxation U/s 44AD in any of the last five years and wants to declare income below the presumptive rate, a tax audit is required.

-

Turnover in Futures and Options refers to Total Transaction Value

Reality: Turnover for Futures and Options trading is calculated by adding the following:

-

- Profit/Loss: Sum of the absolute values of profits and losses from F&O trades.

- Option Premiums: Premiums received on selling options.

- Reverse Trades: Differences from reverse trades..

FINAL THOUGHTS

In conclusion, submitting tax returns is easier than most people believe. Income Tax Taxpayers can simply finish their returns without encountering unnecessary complications by utilising the appropriate tools, such as e-filing software and tax consultants. It’s time to clear up these income tax misunderstandings and focus on understanding the importance of filing an ITR.

FAQS (FREQUENTLY ASKED QUESTIONS) ON ITR

Can I claim HRA while filing income tax?

- Rent receipts are valid documentation of rental payment to the employer for the purpose of claiming HRA. After verifying, the employer may offer deductions and allowances. Rent receipts serve as the basis for determining the HRA allowance.

Where can I file my income taxes in Delhi/NCR, India?

- Taxpayers can easily file their income tax return (ITR) for the AY 2023-24 with the assistance of a skilled tax adviser in Delhi/NCR.

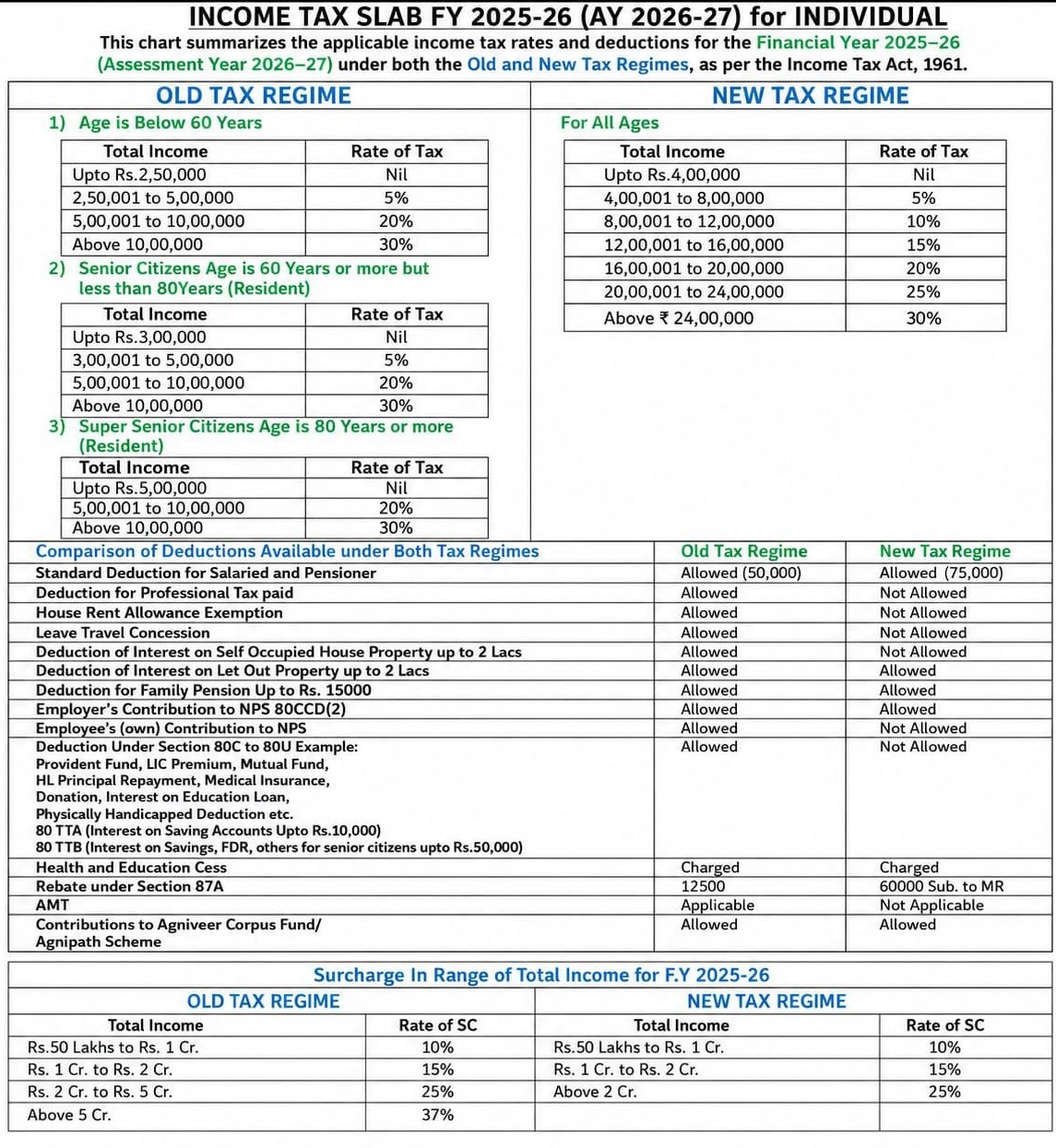

𝐈𝐧𝐜𝐨𝐦𝐞 𝐓𝐚𝐱 𝐒𝐥𝐚𝐛 𝐟𝐨𝐫 𝐅𝐘 𝟐𝟎𝟐𝟓-𝟐𝟔 (𝐀𝐘 𝟐𝟎𝟐𝟔-𝟐𝟕) 𝐟𝐨𝐫 𝐈𝐧𝐝𝐢𝐯𝐢𝐝𝐮𝐚𝐥

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.