SECTION 54F: CONSTRUCTION OF HOUSE WAS NOT COMPLETE

Exemption under Sec. 54F could not be denied merely because the construction of House was not complete in all respects within 3 years of transfer

CIT(Bangalore) v. Smt. B.S. Shantha kumari

Where assessee had invested net sale consideration on transfer of long-term asset in construction of a residential house property, deduction of section 54F could not be denied merely because the construction of house was not complete in all respects within 3 years of transfer

The issue raised by the revenue before the High Court was:

“Whether Tribunal was right in allowing deduction under section 54F of the Income-tax Act (‘the Act’) to assessee though she hadn’t completed the construction of house within three years as per section 54F”

The High Court held in favour of assessee as under:

- Section 54F of the Act is a beneficial provision which promotes construction of residential house. Such provision has to be construed liberally for achieving the purpose for which it has been incorporated in the Statute. The intention of the Legislature in inserting this provision was to encourage investments in the acquisition of a residential plot and completion of construction of a residential house in the plot so acquired.

- A bare perusal of said provision does not even remotely suggest that it intends to convey that such construction should be completed in all respects in 3 years and/or make it habitable.

- The essence of said provision is to ensure that assessee who received capital gains would invest same by constructing a residential house and if assessee is able to establish that he had invested the net consideration within the stipulated period, he would be entitled to get the benefit of Section 54F.

- Though such construction of building may not be complete in all respects that by itself would not dis-entitle the assessee to the benefit flowing from Section 54F.

- AO was not justified in denying Section 54F relief since assessee had invested entire consideration in a residential house property and also produced material evidence before the CIT (A) to demonstrate that the construction was on the verge of completion by producing photographs.

No concealment penalty when AO failed to record satisfaction that there was concealment of income/particulars

Where Assessing Officer had not recorded satisfaction that there was concealment of income, or furnishing of inaccurate particulars, no penalty could be levied under section 271(1)(c)

Kartik Mehra v. DCIT, Kolkata (ITAT KOLKATA)

FACTS OF THE CASE

Search and seizure operation had taken place at various business and residential premises of the assessee’s group and associates. The group made total disclosure of Rs. 6 crores in the hands of various assessee of the group. In the case of instant assessee, disclosure of additional income of Rs. 7.96 lakhs was made for the impugned assessment year, and disclosure of Rs. 2.25 lakhs was made. The assessee filed his return of income declaring total income of Rs. 4.31 lakhs which includes the additional income of Rs. 2.25 lakhs. The assessment was completed.

The Assessing Officer initiated penalty proceedings under section 271(1)(c) and ultimately penalty was imposed.

On appeal, the Commissioner (Appeals) dismissed the appeal of the assessee.

On second appeal:

HELD

The penalty under section 271(1)(c) can be levied for either of the charge. The penalty order simply states that this is a fit case where provisions of section 271(1)(c) are clearly attract. It does not state for what default penalty is levied. Section 271(1)(c)(iii) is expressly clear that the penalty can be levied for concealment of particulars of income or furnishing of inaccurate particulars of income. It is the particulars of income which is the common subject matter of both the charges. The word ‘conceal‘ as per Webster’s Dictionary means ‘to hide, withdraw, or remove from observation; cover or keep from sight; to keep secret; to avoid disclosing or divulging’. That means non-disclosure of particulars of income. On the other hand, where particulars are disclosed but such disclosure is not correct, true or accurate, it would amount to furnishing of inaccurate particulars of income. For example, in case of businessman, if a particular transaction of sale is not shown in the books, it would amount to concealment of particulars of income while sale is shown but at a lesser value, it would amount to furnishing of inaccurate particulars of income.

