FAQ’s on Tax Audit Under Income Tax Act 1961

Table of Contents

FREQUENTLY ASKED QUESTIONS ON TAX AUDIT UNDER INCOME TAX ACT

Q-1. What provision is stated in section 44AB?

Ans. This provision specifies that taxpayers must perform an audit of their company or profession in order to provide an audit report for taxes purposes.

Q-2. Who does tax audits?

Ans. A tax audit is performed by a practicing chartered accountant or the appropriate authorities.

Q-3. What is the consequence for failing to comply with Section 44AB?

Ans. If you fail to comply with Section 44AB, you will be fined 0.5 percent of your entire sales, turnover, or gross revenues, or Rs. 1.5 lakh, whichever is less.

Q-4. Who is exempt from having a tax audit performed?

Ans. The following individuals are exempt from having a tax audit performed:

- Any assessee whose income is derived from section 44B.

- If an assessee’s books of accounts are audited under other laws, he or she is not required to have another tax audit performed under section 44AB. A tax report, in particular, must be filed in Form 3CA, Form 3CB, or Form 3CD.

- Any assessee whose income is derived from section 44BBA.

Q-5. Who is not eligible to be a tax auditor?

Ans. There are several restrictions on the appointment of tax auditors, which are listed below:

- Any member who works part-time is unable to undertake tax audits.

- A chartered accountant cannot audit the accounts of someone to whom he owes more than Rs.10,000.

- Statutory auditor will be considered professional misconduct if he or she accepts the appointment of a Public Sector Undertaking/Government Company/Listed Company and other Public Company with a turnover of Rs 50 crores or more in a year and accepts any other work, assignment, or service in relation to the same.

Undertaking/company on a compensation that exceeds the amount charged for carrying out the same undertaking/statutory company’s audit

- The Chartered Accountant tasked with preparing and maintaining the assessee’s books of account should not audit such accounts.

- Any partner or employee of a professional firm of Chartered Accountants is not permitted to audit the firm’s accounts.

- Assessee’s internal auditor cannot be appointed as a tax auditor.

- An auditor may not take more than 45 tax audit jobs in a fiscal year.

Q-6. Who is not eligible to be a tax auditor?

Ans. There are several restrictions on the appointment of tax auditors, which are listed below:

- Any member who works part-time is unable to undertake tax audits.

- A chartered accountant cannot audit the accounts of someone to whom he owes more than Rs.10, 000.

- Statutory auditor will be considered professional misconduct if he or she accepts the appointment of a Public Sector Undertaking/Government Company/Listed Company and other Public Company with a turnover of Rs 50 crores or more in a year and accepts any other work, assignment, or service in relation to the same.

Undertaking/company on a compensation that exceeds the amount charged for carrying out the same undertaking/statutory company’s audit

- The Chartered Accountant tasked with preparing and maintaining the assessee’s books of account should not audit such accounts.

- Any partner or employee of a professional firm of Chartered Accountants is not permitted to audit the firm’s accounts.

- An assessee’s internal auditor cannot be appointed as a tax auditor.

- Auditor may not take more than 45 tax audit jobs in a fiscal year.

Q-7. What exactly is an audit report?

Ans : A tax auditor must submit his report in a prescribed form, which could be Form 3CA or Form 3CB, depending on whether the person carrying on business or profession is already mandated to have his accounts audited under another law.

Form No. 3CB is required to submit when the person engaged in the business or profession is not mandated to have his accounts audited under another law.

The tax auditor must provide the specified particulars in Form No. 3CD, which is part of the audit report, in the event of either of the aforementioned audit reports.

Q-8. When and how should tax audit reports be provided?

Ans : The tax auditor must submit a tax audit report online using his login credentials as a Chartered Accountant. Taxpayers must also provide CA information in their login portal.

- Once the tax auditor submits the audit report, the taxpayer should accept or reject it using their login site. If the audit report is refused for any reason, all steps must be repeated until the taxpayer accepts the audit report.

- You must file the tax audit report on or before the due date of the income tax return. It is the 30th of November of the following year if the taxpayer has entered into an overseas transaction, and the 30th of September (extended to the 30th of November for AY 2021-22) of the following year for all other taxpayers.

Q-9. What happens if a person is compelled to have his or her accounts audited under another legislation, such as mandatory audits of businesses under company law provisions?

- In such circumstances, the taxpayer is not required to have his accounts audited for income tax reasons again. It is sufficient if the accounts are audited under such other legislation before the return’s due date. Under income tax legislation, the taxpayer may provide this specified audit report.

Q-10. What is the difference between sales turnover and gross receipt in a tax audit?

Sales Turnover– The aggregate amount for which an enterprise affects sales is referred to as sales turnover.

