All about Income tax return (ITR) filing via ITR-U Form

Table of Contents

Income tax return (ITR) filing via ITR-U

What Does Income Tax Return Filing via ITR‑U Mean? (Updated for 2026)

The concept of filing an updated income tax return was introduced through the Finance Act, 2022, to give taxpayers an extended opportunity to correct or declare additional income. Under this provision, taxpayers who missed filing their original or belated return or wish to rectify errors or omissions can file an updated return within 24 months from the end of the relevant Assessment Year (AY). To operationalise this mechanism, the CBDT notified Rule 12AC along with a dedicated form called ITR‑U. This form must be furnished whenever a taxpayer opts to file an updated return for any assessment year permitted under the law. Key Features of ITR‑U (As Applicable in 2026)

24‑Month Extended Time Window :

- Taxpayers are allowed to file an updated return Up to 24 months (2 years) from the end of the relevant AY. Like, for example, for AY 2024–25, an updated return can be filed up to 31 March 2027. This additional window helps individuals correct underreported income, missed disclosures, or other errors.

- Applicability of Section 139(8A) : Section 139(8A) permits filing an ITR‑U except in specific barred situations, such as Search or seizure cases, Survey operations, Cases involving prosecution, Returns with no additional tax outflow and Loss returns to reduce tax liability

ITR‑U May Be Filed Even If

- The taxpayer did not file the original or belated return. The taxpayer wishes to revise earlier disclosures and Additional income needs to be reported voluntarily

Updated Return for Earlier Years

- Since the provision came into effect on 1 April 2022, taxpayers were initially allowed to update returns for AY 2020–21 and AY 2021–22. This has continued year after year, making ITR‑U available for multiple past assessment years on a rolling basis.

Updated Returns for Earlier Financial Years

- ITR‑U also allowed updated filing for FY 2019–20 (AY 2020–21) and FY 2020–21 (AY 2021–22). Taxpayers could correct omissions or income mismatches through the updated return mechanism for these years as well.

Why ITR‑U Matters in 2026:

- As compliance systems evolve (AIS, TIS, GST data matching, SFT reporting), discrepancies are more easily flagged. ITR‑U serves as a voluntary compliance channel, helping taxpayers Avoid future litigation, Correct mistakes proactively, Regularise income reporting and Reduce penalties by timely disclosure

