Taxation on Sale of Property under Income Tax Bill, 2025

Table of Contents

Taxation on Sale of Property under Income Tax Bill, 2025

The New Income Tax Bill, 2025, introduced in the Lok Sabha on February 13, 2025, aims to simplify and modernize India’s tax laws. While the bill largely aligns with the existing provisions of the Income-tax Act, 1961, it introduces certain changes concerning the taxation of property sales and the treatment of losses from house property.

Budget 2025 Updates: the income tax rebate u/s 87A has been increased to INR 60,000, making an income up to INR 12,00,000/- tax-free under the new tax regime. However, this increased rebate is not applicable to special grade incomes such as ‘Capital Gains’.

Capital Gain Taxation on Sale of Property in india

Overview of capital gains taxation on the sale of immovable property, incorporating the recent changes effective from July 23, 2024.

Short-term vs. Long-term Capital Gains

- STCG: If the property is sold within 24 months, taxed at applicable slab rates.

- LTCG: If held for more than 24 months, taxed at 12.5% (without indexation) or 20% (with indexation, if acquired before July 23, 2024).

Short-Term vs. Long-Term Capital Gains on Property

| Particulars | Short Term Capital Gains on Property | Long-Term Capital Gains on Property |

| Definition | Sold within 24 months | Sold after 24 months |

| Tax Rate | Slab rate | |

| (i) 20% with indexation (If sold before 23rd July 2024) | ||

| (ii) 12.5% without indexation (If sold on or after 23rd July 2024) | ||

| Indexation Benefit | Not available | Available (optional) |

| Tax Applicability | Added to total income and taxed as per slab rates | Taxed at fixed rates |

New Tax Regime for LTCG (Post-July 23, 2024)

- For properties bought on or after July 23, 2024: Only 12.5% tax without indexation is applicable.

- For properties bought before July 23, 2024: Taxpayer can choose between 12.5% (without indexation) or 20% (with indexation).

Computation of Capital Gains

- Long-Term Capital Gains before July 23, 2024: Indexed cost of acquisition & improvement can be deducted.

- Long-Term Capital Gains after July 23, 2024: Indexation benefit is removed if opting for the 12.5% tax rate.

- Under the Income Tax Bill 2025, for property acquired before July 23, 2024, Long-Term Capital Gains tax will be calculated as the lower of:

-

- 5% (without indexation)

- 20% (with indexation using CII adjustment)

For property acquired on or after July 23, 2024, Long-Term Capital Gains will be taxed at 12.5% without indexation. This change provides more flexibility to property sellers, allowing them to choose between indexed and non-indexed tax rates for properties bought before the cutoff date.

For properties acquired on or after July 23, 2024, the bill proposes a uniform Long-Term Capital Gains tax rate of 12.5% without the benefit of indexation. We have to be aware that the Income Tax Bill, 2025, is currently a proposal and has not yet become law. Its provisions are subject to change during the legislative process. These provisions are designed to provide relief to taxpayers with property-related losses, allowing them to offset such losses against other income and carry forward unadjusted losses for future set-off.

Tax Exemptions on Capital Gains from Property Sales

Exemptions on Short-Term Capital Gains

- Old Regime:

- Income below Rs. 2,50,000 (for individuals below 60 years) is exempt.

- Income below Rs. 3,00,000 (for individuals aged 60-80 years) is exempt.

- New Regime:

- Exemption applies if total income is below Rs. 4,00,000.

Exemptions on Long-Term Capital Gains.

Long-Term Capital Gains tax exemptions are available u/s 54, 54F, 54EC, and 54GB.

Tax Exemption Under Section 54

- To qualify for this exemption: Asset must be classified as a long-term capital asset. The asset sold must be a residential house. A new residential house must be purchased within 1 year before or 2 years after the sale (or constructed within 3 years). The new property must be located in India. The exemption is capped at 10 crore (effective April 1, 2023). The exemption applies to two residential properties (limited to Rs. 2 crore and only once in a lifetime).

Tax Exemption Under Section 54F

- For exemption under Section 54F: The taxpayer must reinvest the entire sale proceeds in another residential property. Purchase or construction of a new house must be within the prescribed period. The taxpayer must not own more than one residential house at the time of sale. Maximum deduction is 10 crore (effective April 1, 2024).