- Gross Receipts– the Income Tax Act does not define this word. Gross revenues comprise all receipts derived from the practise of a profession.

Q-11. How do you measure a commission agent’s sales turnover?

- The turnover of a commission agency or a person selling items on consignment is defined by the transfer of ownership risk or reward. If the property in goods or all substantial risks and benefits of goods ownership remain with the principle, the relevant selling price will not be included in the commission agent’s turnover.

- However, when the commission agent owns the products, bears considerable risk, and reaps the benefits of ownership, the selling price received/receivable is included in his turnover.

Q-12. How do you determine a stockbroker’s sales turnover?

- When a stockbroker purchases stocks on behalf of a customer, the securities are not transferred into his name but are delivered in the customer’s name.

- This is also valid in the case of sales. The stockbroker holds delivery on behalf of his client. The ownership of securities is not transferred to share brokers. Only brokerage must be included when calculating the value of the turnover.

Q-13. How do you calculate sales turnover when you have numerous businesses?

- If an assessee operates more than one business, the sale turnover or gross revenues from all businesses will be aggregated; however, if the assessee chooses the presumptive tax scheme, the turnover of such business will be omitted when calculating total sales turnover or gross receipts.

Q-14. How can I provide the Income Tax Department with a tax audit report?

- A Chartered Accountant can electronically file the audit report with the income tax department. The tax auditor would instantly post the report to the income tax’s official website. The assessee must authorise and appoint a Chartered Accountant from his e-filing account in order to provide the report.

- The date of the taxpayer’s approval of the report would be deemed the date of submission of the audit report. If the assessee does not accept or approve the tax audit report, it will be considered pending as if it had not been filed.

Q-15. How many tax audit reports may a Chartered Accountant sign?

- A practising CA can perform up to 60 tax audits throughout an assessment year. The Institute of Chartered Accountants of India clarified that audits specified under statutes that require assessees to provide audit reports will not be counted toward the specified number of tax audit assignments if the auditee’s turnover is less than the turnover limit specified in section 44AB of the IT Act.

Q-16. Is it possible to amend a tax audit report?

Generally, an audit report under section 44AB should not be amended, but a member can do so on the following grounds:

Revision of a company’s accounts following its acceptance in an AGM;

-

- A change in the law;

- Shift in interpretation.

- As a result, the audit report, once filed, might be amended on the aforementioned grounds.

Q-17. Is there a penalty for submitting an audit report late?

- If a person fails to have his accounts audited or fails to provide the audit report, the assessing officer may order him to pay a penalty equivalent to the lesser of 0.5 percent of the total sale, turnover/gross revenues or 1,50,000 rupees.

- It should be stressed, however, that there would be no punishment if the failure was due to a justifiable cause.

Q-18. Is Form 3CD reporting performed according to books of account or after modification in accordance with Income Computation and Disclosure Standards?

- According to the preamble to the Income Computation and Disclosure Standards, ICDS is applicable for income computation chargeable under Profit and Gains of Business or Profession or Income from Other Sources, but not for bookkeeping.

Q-19. Should the audit report include the addresses of all locations?

- If books of account are held in various locations, the auditor must supply the addresses of all sites as well as the information of the books of account preserved at each location.

- In the case of a company assessee, the auditor must confirm that Form AOC-5 has been submitted with the ROC under the Companies Act for the keeping of books of account at a location other than the registered office.

- The auditor’s responsibility is not only to provide a list of books of accounts, but also to analyse the books of accounts.

Q-20. Is it necessary to disclose the nature of the assessee’s businesses and any changes to them?

- Clause 10 of Form 3CD requires the assessee to disclose the nature of each business or profession carried out by him or her during the preceding year. Any changes in the nature of the business should be stated explicitly. A transition from manufacturer to trader is one example of a change that necessitates reporting.

- Any addition to, or permanent discontinuation of, a line of business is another example of a change that necessitates reporting. However, a temporary stoppage of operations may not constitute a change and so does not need to be notified.

Q-21. What types of documents should taxpayers keep in order to comply with the requirement to keep books of account?

The following papers should be kept:

- A cash book

- Journal, if books of accounts are kept in accordance with the commercial accounting system.

- Ledgers.

- Copies of invoices and carbon copies or counterfoils of receipts produced by the assessee for more than 25 rupees.

- Original bills given to the assessee and receipts for expenditures spent by him;

- Signed vouchers, if no invoices or receipts are given and the spending amount is less than 50 rupees, if the cash book does not have enough details about these expenditures.

Q-22. How many tax audits can a CA sign off on?

- Chartered Accountants are limited to a specific number of tax audits each year, as determined by the ICAI. Here are the specifics regarding the ICAI-mandated Tax Audit limit for CAs.