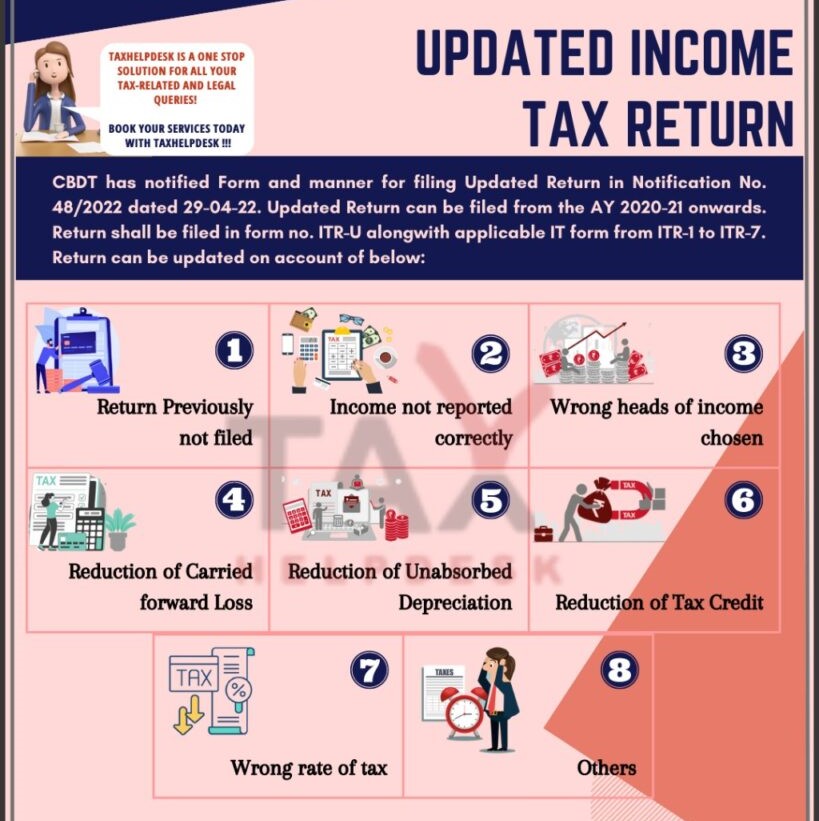

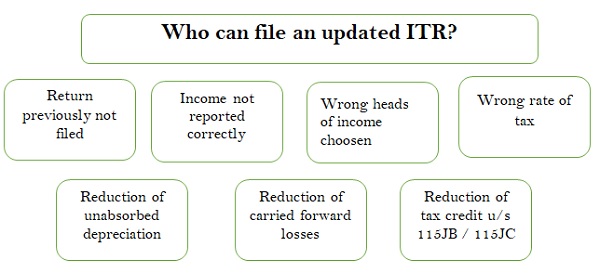

What are case in Which ITR-U Can be Filed ?

- Wrong Heads of Income Choosn

- Reduction of unabsorbed Depreciation

- Return Previously not filed.

- Reduction of Carried forward losses

- Income not reported correctly

- Reduction of Tax Credit u/s 115JB/115JC

- Wrong rate of tax

Note: Taxpayers will be allowed to file only 1 such correction (updated return) per AY.

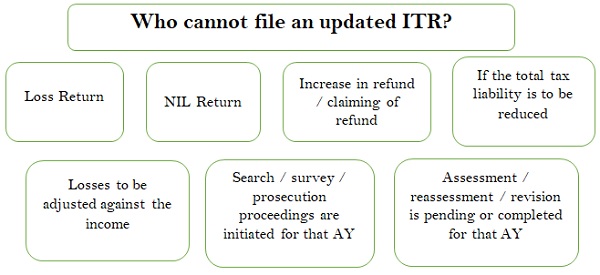

What are the case in which ITR-U Form Cannot be filed?

- Income tax return is reducing the income tax liability from the return filed earlier

- Updated return is a return of the loss

- Return result increases the income tax refund

- Any proceedings for Assessment / Reassessment/Revision/Recomputation is Pending or Completed for Said A.Y.

- Income tax Act will not allow to file the updated return if there is no additional tax outgo

- Search/Survey/Prosecution are Initiated for said A.Y.

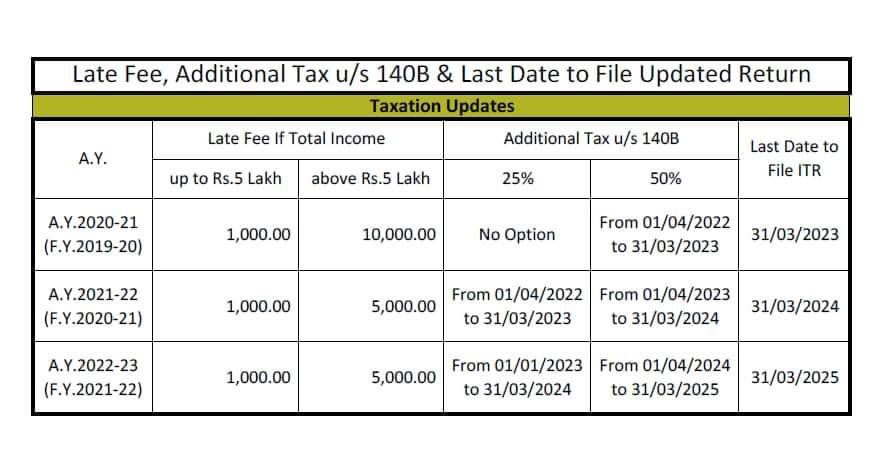

Additional Tax:

- The Income tax Act requires that the taxpayer has to pay an additional 25% interest on the tax due if the updated Income tax return is filed within 12 months from the end of relevant AY.

- While interest will go up to 50% if it is filed after 12 months but before 24 months from the end of relevant AY.

- Taxpayers looking to file the same for FY 19-20 will need to pay the due tax and interest along with an additional 50% amount of such tax and interest.

- For those looking to file for FY 20-21, the additional amount will be 25% of the due tax and interest.

Update about The Late Fee, Additional Tax u/s 140B & last date to File updated Return

Also Read : Tax Audit

Implication of cash transaction under income tax Act

About India Financial Consultancy Corporation Pvt Ltd

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.