TDS RATE CHART for the FY 2026-27

Table of Contents

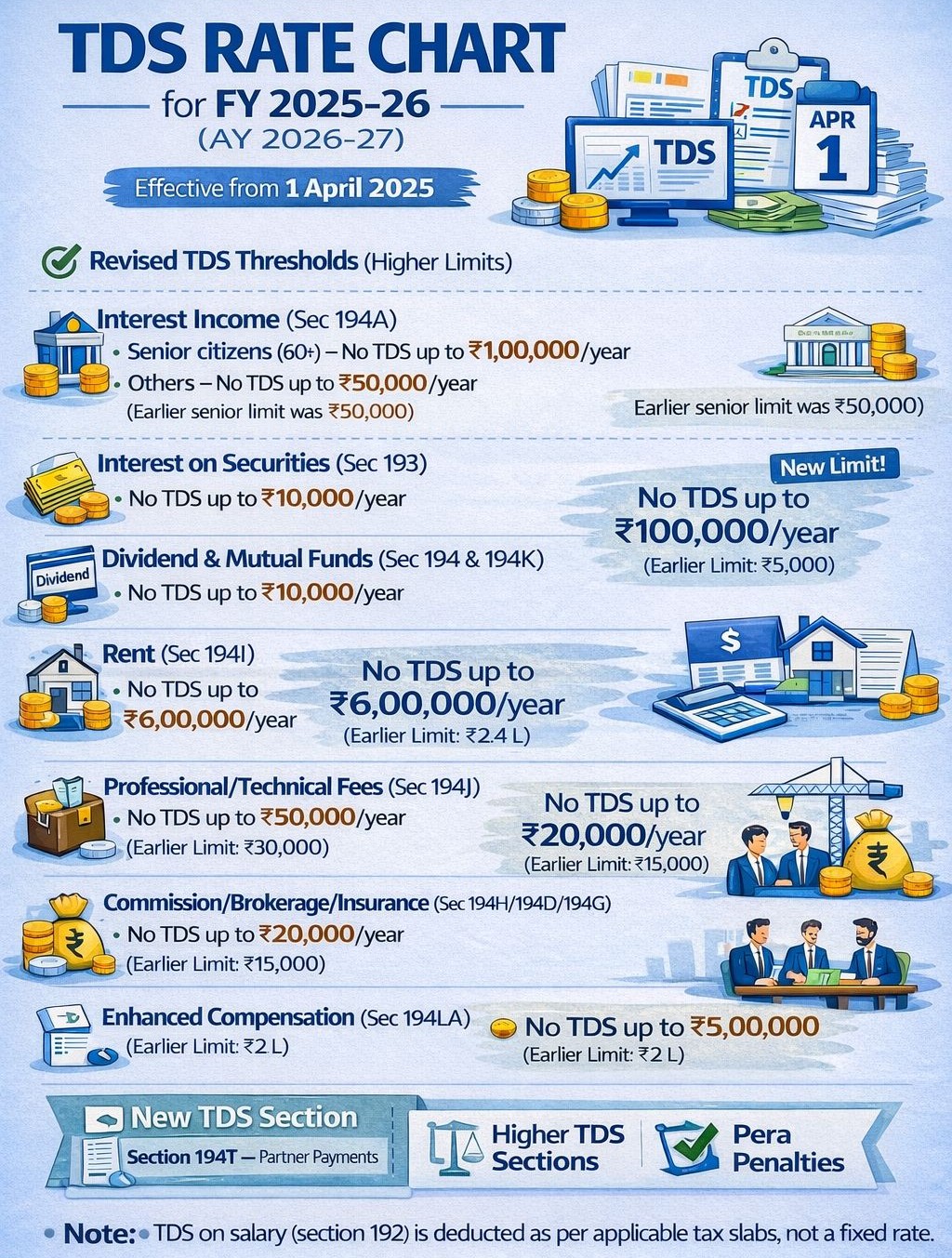

Tax Deducted at Source (TDS) RATE CHART for the FY 2025-26

Q.: How can the TDS be deposited?

A corporate assessee and other business assessees are required to pay taxes (including TDS) via internet or debit cards electronically. The deductor must fill in the Challan No. ITNS 281 to deposit the tax.

Other deductors may deposit the tax so deducted in any branch of the Reserve Bank of India, the State Bank of India, or any authorised bank.

Q.: When is the deadline for submitting TDS?

Taxes deducted during the month must be deposited on or before the due date the following dates.

| Type of Deductor | Mode of payment of TDS | Due Date for deposit of TDS | ||

|

Office of Government |

Without Income-tax Challan |

On the same day on which tax is deducted |

||

| With Income-tax Challan ITNS 281 | Within 7 days from the end of the month in which tax is deducted | |||

| Other Deductor | With Income-tax Challan ITNS 281 |

|

Q.: What are the ramifications of failing to deduct or pay TDS?

