Budget Highlights: Tax Proposals in Finance Bill 2024

Table of Contents

Budget Highlights: Tax Proposals in Finance Bill 2024

Important Direct Tax Proposals:

- Change in Tax Rates:

- Changes in 3 slabs ranging from ₹3 lakhs to ₹12 lakhs result in a tax benefit of ₹10,000.

- Standard Deduction:

- Increased from ₹50,000 to ₹75,000 in the new tax regime. Not available for those opting for the old regime. Tax benefit: ₹7,500.

- Family Pension Deduction:

- Increased from ₹15,000 to ₹25,000 in the new tax regime.

- NPS Contribution Deduction:

- Enhanced from 10% to 14% for private employees under the new tax regime.

- Foreign Companies Tax Rate:

- Reduced from 40% to 35%.

Condition of Salaried Employee

- Uniform Long Term Capital Gain (LTCG) Tax Rate:

- Set at 12.5% for:

- STT paid equity shares and units of equity-oriented funds

- Units purchased in foreign currency

- Bonds or GDRs purchased in foreign currency

- Securities of FIIs

- Set at 12.5% for:

- Removal of Indexation Benefit:

- Indexation for long-term capital gains removed.

- LTCG Exemption Increase:

- Increased from ₹1 lakh to ₹1.25 lakhs for STT paid equity shares and units of equity-oriented funds.

- Period of Holding Changes:

- Reduced from 36 to 24 months for gold, listed debentures, listed bonds, and all units of mutual funds.

- Unlisted shares and immovable property continue to qualify as long-term capital assets after 24 months.

- Capital Gain Treatment for Unlisted Bonds and Debentures:

- Treated as short-term capital gain regardless of holding period.

- Short Term Capital Gain Tax Rate:

- Increased to 20% for STT paid equity shares or units of equity-oriented funds.

- Capital Gain Exemption for Gifts:

- Limited to Individual/HUF.

- Fair Value Excess for Private Companies:

- Amount received in excess of fair value no longer taxable.

- TDS Rate on Commission:

- Reduced from 5% to 2% effective 01-10-24.

- TDS Rate on Rent:

- Reduced from 5% to 2% under section 194-IB.

- Lower TDS Deduction:

- Allowed for buyers and sellers at 0.1% under sections 194Q/206C(1H).

- Consideration of Other TDS/TCS:

- For determining TDS on salary income, ensuring TDS on salary is not less than tax deductible without considering other incomes.

- TCS on Foreign Remittances:

- Can be claimed by the parent for a child’s expenses.

- TCS on Luxury Goods:

- 1% for items above ₹10 lakhs. Motor vehicles already covered.

