Guide to Choosing Correct ITR Form for Stock Market Income

Table of Contents

Guide to Choosing Correct ITR Form for Stock Market Income

For those whose yearly income exceed the basic exemption limit, they must file an ITR. To finish the electronic filing of their income tax returns, taxpayers must fill out a variety of paperwork. These ITR forms are divided according to the type of income. But each situation requires a different ITR form, so choosing the right one can be difficult.

For salaried individuals who earn money from intraday stock exchange or futures and options (F&O) trading, it is important to file the correct Income tax return form to accurately report your income. Different Types of Income Tax Return (ITR) forms and their respective uses:

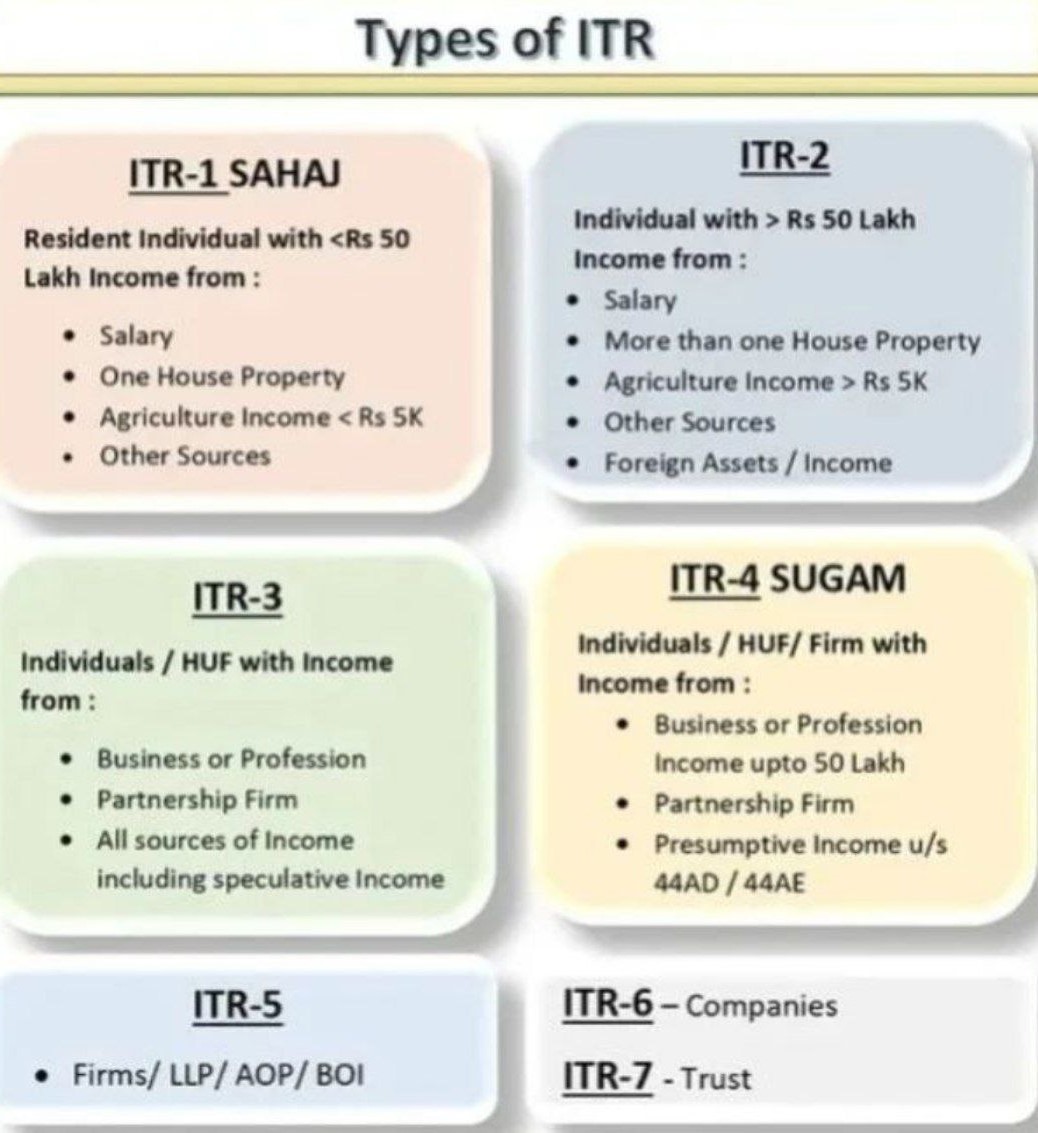

ITR 1

- Eligibility: Individuals residing in India with a total income of up to Rs 50 lakh. Sources of Income: Salary, house property, and other sources. Not Applicable for: Non-Resident Indians (NRIs). Salaried taxpayers can file ITR-1 using Form 16.