CA TAX AUDIT LIMIT

The audit is carried out by a Chartered Accountant or a company of chartered accountants in accordance with tax audit regulations. A single person can only undertake 60 audits in a fiscal year. In the event of a partnership firm, this restriction applies to each partner who is a chartered accountant.

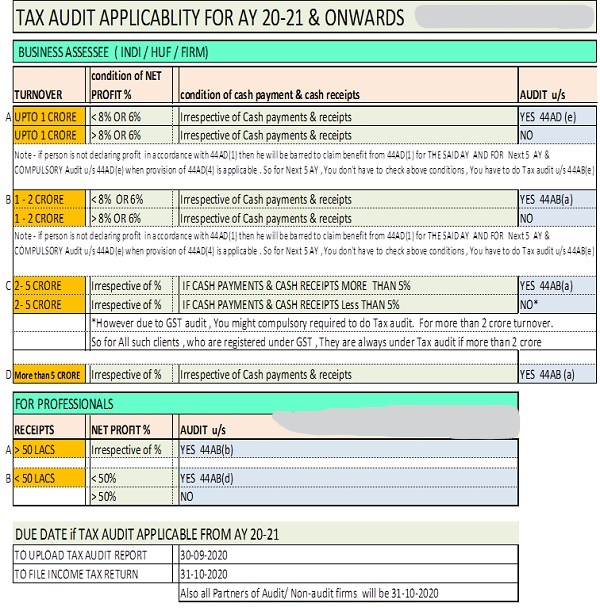

Q-23. What is the tax audit limit ?

Income Tax Audit Applicability & Application in India

- If a taxpayer’s sales, turnover, or gross revenues surpass Rs. 1 crore in a fiscal year, he or she must have a tax audit performed. The Rs. 1 Crore threshold limit for a tax audit is planned to be enhanced to Rs. 5 Crore from AY 2020-21 (FY 2019-20) if the following two requirements are met:

(i) The entire amount received in cash during the preceding year, including sales, turnover, or gross receipts, does not exceed 5% of total turnover/gross receipts; and

(ii) The total of all cash payments made during the preceding year, including the amount paid for expenditure, does not exceed 5% of the total payment.

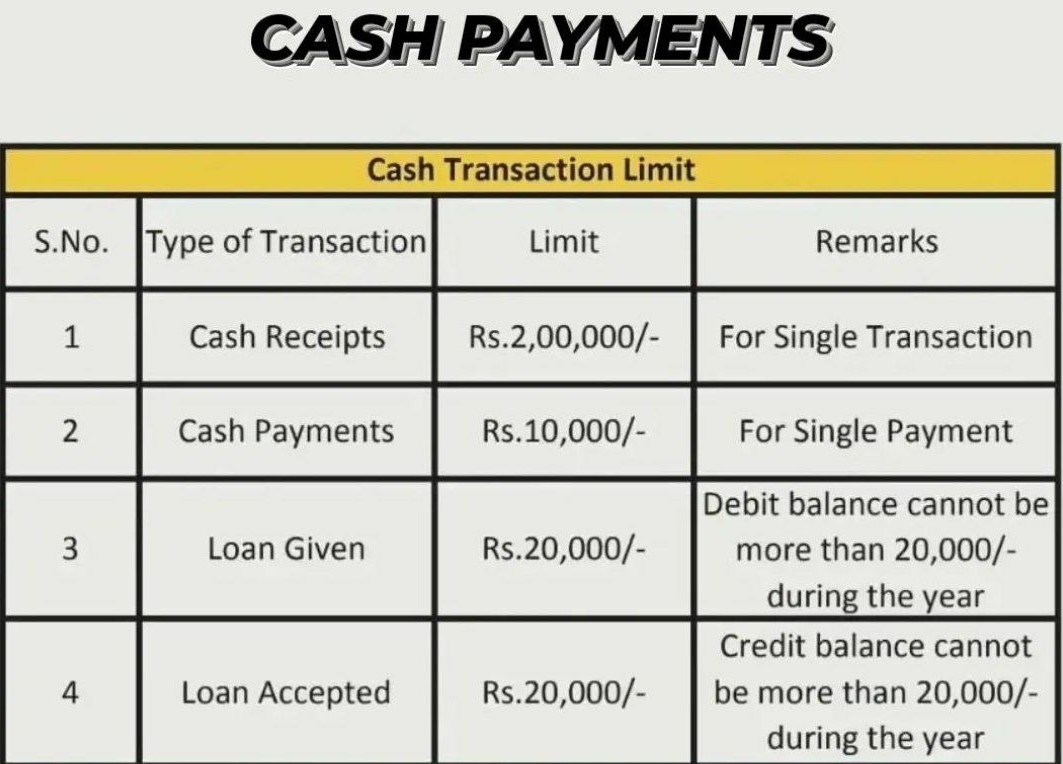

Q-24. What is treatment of cash payment or receipt under the income tax Act ?

