Input Tax Credit & GST Refunds for zero-rated supplies

Table of Contents

Input Tax Credit & GST Refunds for zero-rated supplies

Input Tax Credit (ITC)

ITC is the mechanism under the Goods and Services Tax system that allows businesses to claim a credit for the GST paid on their purchases of goods and services, which are used for business purposes. This system ensures that businesses involved in exports or making zero-rated supplies do not bear the tax burden on inputs, thereby making their goods and services more competitive in the global market. This system is designed to eliminate the cascading effect of taxes, where taxes are paid on both inputs and outputs without credit for taxes paid earlier in the supply chain. Key Features of Input Tax Credit

- Set-off Mechanism: Input Tax Credit allows businesses to offset the tax paid on inputs (goods or services) against the GST liability on the output (sales). This means that businesses only need to pay the difference between the GST paid on inputs and the GST collected on outputs.

- No Cascading Tax Effect: Unlike previous tax systems where tax was levied on tax, Input Tax Credit prevents this by allowing businesses to claim credit on taxes paid, which effectively reduces their tax burden.

- Eligibility: Businesses must be registered under GST and meet the required conditions to claim Input Tax Credit.

In case the company is involved in export supply as a third-party exporter, and the relevant rules governing Goods and Services Tax (GST) are being applied, particularly with reference to the sale of Scrips under Notification No. 40/2017 and the Input Tax Credit regulations under Rule 42 and Rule 43. Here’s a breakdown of the key points:

ITC Utilization:

- Once ITC is availed, there is no time limit to utilize the credit. However, when it comes to claiming a refund of Input Tax Credit, the two-year time limit for refund claims applies as per the GST laws. This is an important point when planning for any refunds.

Documentation for Export Supply:

To prove export supplies, the following documents should be maintained:

- Foreign Inward Remittance Certificate (FIRC): Proof of the remittance received for the exported goods.

- Import/Export Code (IEC): Registration number to validate export activities.

- CA Certificate: Certificate issued by a Chartered Accountant to confirm the export details.

- Registration-cum-Membership Certificate (RCMC): Certification related to export activities.

- Copy of Invoice: For goods sold under export.

- Foreign Exchange Earned: Documentation of the foreign exchange earnings from exports.

- List of Directors: The company’s director details.

- Board Resolution: A resolution authorizing export transactions and related activities.

Ineligible ITC and Reversal

- Ineligible Input Tax Credit refers to credits that a dealer is not eligible to claim under the GST law. This could be due to various exclusions such as credits on certain goods and services which are not used in the course of business, or the purchase of goods or services in contravention of GST regulations. If such credits are claimed mistakenly, they must be reversed in accordance with the law.

- Reversal of Input Tax Credit occurs when a dealer has taken ineligible credit, and the same is reversed through proper reporting in the GST return, usually through GSTR-3B.

Lapsed ITC

- Lapsed ITC refers to situations where the dealer was eligible for ITC, but failed to claim it within the stipulated time frame under the law. Section 16(4) imposes a time limit, specifying that ITC must be claimed by the due date of the return for September of the following financial year, or when the annual return is filed, whichever is earlier. If the credit is not claimed within this time frame, it lapses.

Section-wise Analysis ITC Timing

Section 16(4) – Input Tax Credit Timing

-

- This section restricts the ability to claim Input Tax Credit beyond the due date for the return of September following the end of the financial year or the filing of the annual return (whichever is earlier).

Section 18(2) – Input Tax Credit on Stock at the Time of Registration

-

- ITC can be claimed on goods in stock at the time of registration, but the claim must be made within one year of the invoice date. If not claimed within this period, it lapses.

- Dealers must ensure they file the claim on the first GSTR-3B return after registration or no later than one year after the purchase date, whichever is earlier. If they miss this, the credit lapses, but adjustments can be made in subsequent returns if the claim is still within the allowed time frame.

Section 19(3) – Job Work: Input Tax Credit is allowed on goods sent for job work, but if the goods are not returned within one year, it is considered a supply by the principal to the job worker. GST Taxpayer / Dealers must ensure that goods sent for job work are returned within one year, or tax is paid on the supply to the job worker.