If any person who is responsible for deducting tax at source fails to deduct the whole or any part of the tax or fails to deposit the same to the credit of the Central government after deduction, he is considered to be an assessee-in-default.

If the deductor does not deduct tax at source, the deductor is liable for paying an amount of tax he failed to deduct at an interest rate of 1% for each month or part thereof. In the event that the tax deducted is not deposited at the origin, however, the applicant will be liable to pay interest of 1,5% on or part of the tax that he did not deposit with the central government loan for each month.

Apart from this in accordance with Article 40(a)(ia) of the law, the taxable income of the buyer will not be paid for at least 30 percent of the purchasing value that was responsible for TDS.

Q.: If the buyer pays tax due on the income reported in the return of income, is the seller considered as the assessee in default?

According to Section 201 of the Income-tax Act, a deductor who fails to deduct tax at source is not considered in default if the payee has taken such amount into account when computing income in the return and has paid the tax due on such disclosed income. A certificate is to be obtained in Form No. 26A and submitted electronically by the deductor from the chartered accountable.

Thus, the buyer is not considered an assessee-in-default if the seller has taken the purchase amount into account when calculating his income and has paid the tax due on the income declared in the return.

Q.: What is the deadline for submitting a TDS return?

The tax deducted at source statement required by this provision must be filed with the Income-tax Department on or before the following due date:

| Quarter | Due Date |

| April- June | 31st July of the Financial Year |

| July- September | 31st October of the Financial Year |

| October- December | 31st January of the Financial Year |

| January- March | 31st May of the financial year immediately following the financial year in which deduction is made |

If you fail to file your TDS return on time, you will be charged a late filing fee under Section 234E. The price for failing to provide the TDS/TCS Statement would be charged at the rate of Rs. 200 per day that the failure continues. The amount of the fee, however, must not exceed the total amount deductible or collectible, as applicable. The cost must be paid before the late TDS/TCS Statement may be submitted.

A person who fails to file the TDS return or fails to file it by the required date is subject to a penalty under Section 271H. If you provide inaccurate information on your TDS return, you will face a penalty under Section 271H. The minimum penalty for failing to file a TDS return or providing inaccurate information is Rs. 10,000, with a maximum penalty of Rs. 100,000.

Q.: What are the ramifications of being an assessee in default under the Income Tax Act of 1961?

The following are the consequences of being an assessee in default:

-

Interest levied under Section 220.

Simple interest at the rate of one percent per month is payable on any amount not paid within the time period specified in the notice under Section 156.

Furthermore, this interest can only be levied until the Purchaser of the Goods files the ROI. However, if all three of the following requirements are met, the Principle Chief Commissioner / Chief Commissioner / Principle Commissioner/Commissioner might lower the interest:

- Payment of such sum has/would cause actual hardship to the assessee.

- The assessee’s default was caused by circumstances beyond his or her control.

- Assessee has cooperated in the assessment/recovery procedures investigation.

-

Section 221 imposes a penalty.

The Assessing Officer may order the payment of a penalty, which can be any sum up to the amount owed in tax arrears. If the AO is satisfied that the default was for good and sufficient reasons, he or she may refuse to direct the penalty.

-

Sections 222, 227, 229, and 232 govern recovery proceedings.

Apart from penalties, recovery proceedings must be initiated against the assessee/person responsible under the Act’s sections 222 (Certificate to Tax Recovery Officer), 227 (Recovery through State Government), 229 (Recovery of penalties, fines, interest, and other sums), or 232 (Recovery by suit or under other law not affected).

-

Proceedings for Prosecution.

Depending on the nature and severity of the default, the repercussions may include prosecution under Chapter XXII of the Income Tax Act of 1961 sections 276BB and 276C. If a person fails to pay the tax collected to the credit of the Central Government, he shall be punished by rigorous imprisonment for a time of not less than three months but not more than seven years, as well as a fine (Section 276BB).

TDS Rate chart for FY 2024-25

TCS Rate Chart for FY 2024-25

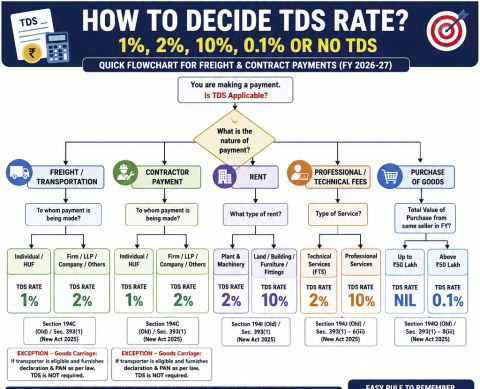

Summary of the TDS Rate Decision Flowchart (FY 2026-27)

Here is a quick guide to determine the correct TDS (Tax Deducted at Source) rate based on the nature of payment.

