Introduction Framework of Faceless Assessment

Table of Contents

Digital Transformation in Tax Administration Faceless Assessment

Introduction

The Income Tax Act, 1961, has been subject to continual reforms aimed at Increasing clarity and efficiency, Promoting voluntary compliance and Minimizing malpractices such as

-

- Wrongful deductions

- Underreporting of income

- Non-disclosure of taxable income

To address these concerns and usher in modernization, the Faceless E-Assessment Scheme was introduced in the Union Budget 2019, post general elections, marking a strategic move toward Digital India and ease of doing business.

What is Assessment :

Under the Income Tax Act, assessment refers to the process of determining Total taxable income, Applicable tax liability, and Compliance with disclosure requirements. In the following cases Common Triggers for Scrutiny inder income tax act.

- TDS mismatch

- Income discrepancies

- Late/non-filing of returns

- Undisclosed assets or foreign income

These red flags typically initiate scrutiny assessments under sections like 143(2), 142(1), 147, etc. The Faceless Assessment Scheme under Section 144B is a landmark tax reform designed to modernize and digitize India’s tax administration. By creating specialized units and enforcing jurisdiction-free, paperless assessments, the scheme enhances fairness, reduces compliance burden, and fosters trust in the tax system.

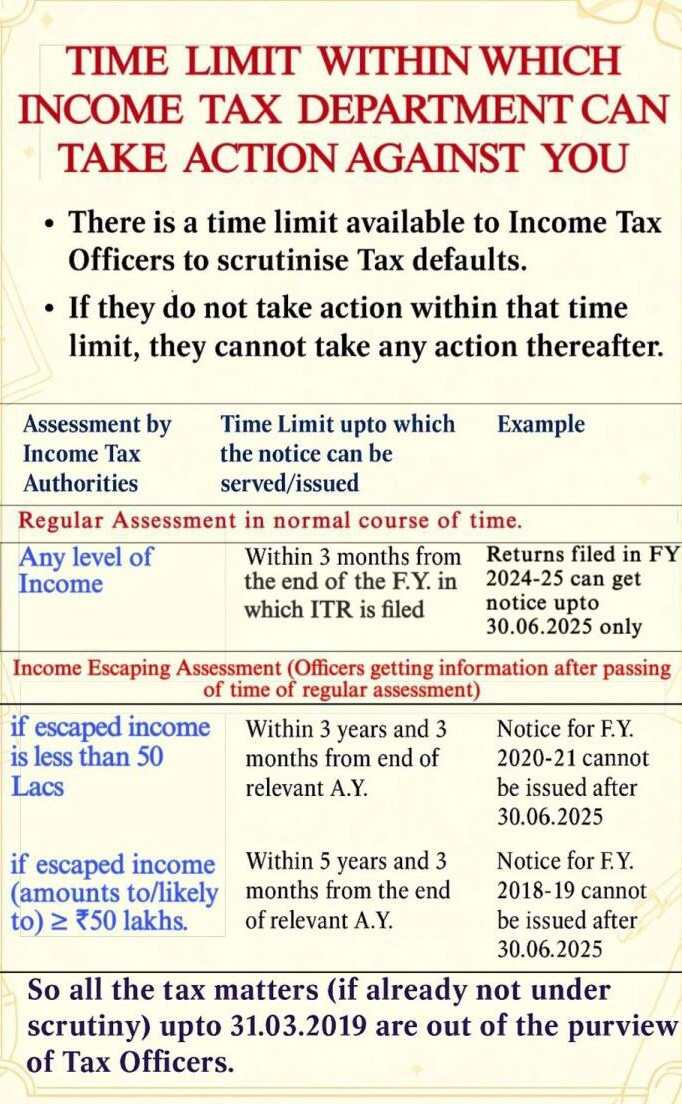

Regular Assessment (Normal Scrutiny) :

Time Limit: 3 months from the end of the financial year (F.Y.) in which the Income Tax Return (ITR) is filed. Example: If you file your return in FY 2024–25, the department can issue a notice only up to 30.06.2025.

Income Escaping Assessment (Reassessment) :

This applies when the department receives new information after the regular assessment period.

a) Escaped Income < ₹50 Lakhs : Time Limit: 3 years and 3 months from the end of the relevant assessment year (A.Y.). Example: For FY 2020–21, notice cannot be issued after 30.06.2025.

b) Escaped Income ≥ ₹50 Lakhs : Time Limit: 5 years and 3 months from the end of the relevant A.Y. Example: For FY 2018–19, notice cannot be issued after 30.06.2025. Tax matters up to 31.03.2019 (if not already under scrutiny) are outside the purview of Income Tax Officers.