GST Refund Procedure for Zero Rated Supplies under Bond or LUT

Zero-Rated Supplies:

Zero-rated supplies refer to exports and supplies to Special Economic Zones (SEZs). These are supplies that are not subject to GST, but businesses can claim a refund of the input tax credit for taxes paid on inputs or services used to make these supplies. Zero-Rated Supplies Include:

- Export of goods or services.

- Supply of goods or services to SEZ developers or units.

Under the Goods and Services Tax framework, exporters can claim a refund of the unutilized Input Tax Credit on zero-rated supplies of goods or services. Zero-rated supplies are those exported outside India or supplied to Special Economic Zones. This article outlines the GST refund procedure for zero-rated supplies under a Bond or Letter of Undertaking, as per the applicable laws. Relevant Legal Provisions:

- Section 16 of the IGST Act, 2017 – Defines zero-rated supplies, including exports and supplies to SEZ units or developers.

- Section 54 of the CGST Act, 2017 – Governs the procedure for claiming refunds.

- Rule 89 to 97A of CGST Rules 2017 – Outlines the refund application procedure.

- Circular-17/17/2017-GST dated 15.11.2017 – Provides detailed guidelines for export refund claims.

Refund Mechanism for zero-rated Supplies:

Under the Integrated Goods and Services Tax (IGST) Act:

- Option 1: Exporters can supply goods or services under a bond or Letter of Undertaking without paying GST, and claim a refund of the input tax credit.

- Option 2: Exporters can pay the GST on exports and claim a refund of the IGST paid.

Conditions for Refund of Unutilized ITC or for zero-rated supplies:

Refunds for unutilized Input Tax Credit are governed under Section 54 of the CGST Act. Refund claims must be filed within two years from the relevant date, which varies depending on the type of export or supply. Relevant Dates:

- Exports by Sea/Air: The date the goods leave India.

- Exports by Land: The date goods cross the border.

- Exports by Post: The date the goods are sent by post.

- Services Exported: The date of receipt of payment or issue of invoice.

Restrictions on GST Refund Claims:

-

- Refund is not allowed if export duties are levied on goods.

- GST Refund cannot be claimed if the supplier avails drawbacks on GST paid.

- Refund is not permitted if the amount is less than ₹1,000 for any tax head.

- GST Refund claims are disallowed if the supplier has been prosecuted for significant tax evasion.

Conditions for GST Refund of Zero-rated Supplies:

Refunds will not be granted in the following cases:

- Goods exported are subject to export duty.

- The supplier has availed of a drawback for the central tax or claims a refund of the integrated tax paid.

Documentary Evidence: GST Refund claims must be accompanied by specific documents like shipping bills, invoices, Bank Realisation Certificates (for services), and proof that the tax incidence was not passed on to others. For claims under two lakh rupees, a declaration suffices.

Provisional Refund: U/s 54(6), exporters can claim provisional refunds on zero-rated supplies, where 90% of the claimed refund amount is processed quickly, and the final settlement is done within 60 days. If the refund is not processed within the stipulated time, interest will be paid to the claimant at 6% per annum.

Calculation of GST Refund: Refunds on zero-rated supplies are calculated using the formula:

Refund Amount=

(Turnover of Zero-Rated Goods+Turnover of Zero-Rated Services)×Net ITCAdjusted Total Turnover\text{Refund Amount} = \frac{(\text{Turnover of Zero-Rated Goods} + \text{Turnover of Zero-Rated Services}) \times \text{Net ITC}}{\text{Adjusted Total Turnover}}Refund Amount=Adjusted Total Turnover(Turnover of Zero-Rated Goods+Turnover of Zero-Rated Services)×Net ITC

Where:

- Net Input Tax Credit is the input tax credit availed on inputs and input services during the relevant period.

- Adjusted Total Turnover is the aggregate turnover, excluding certain taxes and exempt supplies.

Refund for Small Amounts: As per Section 54(14) of the CGST Act, no refund will be issued if the amount is less than ₹1,000.