- Tax Exemption Under Section 54EC: Long-term capital gains can be reinvested in specified bonds (NHAI/RECL/PFC/IRFC) within 6 months. If not invested, gains will be taxed as short-term capital gains.

- Tax Exemption Under Section 54B: Applies to agricultural land outside rural areas. If reinvestment is delayed, funds must be deposited in a Capital Gains Account Scheme within Two years.

Summary of Capital Gains Tax Exemptions

| Section | Eligible Taxpayers | Sold Asset | Investment Made In | Time of Purchase |

| 54 | Individual/HUF | Residential House | New Residential House (India) | Within 1 year before/2 years after (3 years for construction) |

| 54EC | Any Taxpayer | Land/Building (LTCG) | NHAI/RECL/PFC/IRFC Bonds | Within 6 months |

| 54F | Individual/HUF | Any LTCG Asset (except residential property) | New Residential House | Within 1 year before/2 years after (3 years for construction) |

| 54GB | Individual/HUF | Residential Property | Equity Shares (50%+ ownership in a company) | Before ITR due date |

Capital Gains Account Scheme:

The Capital Gains Account Scheme of 1988 allows taxpayers to deposit their capital gains proceeds in authorized banks to defer tax liability. If the deposited amount is not utilized within Two years (for purchase) or three years (for construction), it will be taxed as capital gains in the financial year the time limit expires.

Carry Forward of Losses from House Property:

here is details of Set Off & Carry Forward of Losses & its treatment of losses from house property under the new bill is as follows:

- LTCG losses: Can be set off only against Long-Term Capital Gains and carried forward for 8 years.

- No more indefinite loss carry-forward through mergers—losses must expire within 8 years of their original computation year. Companies engaging in mergers for tax benefits will need to reassess their strategies post-April 2025.

- STCG losses: Can be set off against both Long-Term Capital Gains & short-Term Capital Gains and carried forward for 8 years. Losses can be carried forward only if ITR is filed before the due date.

- Set-Off Against Other Income: A loss from house property can be set off against income from other heads (e.g., salary, business income) up to a maximum of two lakh in a tax year.

- Carry Forward of Unabsorbed Losses: Any unabsorbed loss exceeding Two lakh can be carried forward for up to eight subsequent tax years. These carried-forward losses can only be set off against income from house property in the future years.

Example: How the Amendment Works

-

Before the Amendment: Company X had a business loss in FY 2015-16 (AY 2016-17). The loss was eligible for carry forward until AY 2025-26. Company X merged with Company Y in 2023. Company Y could restart the 8-year loss period, allowing the loss to be carried forward until AY 2031-32.

-

After the Amendment (Applicable from April 1, 2025): The loss from AY 2016-17 will expire in AY 2025-26, even if Company X merges with Company Y. The merger does not extend the carry-forward period beyond 8 years from the original computation year.

It’s important to note that the ability to carry forward these losses is contingent upon filing the income tax return within the prescribed due date. Failing to do so may result in the forfeiture of this benefit.

Impact of Budget 2025 on Section 87A Applicability on Capital Gains

-

Under the Old Tax Regime

- No Change in Scope of Rebate – The rebate under Section 87A remains unchanged for taxpayers opting for the old tax regime in FY 2025-26 (AY 2026-27). Old Regime Still Beneficial in Certain Cases –

- Taxpayers whose income consists solely of capital gains taxed at special rates can still claim rebate under Section 87A if their taxable income does not exceed the prescribed limit.

- Taxpayers with a mix of slab rate income and capital gains taxed at special rates can also assess whether the old regime remains beneficial based on their specific income composition.

- No Change in Scope of Rebate – The rebate under Section 87A remains unchanged for taxpayers opting for the old tax regime in FY 2025-26 (AY 2026-27). Old Regime Still Beneficial in Certain Cases –

-

Under the New Tax Regime

-

- Budget 2025 Amendment: The rebate under Section 87A is now limited only to tax computed as per slab rates under Section 115BAC(1A). This change applies from FY 2025-26 (AY 2026-27)

- FY 2024-25 (AY 2025-26): No Change in Scope – Until March 31, 2025, the rebate under the new tax regime applies to all income types, except LTCG from equity.