Evolution to E-Assessment

- Objectives of E-Assessment is to remove physical interface, Promote transparency, accountability, and fairness and ensure jurisdiction-free, technology-based, and data-driven assessments

- Core Features of E-Assessment is Automated case allocation using AI/ML, Anonymity maintained across units and taxpayer, Online submission of responses, documents, and evidence, No physical appearance at tax offices, and Structured communication via the National e-Assessment Centre (NeAC)

- Policy Alignment of E-Assessment is to Faceless assessments are in line with The Digital India initiative, Ease of Doing Business reforms and enhancing India’s global image as a transparent tax regime

Section 144B: Legal Backbone for Digital Tax Governance :

The Faceless Assessment Scheme under Section 144B is a landmark tax reform designed to modernize and digitize India’s tax administration. By creating specialized units and enforcing jurisdiction-free, paperless assessments, the scheme enhances fairness, reduces compliance burden, and fosters trust in the tax system. Core Objectives of Section 144B to make Transparency, Fairness, Efficiency and Reduced Human Interface. Key Features of Section 144B

| Feature | Description |

| 1. Faceless Assessment Mechanism | Eliminates direct contact between taxpayer and tax officer |

| 2. NFAC (National Faceless Assessment Centre) | Coordinates all communication and central workflow |

| 3. Specialized Assessment Units | Examine returns, gather data, and prepare draft orders |

| 4. Independent Review Units | Verify draft orders for legal and factual accuracy |

| 5. Automated Case Allocation | System-driven, random, and anonymous case assignment |

| 6. End-to-End E-Communication | All notices and responses are exchanged electronically |

| 7. Virtual Hearing Opportunity | Assessee can request a video hearing to present their case |

| 8. Rectification Provision | Allows correction of errors, ensuring natural justice |

Institutional Framework: Centres and Functional Units

National Faceless Assessment Centre (NFAC)

- Central hub for faceless assessments

- Assigns cases, facilitates communication, finalizes orders

- Ensures uniformity, standardization, and nationwide coordination

Regional Faceless Assessment Centres

- Located within jurisdictions of Principal Chief Commissioners

- Handle local implementation and assist NFAC

- Reduce burden on central systems by handling region-specific cases

Key Structural Features of Centres and Functional Units

- NeAC (National e-Assessment Centre) – The nerve centre coordinating the entire faceless process.

- AU (Assessment Unit) – Evaluates facts, evidence, and drafts assessment orders.

- VU (Verification Unit) – Handles verification/inquiry functions.

- TU (Technical Unit) – Offers expertise (valuation, transfer pricing, legal).

- RU (Review Unit) – Ensures checks on legal and factual aspects before finalization.

Functional Units in the Faceless Scheme

| Unit | Function |

| Assessment Units | Core team to analyze submissions, identify issues, draft orders |

| Verification Units | Conduct factual inquiries, verify documents and data |

| Technical Units | Handle complex issues like transfer pricing, valuation, IT, legal, audit |

| Review Units | Final check of draft orders: legal correctness, facts, computation |

Faceless E-Assessment Process – Step-by-Step Summary

| Step | Activity | Relevant Provision/Unit |

| 1 | Notice under Section 143(2) is issued | NeAC |

| 2 | Assessee submits electronic response within 15 days | Assessee |

| 3 | Intimation regarding Faceless Assessment is sent | NeAC |

| 4 | Automated Case Allocation to Assessment Unit (AU) | AI-based system |

| 5 | AU may seek help from: – Verification Unit (VU) – Technical Unit (TU) – Additional info via NeAC |

AU |

| 6 | NeAC acts on AU’s request by: – Serving notices – Forwarding verification or technical queries |

NeAC |

| 7 | Reports from VU/TU received & shared with AU | NeAC |

| 8 | If non-compliance by assessee, Show-cause Notice u/s 144 is issued | NeAC |

| 9 | Draft Assessment Order is prepared by AU | AU |

| 10 | Risk evaluation by NeAC; draft may be: – Finalized – Sent to Review Unit (RU) – Sent for Show Cause |

NeAC |

| 11 | Review by RU: factual, legal, and computational accuracy | RU |

| 12 | If modifications suggested, reassignment to different AU | NeAC |

| 13 | Show-cause reply by Assessee is considered | Assessee & AU |

| 14 | AU prepares Revised Draft Order | AU |

| 15 | Final Assessment Order issued. Hearing opportunity provided if prejudicial | NeAC |

| 16 | Records transferred to Jurisdictional AO for further action | NeAC to AO |

| (Optional) | At any stage, case may be retransferred to Jurisdictional AO with CBDT approval | NeAC/CBDT |

Impact and Benefits of Faceless E-Assessment Process

| Benefit | Result |

| Reduced Interface | Minimizes corruption and subjectivity |

| Standardized Process | Consistent application of tax law |

| Decentralized Efficiency | Enables faster disposal of cases with lower errors |

| Enhanced Taxpayer Confidence | Transparent, fair, and accountable tax assessments |

| Technological Integration | Supports India’s Digital India & Ease of Doing Business goals |

Legal Backbone of Faceless E-Assessment Process

- Section 143(2): Initiation of scrutiny.

