New Income Tax Return Forms for AY 2023-24

Table of Contents

New ITR Return Forms for AY 2023-24

It also published the Income Tax Rules, which aim to make additional changes to the Income Tax Rules, 1962.

Moreover, in Appendix-II of the principal rules, for Forms SAHAJ ITR-1, ITR-2, ITR-3, SUGAM ITR-4, ITR-5, ITR-6, ITR-7, and ITR-V, the two Forms shall be substituted.

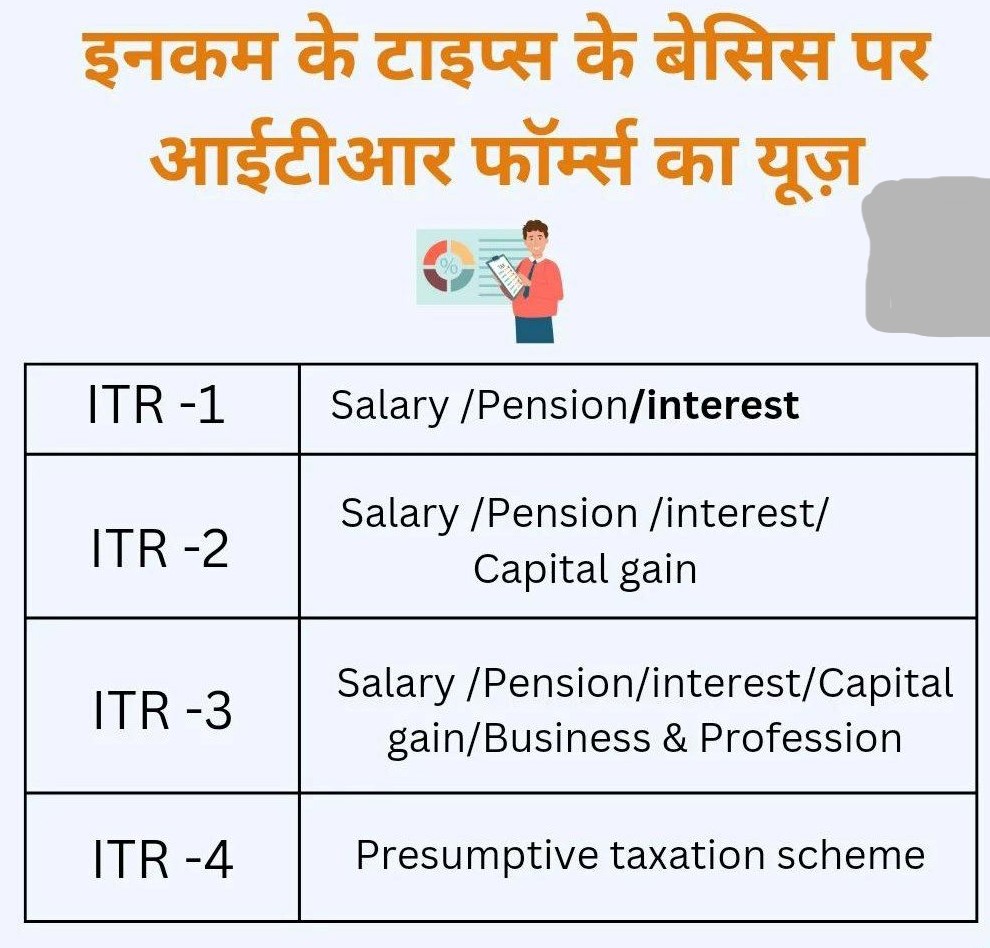

Form ITR-1 Sahaj is for people who are resident (not ordinarily resident) and have a total income of up to Rs 50 lakh from salary, owning a house property, having other sources of income (including interest, etc.), and having agricultural income up to Rs.5 thousand. It does not apply to anyone who is a director of a company, has made an investment in unlisted equity shares, or has had TDS deducted under Section 194N or has deferred income tax on an ESOP.

The Form is a Combination of 5 Parts

· Part-A: General Information,

· Part-B: Gross total income,

· Part-C: Deductions and taxable total income,

· Part-D: Computation of Tax Payable, and

· Part-E: Some other Information.

In light of the ongoing COVID pandemic and in order to make things easier for taxpayers, no significant changes have been made to the ITR Forms in comparison to last year’s ITR Forms. As a result of amendments to the Income-tax Act of 1961, only the most basic changes were made. There has been no change in the manner in which ITR Forms are filed in comparison to last year. For income earned in financial year 2022-23, the assessment year is 2023-24.