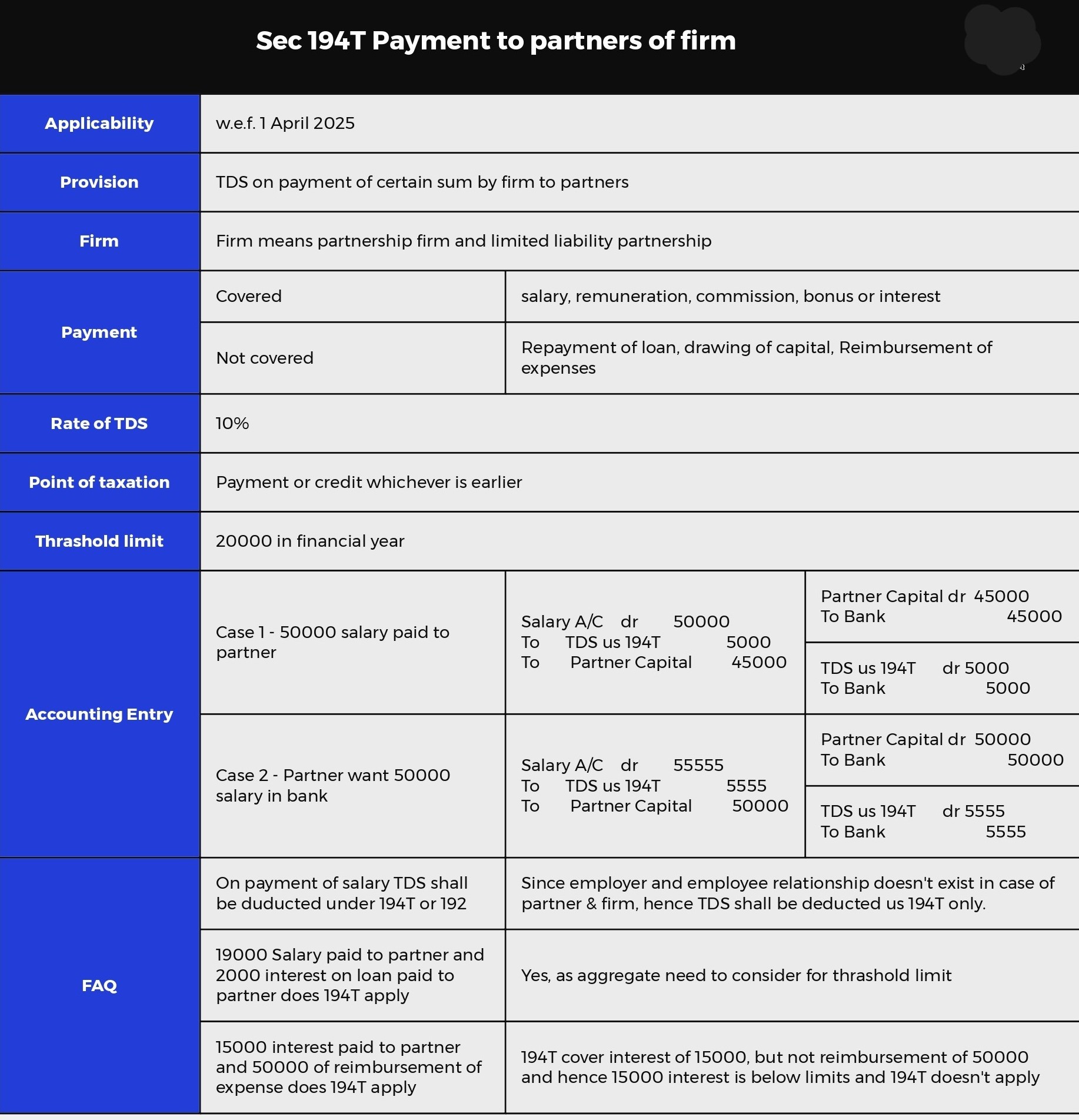

- TDS on Salary and Interest to Partners:

- Above ₹20,000 at 10% under section 194T.

- TDS on Immovable Property:

- Applied on aggregate limit for sales above ₹50 lakhs, even with multiple buyers.

- Interest on Late TCS Payment:

- Increased from 1% to 1.5%.

- Penalty Exemption for Delayed TDS Return:

- Limited to one month from due date.

- Correction of TDS/TCS Returns:

- Not allowed after 6 years.

- Employer NPS Contribution Deduction:

- Increased from 10% to 14%.

- Deduction Disallowance:

- Settlements for law infractions not deductible.

- Partners’ Salary Allowance:

- Slabs changed; first slab up to ₹6 lakhs with deduction allowed to the extent of ₹3 lakhs or 90%, and remaining profits at 60%.

- Vivaad se Vishwas Scheme:

- For disputes filed post 31-01-20: settle by paying only tax amount.

- For pre 31-01-20: settle by paying tax plus 10%.

- Block Assessment for Search Cases:

- Income assessed at 60% without interest and penalty, except in specified circumstances under section 158BFA.

- Search Cases Limit:

- Reduced to 6 years.

- Re-opening of Previous Years:

- Limited to 5 years; requires approval from Additional/Joint Commissioner.

- Reassessment Provisions Revamped:

- Re-opening with approval from Additional/Joint Commissioner.

- Return Filing Period for Notice u/s 148:

- Increased to 3 months; deemed return u/s 139 if filed within 3 months.

- Employer Contribution Deduction:

- Increased to 14% under section 80CCD.

- ITAT Appeals:

- Allowed for penalties under section 158BFA in search cases.

- ITAT Appeal Period:

- Within 2 months from end of month in which appeal is communicated to assess/PCIT.

- Trusts and Section 10(23C) Regime:

- Merged with section 11; no approval application for section 10(23C).

- PCIT Condonation of Delay:

- Allowed if reasonable cause for delay in section 12A application.

- Section 80G Registration:

- Rationalized timelines.

- 12A/80G Registration Applications:

- Decided within 6 months from end of quarter in which application is filed.

- Merger of Charitable Trusts:

- No exit tax for merger with similar trusts registered under sections 12AB/10(23C).

- Income from Letting Residential Houses:

- Not taxed under Profits and Gains of Business or Profession.

- Foreign Assets Non-Disclosure Penalty:

- Up to ₹20 lakhs not imposed.

- Aadhaar Enrolment ID for PAN Linking:

- Abolished; Aadhaar number must be intimated.

- Commissioner Appeal Power:

- Can set aside ex parte assessments; completion within one year from end of financial year.

- Belated Return Assessment:

- Limit of 12 months from end of FY in which return is filed.

- Withholding of Refund:

- Allowed even if not prejudicial to revenue interest.

- Withholding of Refund for Reassessment:

- Allowed up to 60 days; interest on delayed refund accordingly.

- Buyback of Shares:

- Treated as dividend; taxable under Income from Other Sources. 10% TDS applies on income from buyback.

- Presumptive Taxation for Non-Resident Cruise Operators:

- Introduced at 20%; leasing company rental income exempt if both are subsidiaries of the same holding foreign company.

- Equalization Levy:

- 2% on e-commerce supplies abolished.

- TPO Authority:

- To deal with specified domestic transactions not referred by AO, earlier only international transactions.

Important GST Proposals:

- ITC Availment Extension:

- For FY 2017-18 to 2020-21, extended to 30-11-21. No refund for already reversed ITC.

- Waiver of Interest and Penalty:

- For periods 2017-18 to 2019-20 before issue of order under sections 73/74.

- ITC on Cancelled to Revoked Period:

- Available if returns filed within 30 days of revocation, subject to section 16(4) time limit.

- ENA, Rectified Spirit:

- Brought outside GST.

- ITC Blocked for Payment u/s 74:

- Restricted to demand till FY 2023-24.

- Section 73, 74 Operation:

- Until 31-03-2024; new section 74A for uniform SCN period of 42 months with higher penalty.

- No Refund for Export Duty Goods:

- Whether export made under LUT or on payment of tax.

- IGST Payment Refund Stopped:

- Except for notified persons and goods/services.

- Conditional Waiver of Interest and Penalty:

- For cases FY 2017-18 to 2019-20 under new section 28A.

- Pre-Deposit Rate for GSTAT Appeals:

- Reduced from 20% to 10%; maximum pre-deposit before first appellate authority and GSTAT also reduced.

- Mandatory Monthly TDS Returns:

- Introduced irrespective of tax liability.

- Summons Attendance:

- Can be attended by authorized persons.

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.