Presumptive taxation scheme: Cash deposits in bank A/c

Table of Contents

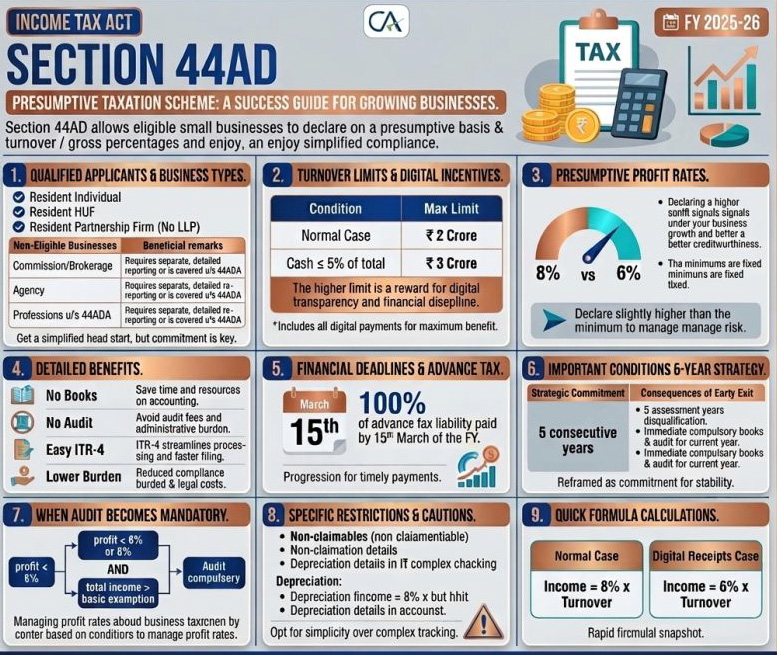

Income Disclosed under Presumptive Taxation Scheme (Sections 44AD, 44ADA, or 44AE): Cash deposits in bank A/c

Cash deposits in bank A/c in cases where income is declared under presumptive taxation scheme (Sections 44AD, 44ADA, or 44AE):

Section 68 of the Income Tax Act can only be invoked when There is a credit entry in the books of accounts maintained by the assessee. The assessee fails to offer a satisfactory explanation for the nature and source of such credit.

However, under presumptive taxation Sections 44AD, 44ADA, or 44AE : The assessee is not required to maintain books of account as per Section 44AA if they declare income at the prescribed presumptive rates. Hence, in the absence of books of accounts, the primary condition to invoke section 68 fails.

- No books = No Section 68: If the assessee is eligible and has opted for presumptive taxation (e.g., under Section 44AD), and has not maintained books, Section 68 cannot be invoked for cash deposits.

- Cash deposits ≠ unexplained income : if they can reasonably be attributed to business receipts (sales, collections, etc.). The total turnover is accepted, and the profit is offered at presumptive rates.

Judicial Support in the Treatment of Cases of Cash Deposits in Bank Accounts under the Presumptive Taxation Scheme:

- Courts and tribunals have consistently ruled in favour of assessees in such cases: COMMISSIONER OF INCOME TAX Surinder Pal Anand (2010) – P&H HC: Held that once income is offered u/s 44AD and no books are maintained, no addition u/s 68 is possible.

- Nand Lal Popli v. Dy. COMMISSIONER OF INCOME TAX (2016) – Income Tax Appellate Tribunal Chandigarh: Confirmed that individual deposits in bank accounts need not be explained if income is returned under the presumptive scheme.

- Thomas Eapen v. income tax officer (2020) – India’s Income Tax Appellate Tribunal Cochin: Reaffirmed that cash deposits that are reasonably attributable to business cannot be added u/ 68.

When Caution Is Needed: If cash deposits are disproportionately large or appear not commensurate with declared turnover, the Assessing Officer may Treat some part as undisclosed turnover, not unexplained cash credit u/s 68. Initiate inquiry u/s 69/69A (unexplained investments or money), but even this has limitations if presumptive tax provisions apply.

If books of accounts are voluntarily maintained and entries appear suspicious, then Section 68 may apply.

Assessee declares income u/s 44AD; cash deposit disclosure must clearly have no nexus with gross receipts of business.

CIT v. Surinder Pal Anand [2011] 242 CTR 061 (P&H HC)—this judgment firmly establishes that once an assessee declares income under Section 44AD, they cannot be expected to explain each and every cash deposit individually, unless those deposits clearly have no nexus with the gross receipts of the business. Two Key Points to Differentiate:

- Punjab & Haryana High Court in Surinder Pal Anand: Binding precedent within its jurisdiction (and persuasive in other jurisdictions unless overruled). Held that presumptive taxation (Sec 44AD) overrides the requirement to maintain detailed books or explain every deposit. Unless deposits are clearly unrelated to business (e.g., personal gifts, loans, or investments), Section 68 additions aren’t valid.

- Pune Income Tax Appellate Tribunal View—Disclosure still expected: The Pune Income Tax Appellate Tribunal in some cases (e.g., ITO v. Raghunath T. Jadhav) has held Even under presumptive taxation, if the assessee voluntarily discloses details of cash, bank balances, stock, and receivables, then he cannot escape scrutiny on inconsistencies or large unexplained balances. This does not contradict the law, but rather applies when:

- The assessee maintains books or submits detailed financial statements.

- AO questions consistency, plausibility, or nexus with declared turnover.

Reconciling the Two Positions:

| Legal Position | Surinder Pal Anand (P&H HC) | Pune ITAT |

|---|---|---|

| Applicability of Section 68 | Not applicable without books | May apply if books/details are voluntarily submitted |

| Requirement to explain deposits | Not required under Sec 44AD unless clearly unlinked | Required if voluntarily providing details shows inconsistencies |

| Presumption under Section 44AD | Strong protection to assessee | Assessee’s own disclosure can weaken protection if unexplained |

Practical Implication:

If an assessee files ITR u/s 44AD and does not maintain books, then Section 68 cannot be invoked unless there’s evidence that cash deposits are not linked to business. But if the assessee submits additional details like a balance sheet or cash flow (even voluntarily), and inconsistencies arise, the Assessing Officer may question the same—not strictly u/s 68, but possibly u/s 69/69A (unexplained money/investments), Or by treating such receipts as unaccounted turnover and taxing presumptive profit on the enhanced turnover.

In Summary:

-

Surinder Pal Anand protects assessees under pure presumptive taxation without books.

-

Pune Income Tax Appellate Tribunal rulings caution that once the assessee opens the door by furnishing additional disclosures, they are liable to explain anomalies. Therefore, the strategic choice lies with the assessee — either rely entirely on presumptive taxation and avoid disclosures or be prepared to explain figures if voluntarily furnished.

-

In cases where an assessee opts for presumptive taxation u/s 44AD, 44ADA, or 44AE and does not maintain books of accounts, cash deposits in the bank—if reasonably attributable to business turnover—cannot be taxed u/s 68.

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.