Overview on Setting up a Fintech Company in India

Table of Contents

Overview on Setting up a Fintech Company in India

- The Fintech Company In India : Fintech businesses operating in India are subject to various laws and regulations that govern their operations. Under the Companies Act 2013, fintech businesses are required to register and comply with all applicable laws and regulations like any other business in the country.

- FinTech is a mixture of two words finance and technology. FinTech companies are those that provide financial solutions using technology such as the internet, mobile phones, cloud services, or software technologies.

- The combination of finance and technology has emerged as one of the largest business sectors in the financial industry. FinTech is used by MNC, small-scale business industries, & individual customers to improve the management of their financial tasks. Previously, technology was used in Financial Services for back-end services such as organising day-to-day transactions and handling the company’s daily affairs. However, it has evolved and is now an important part of the financial sector.

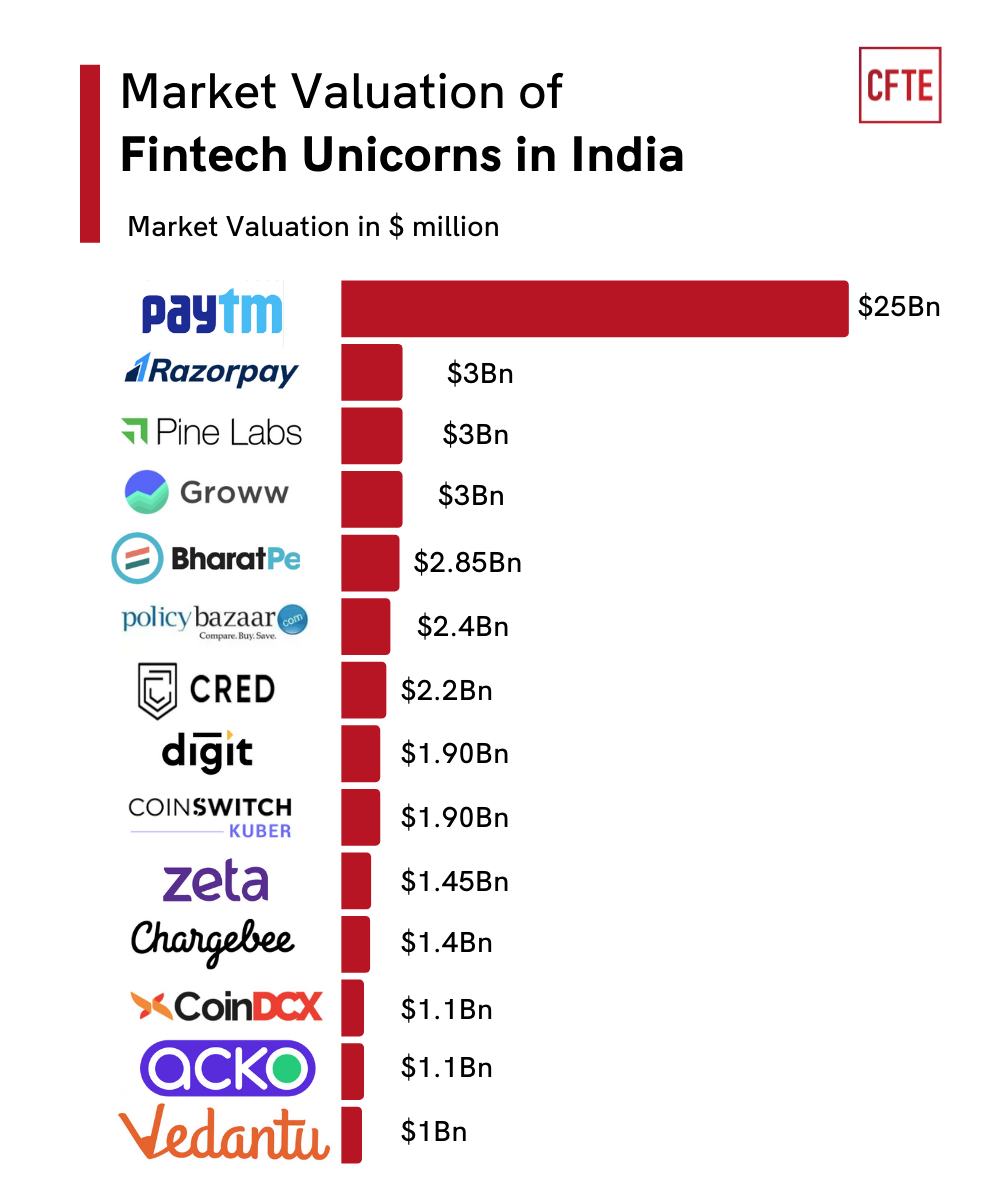

- There are numerous fintech companies in India, each offering a wide range of financial technology services. Here are a few example of fintech companies-Paytm; PhonePe; Razorpay; Policybazaar; Zerodha; Lendingkart; MobiKwik; BharatPe, These are just a few examples, and the fintech landscape in India is continually evolving with new startups and innovations emerging regularly.

What is Fintech framework?

- Financial technology (better known as fintech) is used to describe new technology that seeks to improve and automate the delivery and use of financial services. At its core, fintech is utilized to help companies, business owners, and consumers better manage their financial operations, processes, and lives.

- A fintech integration framework is a set of protocols and standards that can help you connect your fintech solution with other systems and platforms, such as banks, payment providers, and cloud services.

- Fintech businesses operating in India are subject to various laws and regulations that govern their operations, just like any other business entity in the country. The Companies Act 2013 is one of the key legislations that regulate the establishment and functioning of companies in India, including fintech companies.

- Under the Companies Act 2013, fintech businesses are required to register themselves as a specific type of company, such as a private limited company, public limited company, or LLP, depending on their structure and requirements. The registration process involves fulfilling certain legal formalities and requirements set forth by the MCA.

- In addition to the Companies Act 2013, fintech companies in India are also subject to various other laws and regulations, including but not limited to:

- Fintech companies dealing with payment services, lending, or other financial activities are regulated by the RBI. They need to obtain necessary licenses and approvals from the RBI and comply with its guidelines and regulations related to capital requirements, customer protection, cybersecurity, etc.