- FY 2025-26 (AY 2026-27): Major Restriction on Rebate The rebate is only applicable on income taxed as per slab rates. No rebate is available for capital gains taxed at special rates.

- Key Impacts on Capital Gains from FY 2025-26 Onward:

| Type of Income | Rebate Applicability (New Regime from FY 2025-26) |

| LTCG from Equity (Section 112A) | ❌ Not Eligible |

| STCG from Equity (Section 111A) | ❌ Not Eligible |

| LTCG from Debt Funds (Slab-based tax rate) | ✅ Eligible |

| LTCG from Debt Funds (Special tax rate) | ❌ Not Eligible |

| STCG from Debt Funds (Taxed at slab rates) | ✅ Eligible |

Old Tax tax regime remains attractive for certain taxpayers who can still claim a rebate u/s 87A despite having capital gains taxed at special rates. New Tax Regime is now more restrictive, as rebate under Section 87A will not be available on special rate capital gains from FY 2025-26. Taxpayers should evaluate whether the old regime or new regime is more beneficial based on their income mix and eligibility for deductions/exemptions.

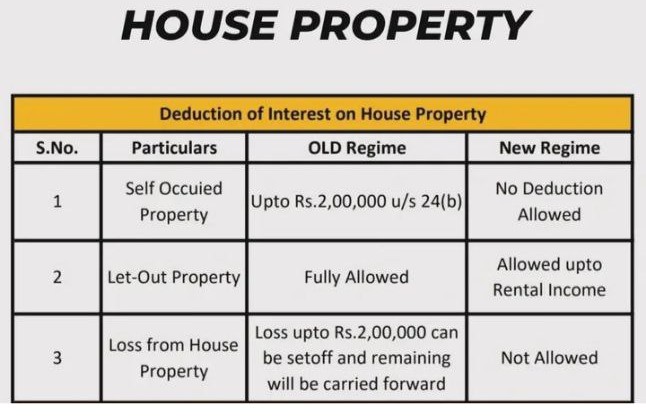

Comparison of deduction of interest on house property between the Old Regime and the New Tax Regime under Indian Income Tax Law.

Deduction of Interest on House Property

| S.No. | Particulars | Old Regime | New Regime |

|---|---|---|---|

| 1 | Self-Occupied Property | Deduction up to ₹2,00,000 under Section 24(b) | No deduction allowed |

| 2 | Let-Out Property | Interest deduction fully allowed | Allowed only up to rental income |

| 3 | Loss from House Property | Loss up to ₹2,00,000 can be set off; excess carried forward for 8 years | Set-off not allowed |

Key Implications of deduction of interest on house property between the Old Regime and the New Tax Regime

-

The Old Regime allows significant tax benefits on home loans, especially for self-occupied properties.

-

The New Regime removes most exemptions/deductions to offer lower tax rates but disallows home loan interest deductions.

-

For rental properties, under the New Regime, the interest is deductible only to the extent of rental income, avoiding any notional or actual loss benefit.

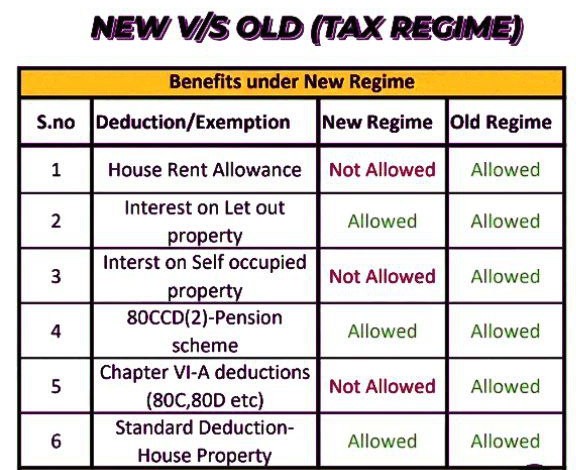

Comparison of deductions/exemptions available under the New Tax Regime vs. the Old Tax Regime.