Explanation 1 to section 271(1)(c) cannot be applied where charge against the ‘assessee’ is furnishing of inaccurate particulars of income since it provides a deeming fiction qua concealment of particulars of income only and consequently cannot be extended to a case where charge against the ‘assessee’ is furnishing of inaccurate particulars of income. On the other hand, where charge against the ‘assessee’ is concealment of particulars of income, the Assessing Officer has to establish either that ‘assessee’ has not disclosed the particulars of income under the main provisions or the case of ‘assessee’ falls within the scope of the deeming fictions created under the explanations. For example, the ‘assessee’ might not disclose particular sales or dividend income or income from any source. Such instances would fall under the main provisions itself. In such cases, the burden is on the Assessing Officer to establish the existence of the charge on the basis of material on record.

Explanation 1 to section 271(1)(c) states that the amount added or disallowed in computing the total income of the assessee shall be deemed to be the income in respect of which particulars have been concealed. This deeming provision is not absolute one but is rebuttable one. It only shifts the onus on the assessee.

Explanation 1 refers to the two situations in which presumption of the concealment off the particulars of income is deemed. It is not applicable where the charge against the assessee is furnishing inaccurate particulars of the income.

The first situation is where the assessee in respect of any fact material to the computation of his total income fails to offer an explanation or offers an explanation, which is found by the Assessing Officer or the Commissioner to be false.

The second situation is where the assessee in respect of any facts material to the computation of his total income offers an explanation which, the assessee is not able to substantiate and also fails to prove that such explanation was bona fide one and that all the facts relating to the computation of total income have been disclosed by him. The presumption available under Explanation to section 271(1)(c), cannot be drawn unless the case of the assessee falls under either of the clause (a) or (b).

In this case, the Assessing Officer has not brought out any specific charge for which the penalty has been imposed on the assessee under section 271(1)(c). He has not brought out whether the assessee has concealed the particulars of income or whether the assessee has furnished inaccurate particulars of income.

The Assessing Officer levied the penalty for both the charges without mentioning any specific charge. The satisfaction of the Assessing Officer about the concealment of particulars of income or furnishing of inaccurate particulars of such income is essential before levying any penalty under section 271(1)(c). The Assessing Officer as is apparent from the penalty order has not satisfied about the concealment of particulars of income or furnishing of inaccurate particulars of income on the part of the assessee. On this basis itself the penalty was deleted.

