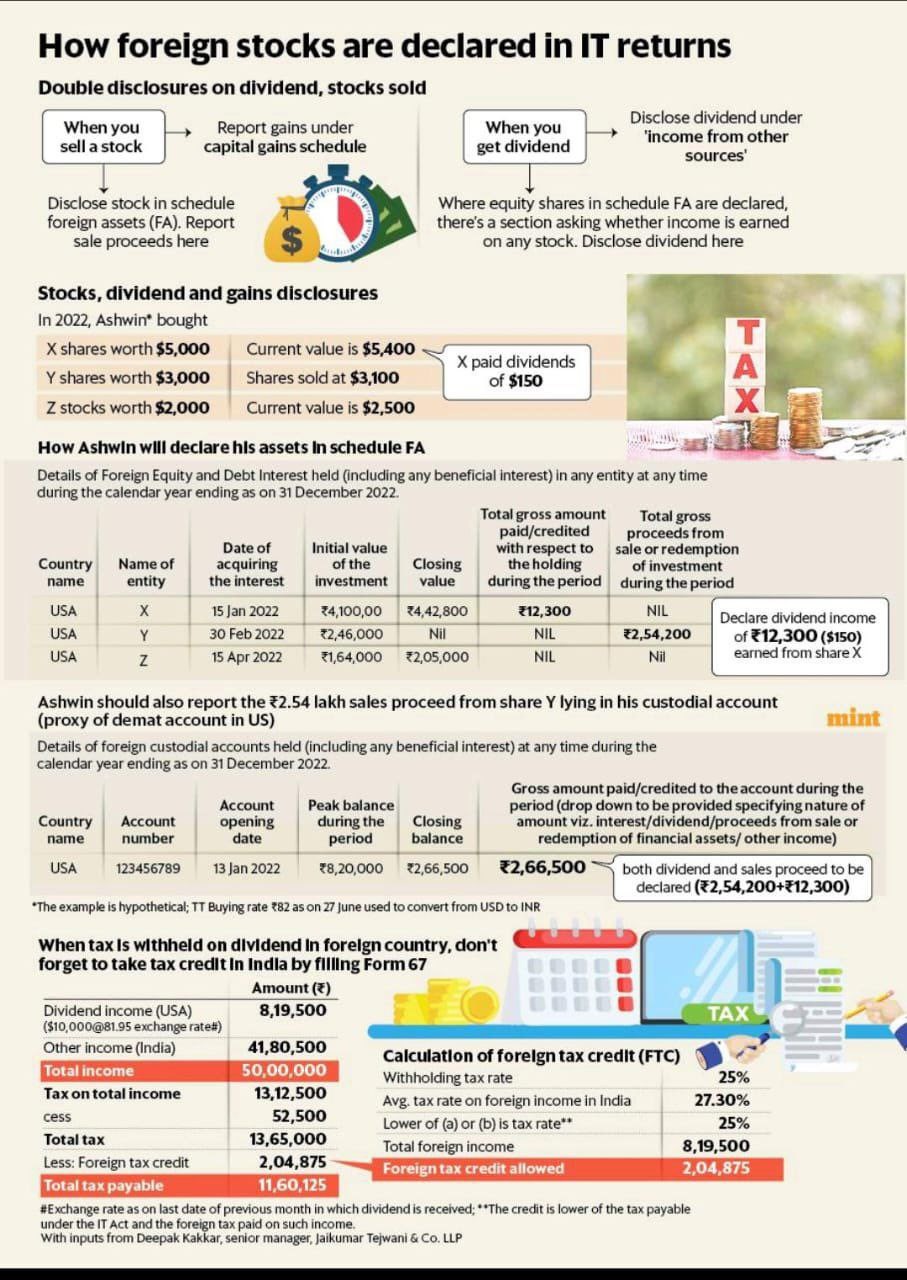

Overview on Taxation of Gains from Equity Shares

Table of Contents

Taxation of Gains from Equity Shares

- Short-Term Capital Gains (STCG) : Gains from selling equity shares listed on a stock exchange within 12 months of purchase. Tax Rate on STCG is @ 15%

- Long-Term Capital Gains : Long-Term Investor is holding shares for over a year before selling. Capital Gains. LTCG taxed at 10% on gains exceeding ₹1 lakh. Gains from selling equity shares listed on a stock exchange after 12 months of purchase. Tax Rate is 10% on gains exceeding ₹1 lakh (post 1 April 2018, without indexation benefit) Long term capital Gains up to 31 January 2018 are exempt.

- Loss from Equity Shares – Short-Term Capital Loss : Can be set off against STCG or LTCG from any capital asset. Up to 8 years, adjustable against any capital gains.

- Long-Term Capital Loss (LTCL) : Can only be set off against LTCG. Up to 8 years, adjustable against LTCG.

Summary Table of Taxation of Gains from Equity Shares

| Type of Gain/Loss | Definition | Tax Rate | Set-off | Carry Forward |

| STCG | Sale within 12 months | 15% | Against STCG or LTCG | 8 years |

| LTCG | Sale after 12 months (post 1 April 2018) | 10% (above ₹1 lakh, no indexation) | Against LTCG | 8 years |

| STCL | Loss within 12 months | Not applicable | Against STCG or LTCG | 8 years |

| LTCL | Loss after 12 months (post 1 April 2018) | Not applicable | Against LTCG | 8 years |

Securities Transaction Tax:

Securities Transaction Tax applicable & Levied on all equity shares transactions on a stock exchange. Registration charges, brokerage, and other charges are deductible from the sale value to calculate net gain or loss.

Securities Transaction Tax Collections see a major surge in the first three months of FY 2024-25, April 1-July 11 STT Collections rise nearly 130% YoY Source – CNBC TV18

CBDT Guidelines Report their share trading activities

1. Classification Criteria

The classification of gains or losses from the sale of shares as ‘business income’ or ‘capital gains’ depends on several factors:

- Volume and Frequency of Transactions: High frequency and volume, particularly in intraday trading or futures and options, may indicate business income.

- Intent: If the intent is to profit from short-term price movements, it is typically treated as business income.

- Holding Period: Longer holding periods often suggest capital gains, while shorter periods suggest business income.

2. Calculation Methods

o Income from Business: All expenses incurred in earning the business income can be deducted. Profits are added to the total income for the financial year and taxed at applicable slab rates. ITR-3 is required, showing income from share trading under ‘income from business & profession’.

o Income from Capital Gains: Expenses incurred on the transfer can be deducted. Short-Term Capital Gains (STCG) are taxed at 15%. & Long-Term Capital Gains (LTCG) over ₹1 lakh are taxed at 10%. ITR Form Depending on other income sources, typically ITR-2 is required.

Summary position mention here under :

| Criteria | · | Business Income | Capital Gains |

| Volume/Frequency | · | High (e.g., day trading, F&O trading) | Low to moderate |

| Intent | · | Short-term profit | Long-term investment |

| ·Expenses Deduction | · | All business-related expenses | Transfer-related expenses only |

| Tax Rate | · | Normal slab rates | 15% (STCG), 10% on gains > ₹1 lakh (LTCG) |

| ITR Form | · | ITR-3 | Typically ITR-2 |

| CBDT Circular (Listed Shares) | · | Option to choose, consistent in subsequent years | Option to choose, consistent in subsequent years |

| Unlisted Shares | · | Not applicable | Always treated as capital gains |

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.