Resident but Not Ordinarily Resident tax status in India

Table of Contents

Resident but Not Ordinarily Resident (RNOR) tax status in India

Who is a Resident but Not Ordinarily Resident (RNOR)?

RNOR Status: The Hidden Tax Advantage for Returning NRIs. RNOR is a special tax classification under Indian income tax law. It applies to returning NRIs and provides a bridge between full non-resident and resident status—offering limited-time tax exemptions on foreign income. RNOR (Resident but Not Ordinarily Resident) status — a transitional tax status under Indian Income Tax Law designed for returning NRIs (Non-Resident Indians).

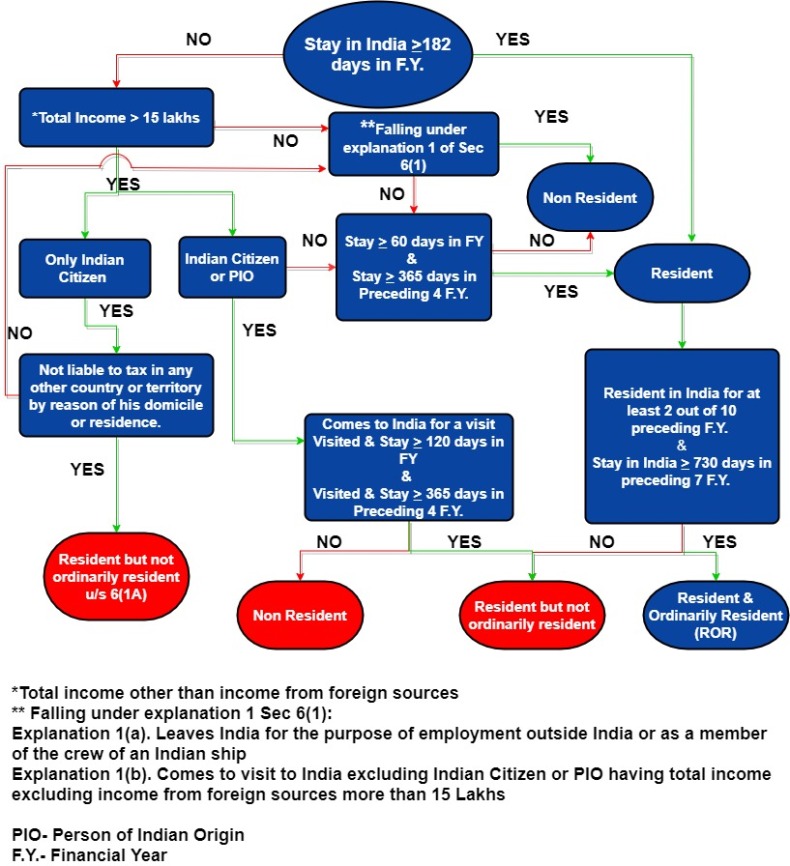

Qualifies for RNOR : To qualify as RNOR (Resident but Not Ordinarily Resident), you must satisfy both steps:

- Step 1: You must be a Resident : Reside in India ≥182 days in the current financial year OR Reside 60 days in the year of return AND 365 days over the past 4 years

- Step 2: Meet ONE of the following: Non-resident in 9 of the last 10 years OR Reside in India for ≤729 days in the last 7 years

Additional Specific RNOR Conditions: Indian citizens/PIOs with income >₹15 lakh in India and stay of 120–182 days in a financial year. Deemed residents whose global income is not taxed in any other country.

In summary : RNOR – Resident but Not Ordinarily Resident

Person can become an RNOR if person :

- Were a non-resident in 9 out of 10 preceding years, or

- Stayed in India for ≤729 days during the last 7 financial years, or

- Are a citizen/PIO with Indian income > ₹15 lakh and stay in India between 120–181 days, and are not liable to tax in another country.

- Duration: RNOR status is available for up to 3 years after returning to India.

RNOR Income Tax Rules Summary

| Type of Income | Taxability in India |

| Income earned in or received in India | Taxable |

| Income accruing in India, regardless of where received | Taxable |

| Foreign business income controlled from India | Taxable |

| Other income earned and received abroad | Not Taxable |

| Remittance to India of foreign income from earlier years | Not Taxable |

RNOR Tax Benefits

No Tax on Foreign Income : Income from the following is not taxable in India during RNOR status:

- Salary earned abroad

- Foreign rental income

- Foreign interest/dividends

- Capital gains on overseas assets

- Exception: If the income is from a business controlled in India, it may be taxable.