- Section 144B: Governs faceless assessment procedure.

- Section 144: Best judgment assessment (non-compliance cases).

- Sections 142(1), 142(2A), 148: Powers to call for information, conduct special audit, and reopen assessments.

Benefits of Faceless Assessment

- Transparency – Eliminates human discretion and subjectivity.

- Efficiency – Tech-driven automation and timeline-based procedures.

- Anonymity – No personal interaction with any specific AO.

- Audit Trail – Digital footprint for all actions ensures accountability.

- Ease of Doing Business – Aligns with India’s vision for Digital Governance.

Key Benefits of Faceless E-Assessment Process

| Benefit | Impact |

| Transparency | Reduces corruption and biased assessments |

| Efficiency | Faster processing and lower compliance costs |

| Anonymity | Eliminates regional or personal bias |

| Centralization | Enables standard procedures nationwide |

| Reduced Litigation | Better documented, reasoned orders |

Types of Assessments Under the Income Tax Act

The Income Tax Act, 1961 provides for several types of assessments to ensure accurate reporting, transparency, and compliance. With the advent of the Faceless Assessment Scheme, these processes have become more efficient and taxpayer-friendly.

Summary Assessment – Section 143(1)

A preliminary assessment done without any interaction with the assessee. It focuses on basic verification of the return. Key Features:

- Correction of arithmetical errors

- Identification of incorrect claims apparent from the return

- Adjustment based on Form 26AS, Form 16, or Tax Audit Report

Time Limit: Must be completed within 9 months from the end of the financial year in which the return is filed.

Scrutiny Assessment – Section 143(3)

Also called detailed assessment, it is carried out to ensure complete accuracy of the return and supporting claims. Key Features:

- Examination of books of accounts and supporting documents

- Verification of deductions, exemptions, and income disclosures

- Notices may be issued and inquiries conducted

- Governed under the Faceless Assessment Scheme, eliminating physical interface and ensuring transparency.

Best Judgment Assessment – Section 144

Best Judgment Assessment Applied when the assessee to Fails to file a return, Does not respond to notices under Section 142(1) or 143(2), and Does not furnish required documents. Key Features of Best Judgment Assessment is :

- Assessment is made by the AO based on available data and best judgment

- Carried out electronically under the faceless regime

- Income Escaping Assessment – Section 147 : Initiated when the AO has reason to believe that income has escaped assessment for a particular year. Key Triggers:

-

-

- Non-disclosure of income

- Wrong claim of exemption/deduction

- New information post original assessment

-

Legal Safeguards:

- Governed by Sections 148 to 153

- Prior approval from competent authority is mandatory

- Follows faceless procedures for reassessment

Assessment Overview Table

| S. No. | Section | Assessment Type | Trigger/Scenario |

| 1. | 143(1) | Summary Assessment | Basic verification and automatic processing of return |

| 2. | 143(3) | Scrutiny Assessment | In-depth review of income, deductions, and claims |

| 3. | 144 | Best Judgment Assessment | Non-filing of return or non-compliance with notices |

| 4. | 147 | Income Escaping Assessment | AO believes income has escaped assessment; new evidence or misreporting noticed |

AO = Assessing Officer

Tax Dept has flagged nearly 1.65 lakh cases for detailed scrutiny u/s 143(2) in 2025

- The Income Tax Dept has flagged nearly 1.65 lakh cases for detailed scrutiny u/s 143(2) a sharp increase compared to previous years.

- This development makes it clear that filing your Income Tax Return is not the end of the compliance process. Even after filing, the Department may issue scrutiny notices if discrepancies, mismatches, or mistakes are detected in the return.

- Taxpayers should therefore ensure Accuracy and consistency in reporting income, deductions, and exemptions. Proper reconciliation of income with Form 26AS, AIS, and TIS data. & Maintenance of supporting documentation to substantiate claims made in the Income Tax Return. In short, filing is only the first step due diligence & compliance continue until the assessment cycle is completed.

Conclusion

- Faceless E-Assessment is not just an administrative reform, but a paradigm shift in India’s tax enforcement and governance. It bridges the gap between taxpayers and authorities with a technology-first, citizen-friendly, and data-reliant approach.

- The Rise of Faceless Assessments: The Faceless E-Assessment Scheme introduced under Section 144B has revolutionized the assessment landscape in India. By leveraging digital infrastructure and minimizing human interface, it achieves Transparency and objectivity, Standardized procedures with audit trails, Time-bound assessments with minimal harassment, Greater ease of compliance for taxpayers.

- The Faceless E-Assessment Supported by units like NFAC (National Faceless Assessment Centre), Assessment Units (AUs), Verification Units (VUs), Technical Units (TUs), Review Units (RUs). This scheme is a landmark shift from a person-driven to a process-driven tax administration, aligning with India’s digital governance vision and enhancing Ease of Doing Business.

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.