New Regime vs. Old Regime – Tax Benefits Comparison

| S.No. | Deduction / Exemption | New Regime | Old Regime |

|---|---|---|---|

| 1 | House Rent Allowance (HRA) | ❌ Not Allowed | ✅ Allowed |

| 2 | Interest on Let-Out Property | ✅ Allowed | ✅ Allowed |

| 3 | Interest on Self-Occupied Property | ❌ Not Allowed | ✅ Allowed |

| 4 | 80CCD(2) – Pension Scheme Contribution | ✅ Allowed | ✅ Allowed |

| 5 | Chapter VI-A Deductions (80C, 80D, etc.) | ❌ Not Allowed | ✅ Allowed |

| 6 | Standard Deduction – House Property | ✅ Allowed | ✅ Allowed |

Other Point Takeaways:

-

Old Regime is suitable for those who have significant investments, loans, or eligible deductions.

-

New Regime is better for those with fewer exemptions/deductions, offering simplified lower tax rates.

-

Some deductions like 80CCD(2) (employer’s contribution to NPS) are allowed under both regimes.

-

Major exclusions in New Regime: HRA, 80C, 80D, home loan interest (self-occupied).

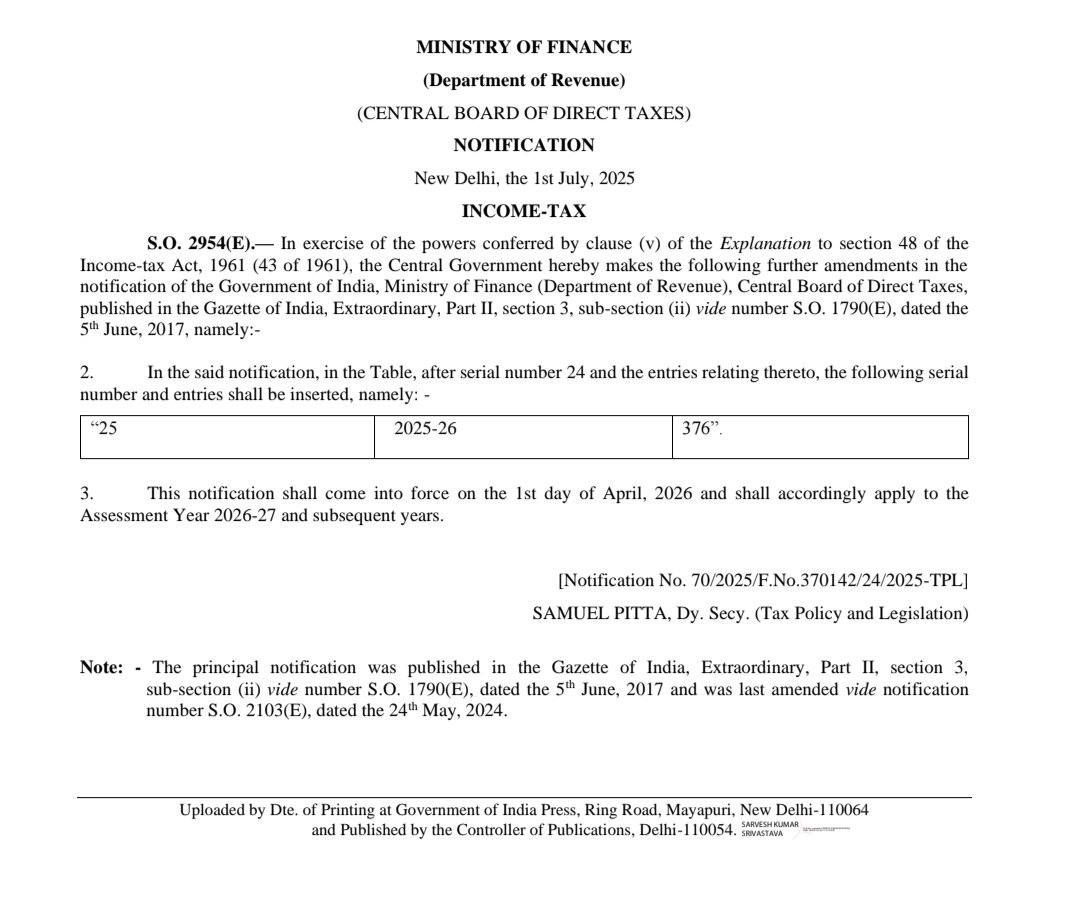

CII for FY 25-26 notified

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.