To claim a GST refund for zero-rated supplies:

The refund procedure for zero-rated supplies under Bond or LUT is structured to ensure exporters can claim back their input tax credits on a timely basis. However, exporters need to be aware of the documentation, time limits, and specific conditions under which refund can be claimed. To claim a Goods and services Tax refund for zero-rated supplies, the following key documents need to be submitted:

- GSTR-1: You must have filed the GSTR-1 return for the relevant tax period. This return should include details of zero-rated supplies made by you.

- GSTR-3B: You must also file your GSTR-3B return for the same period, ensuring that it reflects the payment of GST on inputs used to manufacture or provide the zero-rated supplies.

- Invoice and Shipping Bill: Ensure you have the proper invoice and shipping bill for the zero-rated supplies. These documents must include:

- GSTIN of the supplier.

- Description of the goods or services.

- Value of the supplies.

- The destination of the goods or services if they are being exported.

- Proof of Export: If the zero-rated supplies are exported, you need to provide proof of export. This can include:

- A shipping bill.

- Bill of lading.

- Airway bill.

- Certificate from the Recipient: If the zero-rated supplies were made to a Special Economic Zone or a diplomatic mission, a certificate from the recipient is required. This certificate should confirm that the supplies were received.

Ensure that all these documents are in order before applying for a refund to avoid delays or rejections. The refund claim should typically be filed through the Goods and services Tax portal by using the appropriate application forms like GST RFD-01

Procedure for claiming a GST refund for zero-rated supplies

It is crucial to submit the application within this time frame to avoid the rejection of the refund claim. The procedure for claiming a GST refund for zero-rate supplies, such as exports, involves the following steps:

- File Form GST RFD-01: File your refund application on the GST Portal using Form GST RFD-01. You can apply for refunds for multiple tax periods in one application. Initally you Log in to the GST portal. Then Navigate to the “Refund” section and select “Application for Refund” (Form GST RFD-01). thereafter Choose the appropriate refund category (in this case, for zero-rated supplies or exports). Enter the turnover of zero-rated supplies and Adjusted Total Turnover for the period for which the refund is claimed.

- Net ITC Calculation:

-

- The Net Input Tax Credit will be auto populated by the system, but it can be adjusted downwards considering the ITC availed for CGST/SGST/IGST and Cess in the relevant tax period.

- Exclude ITC related to Capital Goods, Transition Input Tax Credit, and refund claims under Rule 89(4A) (deemed export) or Rule 89(4B) (merchant exporter).

- Ensure Refund Does Not Exceed Limits

-

- The amount claimed in each tax head (CGST/SGST/IGST) should be equal to or less than the balance in your Electronic Credit Ledger.

- Ensure the total refund amount does not exceed the “Maximum Refund Amount” calculated by the system.

- Upload Supporting Documents:

-

- Upload all required documents in the refund application, including the statement of invoices and related documents. Use the Offline Utility to enter document details for Statement 3 (e.g., invoices, debit/credit notes). Validate these documents before submission to ensure correctness. If any errors occur during validation, correct the errors and upload the corrected documents.

- Attach all necessary documents as proof for the export or zero-rated supply, which typically include:

-

-

- Export invoices or tax invoices.

- Shipping bill or export bill of entry.

- Proof of export, such as transport documents or goods dispatch evidence.

- Any other documents as required by the authorities, such as a bank realization certificate (BRC) for exports.

-

- Before submission of the document to the GST portal we needed to ensure Form GSTR-1 and Form GSTR-3B filed for the tax periods covered by the refund claim. For exports of goods, provide details like Shipping Bill and EGM (Export General Manifest). For export of services, provide FIRC (Foreign Inward Remittance Certificate) or BRC (Bank Realization Certificate).

- Bank Account Details: If GST taxpayer are a regular taxpayer (and not a casual or non-resident taxpayer), In case GST taxpayer has enter bank account details for the refund disbursement. However, casual or NRTP taxpayers whose registration was cancelled cannot provide bank details for this refund application.

- Submit the Application: Once you have completed the application and uploaded the necessary documents, submit it electronically on the GST portal.