NRE/NRO Account Interest Exemption

- Interest on NRE/NRO accounts is tax-free for up to 2 years after return. After 2 years, interest becomes taxable unless moved to RFC account

Capital Gains Flexibility

- No tax on capital gains from overseas investments. Offers flexibility in managing foreign assets without Indian tax burden

Foreign income remains exempt from Indian taxation details are mention as below :

- Rental income from property located abroad

- Dividends and interest earned on foreign securities and deposits

- Withdrawals from offshore retirement accounts (e.g., 401(k), IRA)

- Capital gains from sale of foreign assets

- Interest from NRE/FCNR deposits (if converted to RFC account)

How to Claim RNOR (Resident but Not Ordinarily Resident) Status

- Declare residential status correctly under Section 6 of the Income-tax Act when filing your ITR. Keep documentation: passport stamps, visa, and travel history.

- On RNOR (Resident but Not Ordinarily Resident ) status change than Notify banks. Thereafter RNOR has to Convert NRE/FCNR to RFC accounts. And RNOR has to Submit Form 67 (if claiming tax credit under DTAA). RNOR has to Maintain records of days spent in India.

Actionable Checklist for RNORs

- Declare RNOR status correctly under Section 6 of Income Tax Act in ITR

- Maintain travel records, passport stamps, and visa history

- Notify banks to convert NRE/FCNR to RFC accounts

- File Form 67 to claim foreign tax credit under DTAA, if applicable

- Keep documentation to prove foreign income origin and receipt location

- Benefits of RNOR (Resident but Not Ordinarily Resident) Status

- Foreign income not taxed in India.

- Interest on RFC accounts is tax-free.

- Can use foreign tax credits via Form 67.

How Long Can You Be Resident but Not Ordinarily Resident (RNOR)?

- RNOR status typically lasts 2 to 3 years.

- Returning late in the financial year may help extend Resident but Not Ordinarily Resident (RNOR) eligibility.

- In summary we can say that RNOR status can be retain up to 3 financial years after returning to India (subject to meeting conditions annually) and Returning later in the financial year can help you qualify for a longer RNOR period. Additional RNOR Considerations

-

- Life Insurance Plans for RNORs

- RNORs can buy NRI life insurance policies in India

- Premiums can be paid from India or abroad

- Enjoy life cover + tax benefits under Section 80C & 10(10D) (subject to conditions)

Don’t Confuse Income tax act Tax Residency with FEMA act Residency

- Tax Residency = Based on days in India

- FEMA Residency = Based on intention (settling vs. visiting)

- You may be RNOR (tax resident) but FEMA non-resident, and must report NRE/FCNR accounts and foreign assets. You can be tax resident but FEMA non-resident — then report NRE/FCNR accounts and foreign assets.

RFC Account : RFC (Resident Foreign Currency) account is for returning NRIs

- Can hold foreign currency (USD, GBP, EUR etc.)

- Interest earned is tax-free during RNOR status

- Helps manage foreign assets without currency conversion losses

RFC (Resident Foreign Currency) Eligibility:

- Returned to India after at least 1 year abroad

- Permanent relocation to India

- Return after April 18, 1992

After RNOR Status Expires then : Once you become a Resident and Ordinarily Resident (ROR) then Your global income becomes taxable in India and DTAA (Double Taxation Avoidance Agreement) may help reduce double taxation. So Track Your Residency,

- Keep records of passport stamps

- Calculate stay carefully to avoid unintended resident status

Automatic RNOR Classification: RNOR don’t need to apply. RNOR status is determined based on Travel history, Number of days stayed in India, Income thresholds

Taxability Comparison: NRI vs RNOR vs Resident

| Type of Income | NRI | RNOR | Resident |

| Income earned or received in India | Taxable | Taxable | Taxable |

| Foreign income (earned & received outside India) | Not taxable | Not taxable | Taxable |

| Foreign business income controlled from India | Not taxable | Taxable | Taxable |

| Salary received in India for foreign services (e.g., Govt job) | Taxable | Taxable | Taxable |

We as tax expert consultants know that your RNOR rules are time-sensitive and complex; we as tax advisors can help with:

-

- RFC/NRE/NRO account restructuring

- Capital gains planning

- DTAA claims via Form 67

- ITR filing with correct residential status

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.