1. Freight / Transport Payments

Section 194C

- Payment to Individual / HUF → TDS @ 1%

- Payment to Firm / LLP / Company / Others → TDS @ 2%

Exception: No TDS if the transporter owns 10 or fewer goods carriages and furnishes a valid declaration/PAN.

2. Contractor Payments

Section 194C

- Payment to Individual / HUF → TDS @ 1%

- Payment to Firm / LLP / Company / Others → TDS @ 2%

Exception: No TDS if the contractor’s annual receipts are below the prescribed threshold limits.

3. Rent Payments

Section 194I

- Rent for Plant & Machinery → TDS @ 2%

- Rent for Land, Building, Furniture, or Fittings → TDS @ 10%

4. Professional / Technical Services

Section 194J

- Technical Services Fees → TDS @ 2%

- Professional Services Fees (CA, Lawyer, Doctor, Architect, Consultant, etc.) → TDS @ 10%

5. Purchase of Goods

Section 194Q : Based on total purchases from the same seller during the financial year:

- Up to INR 50 lakh → No TDS

- Above INR 50 lakh → TDS @ 0.1% on the amount exceeding INR 50 lakh

A Practical on TDS Provisions in India

Most TDS mistakes are not rate-related , they arise from wrong section selection during transaction design or voucher classification. Below is a structured, quick-reference chart grouping TDS sections by nature of payment to make compliance easier during vendor onboarding, audits, and month-end closing.

Salary & Investment Income

| Section | Nature of Payment | TDS Rate |

|---|---|---|

| 192 | Salary | As per slab rates |

| 192A | Premature PF withdrawal | 10% |

| 193 | Interest on securities | 10% |

| 194 | Dividend income | 10% |

Interest, Winnings & Insurance Payouts

| Section | Nature of Payment | TDS Rate |

|---|---|---|

| 194A | Interest (bank deposits, loans, FDs) | 10% |

| 194B | Lottery/game winnings | 30% |

| 194BB | Horse race winnings | 30% |

| 194DA | Life insurance maturity payout | 5% |

Business & Professional Payments

| Section | Nature of Payment | TDS Rate |

|---|---|---|

| 194C | Contractors | 1% (Individual/HUF) 2% (Others) |

| 194J | Professional services | 10% |

| 194J – Technical/royalty (FTS) | Technical services | 2% |

| 194H | Commission / brokerage | 5% |

Rent & Property Transactions

| Section | Nature of Payment | TDS Rate |

|---|---|---|

| 194I | Rent – Plant & machinery | 2% |

| 194I | Rent – Land, building, furniture | 10% |

| 194IA | Purchase of immovable property | 1% |

| 194IB | Rent paid by Individual/HUF (not covered under 44AB) | 5% |

Purchase Transactions, Cash Withdrawals & Digital Economy

| Section | Nature of Payment | TDS Rate |

|---|---|---|

| 194Q | Purchase of goods > ₹50 lakh | 0.1% |

| 194O | E‑commerce transactions | 1% |

| 194N | Cash withdrawals > limits | 2% / 5% |

| 194S | Virtual digital assets / crypto | 1% |

Key Compliance Rules Every Team Must Track

- Section 206AA – No PAN : TDS deducted at 20%, or higher prescribed rate, whichever is higher.

- Under Section 206AB Specified Non-Filers (SNFs) : Higher TDS for persons who have not filed returns for the last 2 years and exceed INR 50,000 TDS threshold.

- Nil / Lower Deduction Options : Form 15G / 15H & Section 197 Certificate (lower/NIL TDS order)

- Correct TDS compliance depends on identifying the correct TDS section at the transaction-design stage not during payment posting. Using proper vendor classification to avoid defaults & Reviewing thresholds, exceptions, and PAN/ITR status

- This reference is particularly useful for Month-end TDS review teams, Vendor onboarding & procurement, Internal audit and IFC reviews & Tax compliance monitoring

Quick TDS Rate Reference

| Nature of Payment | TDS Rate |

|---|---|

| Contractor (Individual/HUF) | 1% |

| Contractor (Firm/Company/LLP) | 2% |

| Transporter | 1% / 2% (subject to exemption) |

| Rent – Plant & Machinery | 2% |

| Rent – Land/Building/Furniture | 10% |

| Technical Services | 2% |

| Professional Services | 10% |

| Purchase of Goods (> ₹50 lakh) | 0.1% |

| Purchase of Goods (≤ ₹50 lakh) | Nil |

To determine the correct TDS rate, first identify the nature of payment (contract, transport, rent, professional fee, or purchase of goods), then check the category of the payee and any applicable thresholds or exemptions. The most common rates are 1%, 2%, 10%, 0.1%, or Nil.

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.