- Tracking Refund Application: Once submitted, an Application Reference Number (ARN) will be generated. The refund application will be assigned to a Jurisdictional Refund Processing Officer for further processing. You can track the status of the refund through the Track Application Status option on the portal.

- Processing and Verification: The GST authorities will process your application, which includes verifying the details provided and the documents submitted. If everything is in order, the refund request will be approved. the GST Portal will generate ARN, and the refund will be processed by the Refund Processing Officer after scrutinizing the application and attached documents. We can view the status of your refund and download your filed refund application at any time from the portal.

- GST Refund Credit: If the refund claim is approved, the GST refund amount will be credited directly to your designated bank account.

- Time Limit for Claiming GST Refund: The time limit for filing a GST refund claim for zero-rated supplies is 2 years from the date of export or the date of supply, whichever is earlier.

- GST Taxpayer / Dealers should track the due dates for claiming Input Tax Credit, especially in cases involving delayed claims or missed credits. If Input Tax Credit is missing due to errors in invoices or supply documents, dealers should coordinate with suppliers to ensure that amended invoices are provided, and the Input Tax Credit can be auto-populated in GSTR-2A.

IFCCL GST Refund Services:

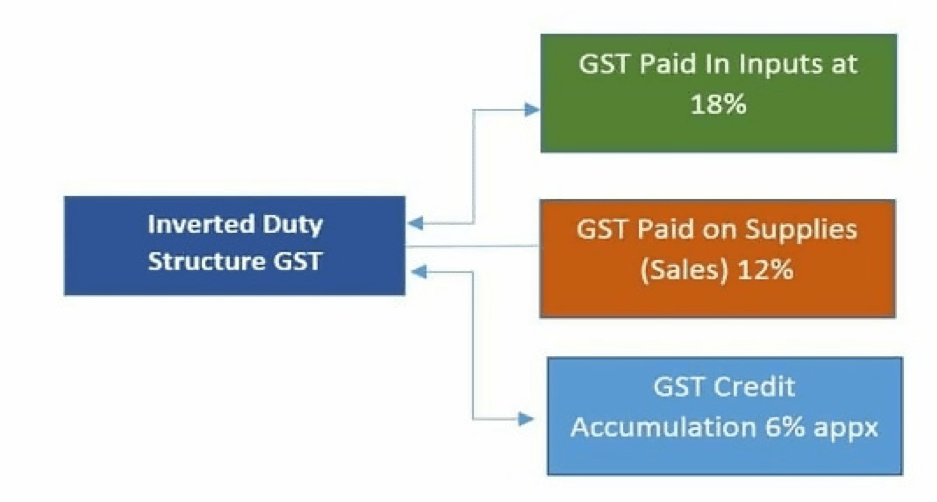

IFCCL GST Refund services offers a comprehensive service designed to simplify and expedite the process of claiming GST refunds for businesses, particularly exporters, e-commerce sellers, and businesses facing inverted duty structures. With IFCCL GST Refund services, businesses can ensure a smoother, more efficient GST refund process, helping them reclaim eligible amounts faster and with guaranteed success. Here’s a breakdown of their services and how they assist clients in maximizing their refunds efficiently: GST Refund Services Offered by IFCCL GST Refund services:

- Export Refunds:

- GST TCS Refund:

- Inverted Duty & Other Refunds:

- GST Litigation Support:

- We are also support in following services related to DGFT and Foreign Trade compliances under the Foreign Trade Policy (FTP) and CBIC provisions:

1. CE Certificate for Fixation of SION

2. CE Certificate for Advance Authorization for Duty-Free Import

3. CE Certificate for Self-Ratification of Duty-Free Import

4. CE Certificate for Installation of Machines under the EPCG Scheme

5. CE Certificate for Nexus under EPCG Scheme

6. CE Certificate for Fixation of Drawback Rates (DBK-I)

7. CE Certificate for Investment in Plant & Machinery as required by 100% EOU

8. CE Certificate for Exemption of Custom Duty on Capital Goods, Components & Spares

9. CE Certificate for Exemption to Goods Imported under Credit Entitlement Scheme

10. CE Certificate for Export of Defective Parts for Repair & Return

11. CE Certificate for Sale of Material Imported for SEZ

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.