- Fintech companies involved in activities related to securities trading, investment advisory, crowdfunding, etc., may fall under the purview of SEBI Regulations. They need to comply with Securities and Exchange Board of India (SEBI) guidelines, obtain necessary registrations, and adhere to disclosure and compliance requirements.

- The Fintech companies providing taxable services are required to register under the Goods and Services Tax (GST) Act & comply with GST regulations for invoicing, tax collection, and filing of returns.

- Fintech companies dealing with electronic transactions, data protection, and cybersecurity are subject to the Information Technology (IT) Act & related regulations. They need to ensure compliance with data privacy and security standards, such as the Personal Data Protection Bill (PDPB), once enacted.

- Fintech companies engaged in cross-border transactions or foreign investment may need to comply with FEMA regulations governing foreign exchange transactions, capital flows, and repatriation of funds.

- Compliance with above Law like RBI, FEMA, Co Act, GST law, Income tax Laws, and regulations is essential for fintech businesses to operate legally and sustainably in India while maintaining trust and confidence among customers and stakeholders. Additionally, regulatory compliance helps mitigate risks and ensures the stability and integrity of the financial system.

Setting Up A Fintech Company Operations In India

As a fintech business, devising a business plan is the first step in setting up a fintech company in India, however, one has to consider numerable factors before taking that step. Before moving forward with the strategy, Indeed, devising a comprehensive business plan is crucial for setting up a fintech company in India. Before moving forward with the strategy, it’s essential to consider several factors, as you’ve listed. It sounds like you’re highlighting the potential benefits and challenges of starting a fintech company and suggesting seeking professional assistance to navigate the complexities of the process.it is necessary to consider the indicative list of factors as mentioned below:

- Identify your fintech business sector: Determine the specific sector within fintech in which you intend to operate. This could include payment processing, lending, wealth management, insurance, blockchain, or any other niche area.

- Familiarize yourself with the regulations: Understand the regulatory landscape governing fintech operations in India. This includes compliance requirements set forth by regulatory bodies such as the RBI, SEBI, and others.

- Discover your competitive edge: Conduct a thorough market analysis to identify your unique value proposition and competitive benefit. Determine what sets your fintech offering apart from existing players in the market.

- Recruit your dream team: Build a talented and diverse team with expertise in technology, finance, compliance, marketing, and other relevant areas. Your team is instrumental in executing your business plan effectively.