ITR 2

- Individuals and Hindu Undivided Families (HUF) with income from sources other than business or profession. Sources of Income: Salary, house property, capital gains, and other sources.

- Can be filed by salaried people who have made profits or losses from stock purchases and sales. NRIs earning from similar sources may also use ITR-2.

ITR 3

- Individuals with income from business or profession. Form ITR-3 is specifically designed for this purpose. Individuals can use Income tax return form ITR-3 to report income from the following sources:

- Salary: Income from your job or employment.

- House Property: Income from real estate.

- Capital Gains: Profits from the sale of assets such as stocks or property.

- Business or Profession: Income from a business or trade, including presumptive income.

- Other Sources: Any additional income, such as interest or dividends.

- Salaried individuals earning from intraday stock exchange or futures and options trading should file ITR-3. Using ITR-3 ensures comprehensive reporting of your diverse income streams, which is crucial for accurate tax filing and compliance.

ITR 4

- Eligibility: Individuals, HUFs, and partnership firms subject to a presumptive taxation system.

- Sources of Income:

- Business with turnover up to Rs 2 crore (section 44AD).

- Profession with turnover up to Rs 50 lakh (section 44ADA).

- Usage: Freelancers in notified professions can use ITR-4.

ITR 5

- LLPs, partnership firms, Association of Persons (AOP), and Body of Individuals (BOI). ITR 5 filling required To disclose profits from businesses and professions, as well as other sources of income.

ITR 6

- Companies (excluding those claiming exemption under section 11). ITR 6 filling required to report income from industry or profession and other forms of income.

ITR 7

- Entities including companies, partnerships, and trusts exempt from paying income tax. ITR 7 filling required, Income tax dept Govt tax return for exempt entities like NGO or NPO etc

Summary of Income tax Return From to use for reporting stock market income.

Choosing the correct ITR form is crucial for accurate reporting of your stock market income. If you are unsure which form to use, it is advisable to consult with your Chartered Accountant to ensure a smooth and correct filing process. Choosing the correct ITR form is crucial for accurate tax reporting. which ITR form to use for reporting stock market income. To clear up any confusion, here is a quick summary are mention here under :

- Salary + Capital Gains: Use Income tax return form ITR-2

- Salary + Capital Gains + Intraday Trading: Use Income tax return form ITR-3

- Salary + Capital Gains + F&O Trading: Use Income tax return form ITR-3 (or ITR-4 if opting for presumptive taxation)

- Only Intraday Trading: Use Income tax return form ITR-3

- Only F&O Trading: Use Income tax return form ITR-3 (or ITR-4 if opting for presumptive taxation)

- Salary + F&O Trading: Use Income tax return form ITR-3 (or ITR-4 if opting for presumptive taxation)

- Salary + Intraday Trading: Use Income tax return form ITR-3

Consequences and Solutions for Filing the Wrong ITR Form

Filing the incorrect Income Tax Return (ITR) form can lead to several complications. Understanding these and knowing how to rectify them is crucial to avoid penalties and ensure compliance. By understanding these consequences and solutions, you can ensure compliance with tax laws and avoid potential issues with the Income Tax Department. Here’s what happens and how you can address the situation:

What is the Consequences of Filing the Wrong ITR Form?

- Rejection of ITR:

- The Income Tax Department may reject your return if it’s filed in the wrong form. This causes delays in processing and can lead to penalties for late filing if the mistake is not corrected promptly.

- Scrutiny or Assessment:

- Filing with the wrong form could trigger additional scrutiny from tax authorities, They might request you to re-file using the correct form, potentially causing further delays and complications.

What is solutions to Address Filing the Wrong ITR Form?

- Revised Return:

- If you identify the error before the ITR filing deadline (typically July 31st for most taxpayers), you can file a revised return using the correct form. There’s no limit on the number of revised returns you can submit within the assessment year, allowing you multiple opportunities to correct mistakes.

- Defective Return Notice:

- If the error is identified by the tax department after the deadline, you might receive a “defective return notice” under Section 139(9) of the Income Tax Act. You are given 15 days to rectify the mistake by filing a revised return. If needed, you can request an extension for this period. Timely rectification ensures your return is processed correctly and helps avoid penalties.

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.