The ITR must be filed for income earned between April 1, 2022 and March 31, 2023, in the assessment year 2023-2024, with the last date being July 31, unless extended by the government. The fiscal year is followed by the assessment year (AY) (FY). This is the period during which the income earned during the fiscal year is assessed and taxed. The fiscal year (FY) and fiscal year (AY) both begin on April 1 and end on March 31.

FAQ on New ITR Return Forms for AY 2023-24:

Who can file ITR 1 Sahaj?

Individuals who are residents and have a total income of up to Rs 50 lakh from salaries, one house property in single ownership, interest income, family pension income, and agricultural income of up to Rs 5,000 are eligible for the ITR 1-Sahaj.

Who can file ITR Form 4 (Sugam)?

Individuals, HUFs, and Firms (other than LLP) who are residents and have a total income of up to Rs.50 lakh, one house property (single ownership), income from business and profession computed under sections 44AD, 44ADA, or 44AE, or Interest Income, Family Pension, and agricultural income of up to Rs.5,000 are eligible for ITR 4-Sugam.

Who can file ITR-2?

Individuals and HUFs who do not have business or professional income and are thus ineligible to file Sahaj can file ITR-2. Anyone who is a director of a company, as well as anyone who owns unlisted equity shares in a company, must file ITR-2 returns. Individuals who own more than one house should file an ITR-2 income tax return. Individual taxpayers who earn money from a business or profession cannot use ITR-2.

Who can file ITR-3?

Those who earn a living from a business or profession can file Form 3 of the ITR. 3. Individuals who earn money from the following sources may file ITR 3:

- Owning a business or working in a profession (both tax audit and non-audit cases)

- Household income, salary/pension, capital gains, and other sources of income may all be included in the return.

Who can file ITR-5?

Firms, LLPs, AOPs and BOIs (Body of Individuals), Artificial Juridical Person (AJP), Estate of Deceased, Estate of Insolvent, Business Trust, and Investment Fund are all eligible to apply this income tax return. Individuals, HUFs, and companies (e.g., partnership firms, LLPs) are not the only ones who can file ITR Form 5.

Who can file ITR-6?

Companies can use ITR Form 6 to file their tax returns. Companies that do not qualify for an exemption under Section 11 must file ITR-6 income tax returns. Section 11 exempts companies that earn income from property held for charitable or religious purposes. This income tax return must be submitted electronically with a digital signature to the Income Tax Department.

Who can file ITR-7?

Trusts, political parties, charitable institutions, and other organisations that have exempt income under the Act can file Form ITR-7. Individuals and companies who fall under Section 139(4A), Section 139(4B), Section 139(4C), or Section 139(4D) must file an ITR-7 form. Taxpayers should match the taxes deducted, collected, or paid by or on their behalf with their Tax Credit Statement Form 26AS.

The ITR-7 form is divided into two sections, each with 23 schedules. Part A is made up of general information. Beginning with the 2019-20 fiscal year, a taxpayer also need to provide information on registration or approval details. Part B outlines total income and tax computations for taxable income.

THIS IS RIGHT TIME TO FILE ITR RETURN FOR AY 2023-24

- ITR filing time limit varies according to the type of taxpayer (individual, HUF, firm, LLP, company, trust, and AOP/BOI) and the auditability.

- The time limit for filing an income tax return is usually the 31st of July of the assessment year (AY). The ITR must be filed for income earned between 1 April 2022 and 31 March 2023 but no later than 31 July 2023, unless the government extends the time limit.

- In my opinion, the best time to file an income tax return for the FY 2022-23 is not before June 15th, 2023.

- The following points have been aimed to be explained in this blog:

(a) what are the/documents details mandated for filing Income Tax Return.

(b) The source from which the information in the pre-filled ITR Form / Form 26AS / Form 16 / Form 16A is acquired.

(c) Explain why the fiscal year’s return should not be filed before June 15, 2023.

- The prescribed ITR Forms & procedure for filing an Income Tax Return vary depending on the amount of income earned per year and the source of income, such as salary, business profit, investment profit, and so on. Before preparing and submitting an income tax return, certain documents are required.

- Based on what the deductor uploads, Form 26AS picks up the TDS details on the taxpayer’s income.

6.1 A deductor is a person or entity that deducts tax from a payment at the point of origin. The tax deducted by the deductor through a TDS system must be submitted with the Income Tax Department within a certain time frame.

6.2 The TDS deductor must additionally file a statement detailing the tax deducted. TDS return forms are Forms 24Q, 26Q, 27Q, and 27EQ, which must be submitted to the Income Tax Department by the deductor.