- Select the tech stack: Choose the appropriate technology stack and infrastructure to support your fintech platform. Consider factors such as scalability, security, interoperability, and regulatory compliance when selecting your tech stack.

- Prioritize data protection: cybersecurity & Data protection are paramount in fintech operations. Implement robust security measures to safeguard sensitive customer information and comply with data protection regulations.

- Obtain funding: Secure adequate funding to support your fintech venture. Explore various sources of funding, including venture capital, angel investors, bank loans, government grants, and crowdfunding platforms.

- Develop and enhance: Continuously invest in the development and enhancement of your fintech platform. Stay abreast of technological advancements and market trends to ensure that your offering remains competitive and relevant.

By carefully considering these factors and incorporating them into your business plan, you can lay a strong foundation for your fintech company in India and increase the likelihood of success in the dynamic and rapidly evolving fintech landscape.

Steps To Set Up a Fintech Company In India

- Select the Appropriate Business Structure-

-

-

- One Person Company

- A Limited Liability Partnership (LLP)

- Private Limited Company

- Register for GST

-

- Obtain legal contracts and agreements

-

-

- Co-Founders Agreement

- License Agreement for Intellectual Property

- Privacy Policy

- Website User Policy

- Terms and conditions for mobile app users

- Vendor Agreement

- Product Development Agreement

- Employment Agreements

- Obtain Intellectual property

-

- Licensing

-

-

- For Payment service

- For P2P

- For Retail service providers

- For Financial Management/Investment

-

6. Register domain name

Services offered by FinTech Company

Fintech companies have expanded their domain at both the micro and macro levels. Currently, such businesses provide a variety of services, such as personalising specialised digital platforms and online accounting software. So, let’s discuss the services that one can obtain from a FinTech company:

- Peer-to-Peer Lending

- Retail investment service

- Crowdfunding services

- E-commerce payment services

- InsureTech

- Regulatory Technology

What is the IFSC fintech incentive scheme?

Empower Indian Fintechs aiming for international markets: The objective of the scheme is to give money to Indian Fintech firms who want to enter international markets. The initiative promotes these businesses to grow internationally and positions India as a centre for Fintech innovation by providing grants and incentives.

Circular related to Framework for FinTech Entity Registration under IFSCA

IFSCA Circular dated April 27, 2022 on “Framework for FinTech Entity in the International Financial Services Centres Authority” empowers International Financial Services Centres Authority to grant Authorization or Limited Use Authorization to all eligible domestic and foreign Techfin/ FinTech entities, as a “Fintech Entity” under the said framework.

IFCCL Expertise In Fintech Company Setup

We have some of the top lawyers in the business on our fintech team. They have offered legal advisories on a wide range of legal issues that have an impact on the day-to-day operations of a typical fintech business. They have also assisted payment gateways and aggregators, drafted commercial agreements, and provided regulatory advice on the evolving regulatory framework (including advice on electronic transactions & payment services & related compliance requirements).

Role Of IFCCL In Setting Up A Fintech Company In India

- Our team of professionals provides a range of legal services in the Fintech industry, from incorporating a start-up in India to guaranteeing data protection, adhering to regulatory requirements, and handling agreements in an all-encompassing way.

- To provide the most comprehensive advice on fintech start-up business plans, strategic transactions, regulatory compliance, and litigation matters, we bring together experts from our venture capital, technology, banking and financial, securities litigation and white-collar defence, private investment funds, intellectual property, tax, and labour and employment practises.

- The Financial Regulatory and Markets Practices at our firm is Professional experts who are the best at what they do & can’t wait to tackle any challenge that comes their way.

Conclusion

- In summary, while starting a fintech company holds immense potential, it’s essential for entrepreneurs to seek guidance from knowledgeable legal experts to navigate the complexities of the process effectively. With the right support and expertise, entrepreneurs can increase their chances of success in the dynamic and competitive fintech industry.

- Fintech company concentrates on using cutting-edge technology for financial services, which makes them quicker and more effective. It will be a good decision to start your Fintech company since the industry seems to have a bright future.

- Starting a new FinTech company is a difficult process for new entrepreneurs. Hence, consult a reputable and experienced legal expert of Online Legal India if you want to start a top-notch online financial platform. Our knowledgeable professionals will guide you and make the FinTech company registration procedure easier for you.

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.