APPLICABILITY OF SECTION 44AD ON SPECULATIVE BUSINESS

Table of Contents

APPLICABILITY OF SECTION 44AD ON SPECULATIVE BUSINESS

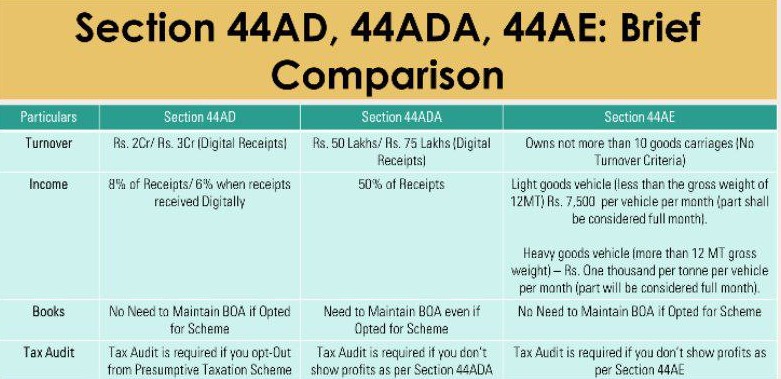

Section 44AD-

Section 44AD of the Income Tax Act allows eligible small taxpayers (individuals, HUFs, and partnership firms excluding LLPs) to declare income on a presumptive basis at 8% of turnover (6% for digital transactions) and without maintaining detailed books of account or audit (subject to turnover limits). In the case of an eligible assessee engaged in an eligible business, a sum equal to eight percent of the total turnover or gross receipts of the assessee in the previous year on account of such business or, as the case may be, a sum higher than the aforesaid sum claimed to have been earned by the eligible assessee, shall be deemed to be the profits and gains of such business chargeable to tax under the head “Profits and gains of business or profession.”

Explanation.—For the purposes of this section,—

A. “eligible assessee” means,—

(i) an individual, Hindu undivided family or a partnership firm, who is a resident, but not a limited liability partnership firm as defined under clause (n) of sub-section (1) of section 2 of the Limited Liability Partnership Act, 2008 (6 of 2009); and

(ii) who has not claimed deduction under any of the sections 10A, 10AA, 10B, 10BA or deduction under any provisions of Chapter VIA under the heading “C. – Deductions in respect of certain incomes” in the relevant assessment year;

B. “eligible business” means,—

(i) any business except the business of plying, hiring or leasing goods carriages referred to in section 44AE; and

(ii) whose total turnover or gross receipts in the previous year does not exceed an amount of one crore rupees.

The above mentioned sections are clear evident that of assessees, falling under specified criteria, may take advantages of Sec.44AD whether it is of speculative nature or not.

Applicability to Speculative Business

Not Applicable to Speculative Business : Section 44AD does NOT apply to speculative business, commission income, brokerage, or agency businesses. This is clearly stated in Section 44AD(6) of the Income Tax Act. Section 44AD(6): The provisions of this section shall not apply to

-

a person carrying on a profession as referred to in section 44AA(1);

-

a person earning income in the nature of commission or brokerage; or

-

a person carrying on any agency business; or

-

a person earning income in the nature of speculative business.

Meaning of Speculative Business

As per Section 43(5) of the Income Tax Act “Speculative transaction” means a transaction in which a contract for the purchase or sale of any commodity, including stocks and shares, is settled otherwise than by the actual delivery or transfer of the commodity or scrips. Examples:

- Intraday trading in shares or securities → Speculative business

- Futures & Options (F&O) trading → Not speculative (specifically excluded from speculative definition under Section 43(5)(d))

Turnover considered for the purpose of Sec.44AD-

Since, a number of transactions in speculative business are involving intra-day transactions, futures and options etc, turnover is based upon the following two situations-

- If delivery of Goods is made-

Turnover = Value of Scrips sold

- If delivery of Goods isn’t made-

In this case profit/loss is booked through increased/decreased value of scrips in future conditions as compared to present ones.

Turnover = Amount of Profit/Loss

Note- In this case even amount of even loss will be taken in positive sense while computing turnover.

| Type of Business/Transaction | Speculative? | 44AD Applicable? | Tax Treatment |

|---|---|---|---|

| Intraday equity trading | Yes | No | Treated as speculative business income (normal taxation, books required if turnover > INR 25 lakh or profit < 6%) |

| F&O trading (Equity, Commodity, Currency) | No | Possible (technically non-speculative business) | Taxed as non-speculative business income; presumptive scheme under 44AD may be opted subject to turnover definition |

| Commission or brokerage business | Not speculative | No | Regular business income (books + audit if limits exceeded) |

| Manufacturing/trading of goods | No | Yes | Normal 44AD presumptive scheme applies |

Conclusion

While F&O trading is not speculative, it’s treated as a business (non-speculative) and can technically opt for presumptive taxation under Section 44AD, provided

-

Turnover is calculated as per ICAI guidance (absolute profit + loss basis), and

-

The taxpayer has no other excluded income (like commission or speculative income).

However, intraday trading (purely speculative) cannot be shown under Section 44AD. It must be reported under “Income from business or profession – speculative business”, with books of accounts maintained.

| Nature of Income | Section 44AD Applicability | Remarks |

|---|---|---|

| Speculative business (intraday trading) | Not allowed | Excluded under Section 44AD(6) |

| Non-speculative business (F&O, delivery-based) | Allowed | Can opt for presumptive scheme if turnover ≤ INR 2 crore (INR 3 crore from AY 2024-25) |

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.