- FORM 26AS: The most critical document to have before submitting an ITR is Form 26AS. This form, also known as the annual consolidated statement, covers all of the taxpayer’s tax-related information, such as details of tax deducted at source, advance tax, and so on.

7.1. The Annual Information Return (AIR), which is filed by various entities based on what an individual has invested or spent, primarily high-value transactions, is also reflected in Form 26AS.

7.2 All of this must be submitted by May 31, 2023. This means that pre-filled returns and Form 26AS will not be updated on the tax department’s website until mid-June, and taxpayers may be unable to complete a tax return with correct information.

- Annexure-II contains salary information, such as the total breakdown of the wage and the deductions that the employee is entitled to. Annexure I must be filed for each of the four quarters of a financial year, but Annexure II must only be filed for the fourth quarter of each financial year.

- TDS Form 26Q: This form is used to calculate TDS on all payments other than salary. It is applicable for TDS u/s 193 and 194 of the Income Tax Act of 1961 and must be reported by the deductor every quarter. TDS on income such as dividend securities, interest on securities, directors’ salaries, professional fees, and so on are filed on Form 26Q.

- TDS Form 26Q: This form is used to calculate TDS on all payments other than salary. It is applicable for TDS u/s 193 and 194 of the Income Tax Act of 1961 and must be reported by the deductor every quarter. TDS on income such as dividend securities, interest on securities, directors’ salaries, professional fees, and so on are filed on Form 26Q.

TDS Form 27Q is applicable to payments made to non-resident Indians and foreigners other than salary. It is used to declare TDS for non-resident Indians and foreigners. Every quarter, the deductor submits Form 27Q, which is used to calculate TDS under Section 200(3) of the Income Tax Act of 1961. TDS on additional income, such as interest, bonuses, or any other amounts owed to NRIs or foreigners, is calculated using Form 26Q.

After filing the TDS returns, the deductor will issue Form 16/16A.

- PRE-FILLED ITR FORM: To make compliance easier for taxpayers, ITR Forms are now pre-filled with information such as salary income, tax deducted at source, tax payments, and so on.

- In her Budget speech for the Finance Bill , the Finance Minister declared that beginning in FY 2022-23, the details of capital gains from listed securities, dividend income, and interest from banks, post offices, and other sources will be pre-filled in ITR Forms.

- The data is already filled in. Form 26AS is also available in the taxpayer’s account on www.incometaxindiaefiling.gov.in.

- Deadline for filing TDS returns for the 4th QTR of FY 2022-23 is May 31, 2023, and the Timeline for TCS reports is May 15, 2023.

- Since a result, it is recommended that taxpayers submit their Income Tax Return after June 15, 2023, as the Pre-filled IT Return /Form 26AS / Form 16 will reflect updated details of taxable income and tax deducted at that time.

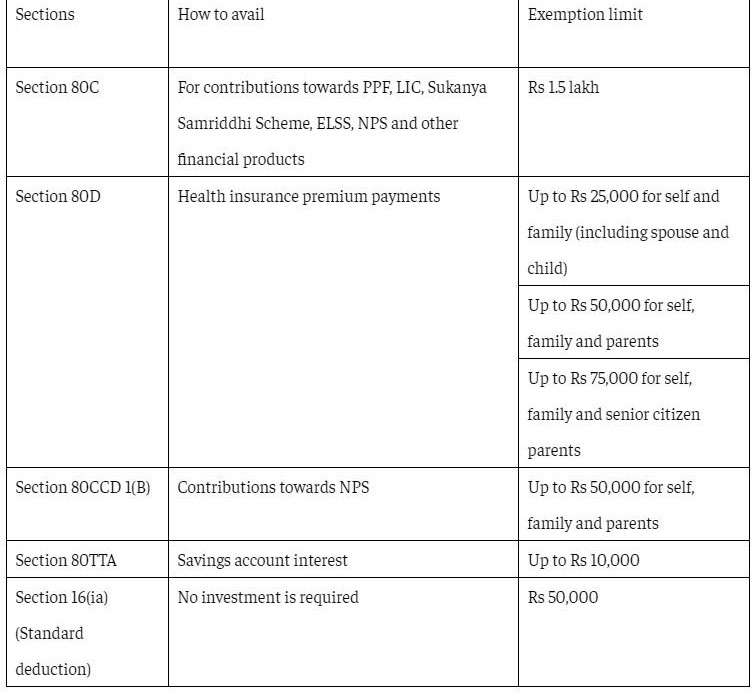

Income Tax Exemption

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.