Generally, an audit report under section 44AB required to be report the cash transaction exceed more than certain limit. a member can do so on the following grounds:

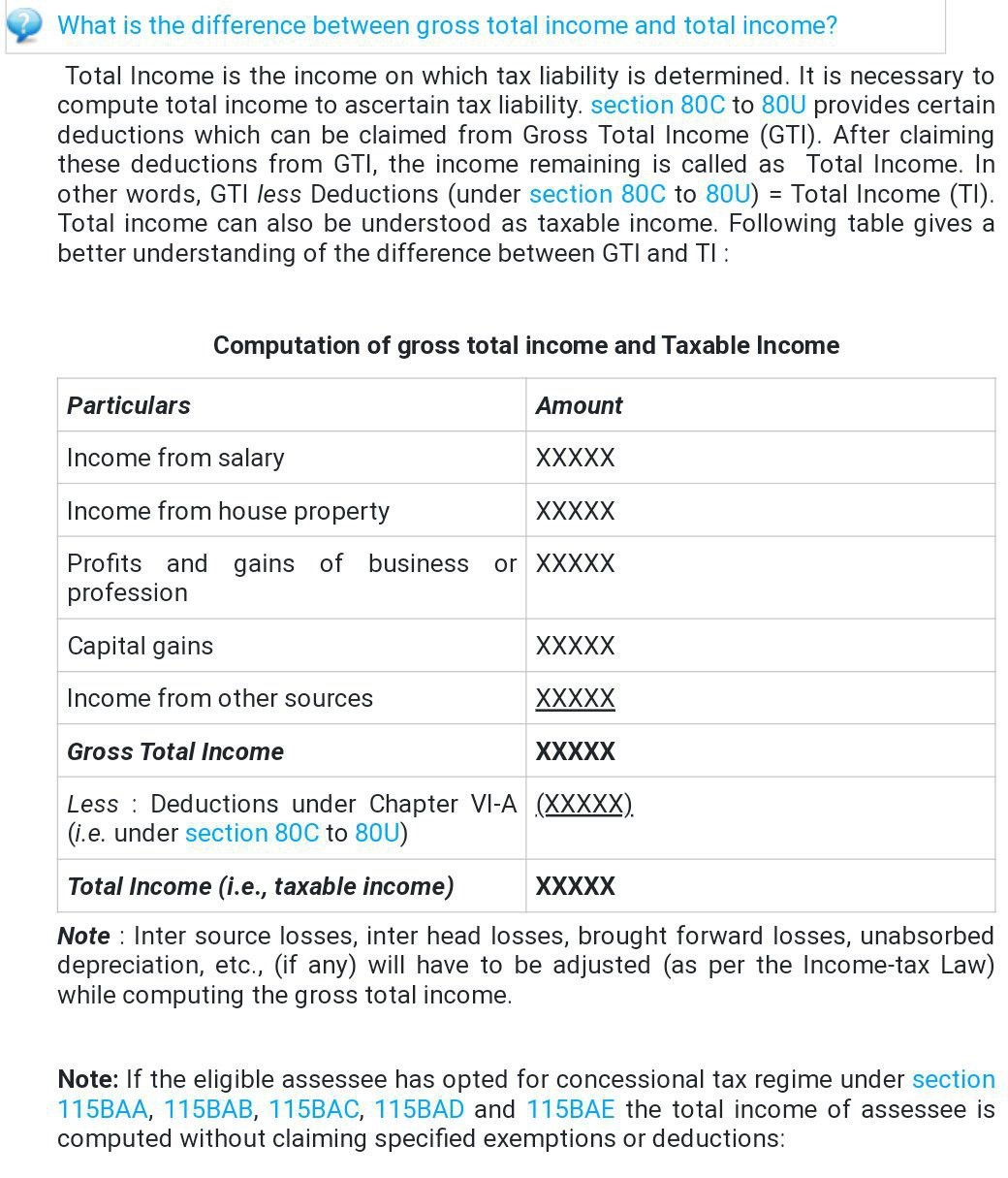

Q-25 what is Difference between Gross Total Income and Total Income?

I hope the FAQs have answered at least some of your questions. Tax audits are not anything to be concerned about if you conduct your business properly and file returns on time. Assure that if you fall into the category of taxpayer, you follow all compliances on time.

Popular Articles related to Tax Audit :

- Amendment in Tax Audit u/s 44AB

- Limit Applicable for tax Audit U/S 44 AB under Income Tax

- Tax Audit Check List

- Tax Audit Updated 01.08.2022 Under the Income Tax Act

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.