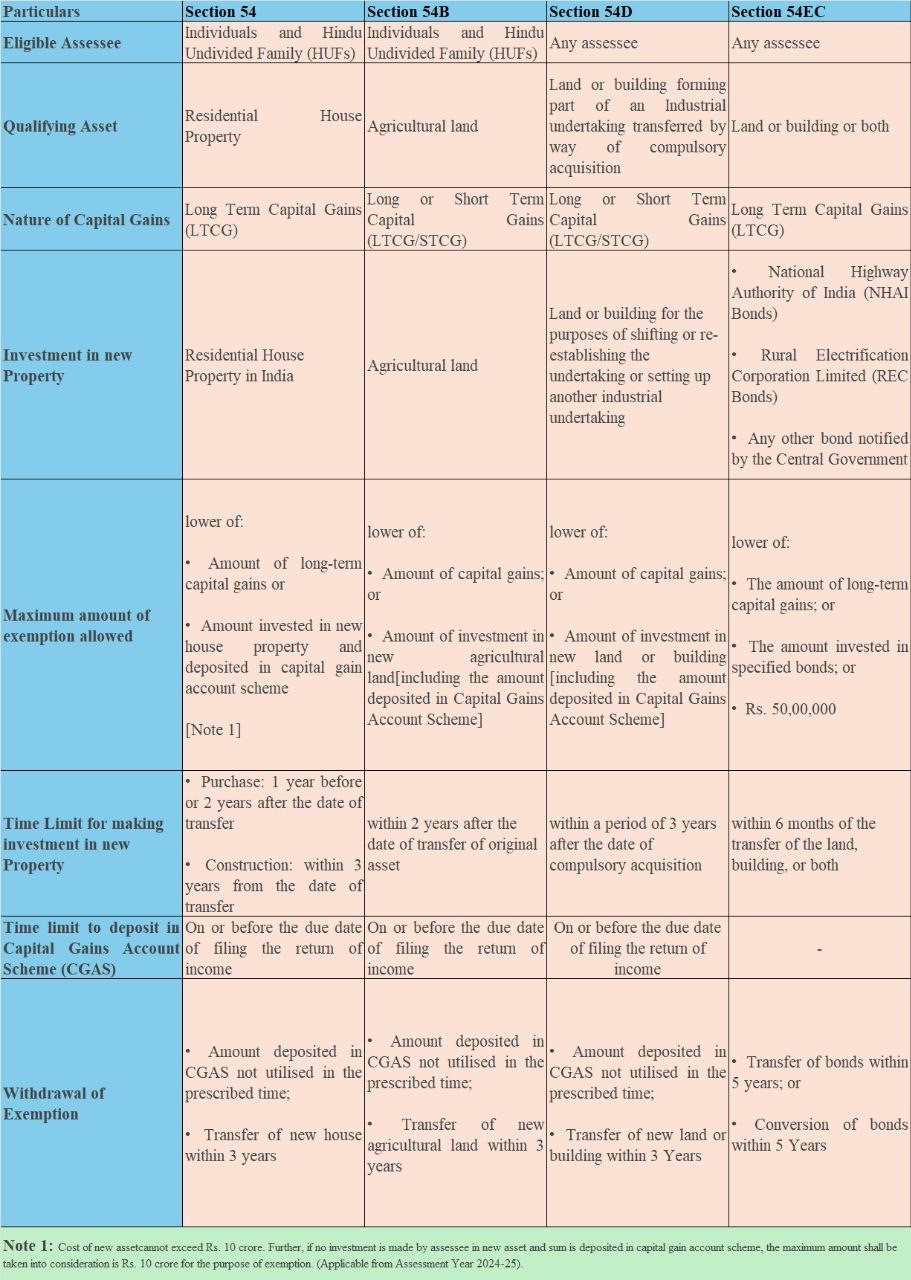

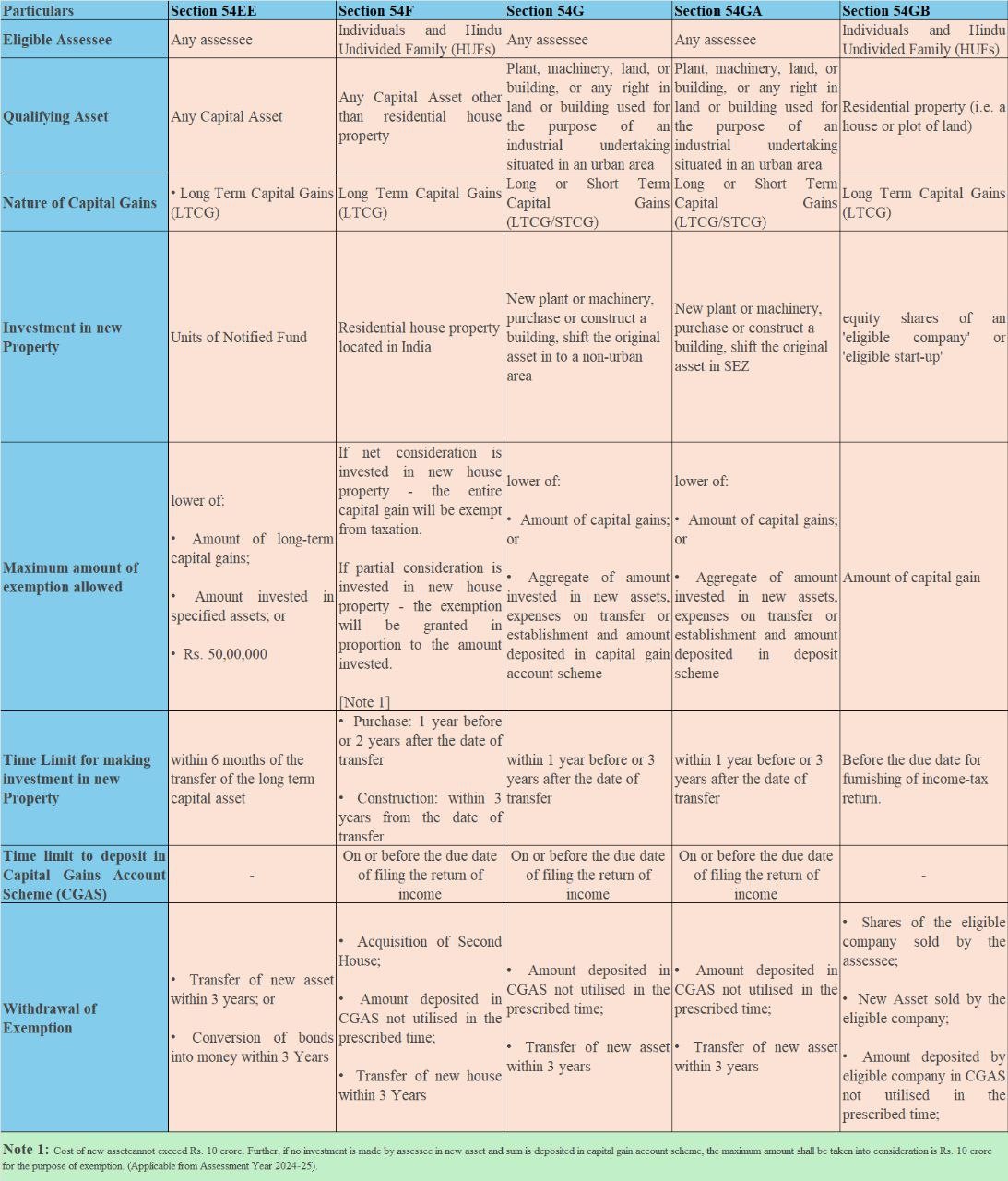

Various Capital Gain Exemption Scheme under Income Tax law

Query : Old property purchased in 2007 – 7lacs, old property sold in dec 2024 – 52 lacs and new property though purchased (means saled deed executed) in dec 24 for 60 lacs but the payment for the same was being done from 2017 itself. i.e. From 2017 to 2021 – 52lacs were paid and in 2024 – 8lacs were paid only. is the relief under section 54 shall be available on the whole amount accrued as LTCG??

Answer: Claiming an exemption under Section 54 of the Income Tax Act depends on whether the payments made toward the new property (from 2017 to 2021) qualify as part of the reinvestment: Eligibility Criteria for Section 54:

- Purpose of Reinvestment: The exemption applies if the capital gains from the sale of a residential property are reinvested in a new residential property.

- The new property must be purchased within one year before or two years after the date of transfer of the original property. Alternatively, if it is constructed, the construction must be completed within three years from the date of transfer.

- Payments Made Between 2017 and 2021: Payments made toward the new property prior to the sale of the old property (from 2017 to 2021) would ordinarily not qualify as a reinvestment under Section 54 because they were made outside the permissible one-year window before the transfer of the old property.

- Sale Deed Executed in December 2024: If the sale deed of the new property was executed in December 2024, it falls within the permissible time frame (two years after the transfer of the old property). The date of execution of the sale deed is crucial for determining the date of “purchase” of the new property.

- In case payments Considered as Advance: Payments made prior to the sale of the old property could be treated as advances. However, for exemption under Section 54, the critical factor is whether the “purchase” of the new property was completed within the specified time frame.

- Judicial Precedents Courts have interpreted Section 54 liberally in some cases, emphasizing the substance over the form. If the intention to purchase the new property can be established and the transaction is completed within the specified time, the exemption has been allowed in some instances, even when part of the payments was made before the transfer of the old property.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances; Hope the information will assist you in your Professional endeavors. For query or help, contact: singh@caindelhiindia.com or call at 09555 555 480

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.