Taxation of cryptocurrencies in India

Table of Contents

Cryptocurrency Taxation in India

The income tax department reported that the taxation system for cryptocurrency in India has been established as follows:

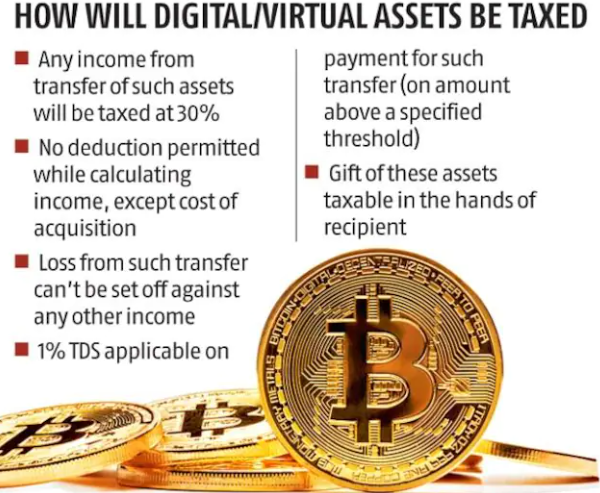

- With effect from April 2022, income generated from cryptocurrency transactions is subject to a 30% tax. No income tax deductions against any expenses whatsoever is allowed.

- Moreover, crypto businesses are expected to pay GST.

- Furthermore, any transactions conducted by such businesses is also liable for a 1% tax deduction at source.

Tax Deducted at Source Applicability—Indian Cryptocurrency Taxation

Taxation of cryptocurrencies: In India, the gains from trading cryptocurrencies are subject to tax at 30% (plus 4% cess) as per section 115BBH. The Tax Deducted at Source rate for crypto is set at 1%. Starting from July 01, 2022, the buyer will be responsible for deducting TDS at the 1% rate while making payment to the seller for the transfer of crypto/NFT. Any transfer of crypto assets on or after 1 July 2022 for an amount of INR 50,000 or INR 10,000 in some cases is subject to a Tax Deducted at Source at 1% U/s194S.

- As of April 2022, income from cryptocurrency transactions is subject to a 30% tax rate; these businesses will likely also be required to pay the Goods and Services Tax at a rate of 28%.

- Moreover, a 1% tax deduction at the source will be available on any transaction carried out by such enterprises.

- If the transaction takes place on an exchange, then the exchange may deduct the tax deducted at source and pay the balance to the seller. Indian exchanges automatically deduct Tax Deducted at Source, while individuals trading on foreign exchanges must manually deduct Tax Deducted at Source & file their Tax Deducted at Source

- P2P Transactions: In case of P2P transactions, buyer will be responsible for deducting Tax Deducted at Source & filing Form 26QE or 26Q, whichever is applicable. Eg: Buying cryptocurrency using INR over a P2P platform or international exchange.

- Crypto-to-Crypto Transactions: Tax Deducted at Source will be applicable on both buyer and seller at 1%. Eg: Buying crypto with stablecoins as per U/s194S.

Cryptocurrency Taxation on Airdrops

- An airdrop refers to the process of distributing cryptocurrency tokens or coin directly to specific wallet addresses, generally for free. Airdrops are done to increase awareness about the token and increase liquidity in the early stages of a new currency. Airdrops are taxed at 30%.

- Airdrops will be taxed on the value determined as per Rule 11UA, i.e. at the fair market value of the tokens as on the date of receipt on exchanges or DEXes. Tax will be levied at 30% on such value. Sell, swap, or spend them later: If you sell, swap or spend those tokens later, then 30% tax will be levied on the gains made.

- Sell, swap, or spend them later: If you sell, swap, or spend those assets later, 30% tax will be levied on the gains made.

Cryptocurrency Taxation on mining of cryptocurrency

- The cryptocurrency mining income received will be taxed at a flat 30%.

- Mining income received from cryptocurrency will be taxed at a flat 30%. The cost of acquisition for the crypto mining will be considered as ‘zero’ for computing the gains at the time of sale. No expenses such as electricity cost or infra cost can be included in the cost of acquisition.

- Cryptocurrency assets received at the time of mining will be taxed on the value determined as per income tax Rule 11UA, i.e. at the fair market value of the tokens as on- if the consideration for the issue of cryptocurrency exceeds the FMV of the cryptocurrency, it shall be chargeable to income tax under the head ‘Income from other sources.’ Rule 11UA prescribes the manner to compute the FMV of such shares

- The date of receipt on exchanges or DEXes. Tax will be levied at 30% on such value.

Cryptocurrency Taxation on Crypto Gifts

- Cryptocurrency can be gifted either via gift cards, cryptocurrency tokens, or a cryptocurrency paper wallet.

Cryptocurrency received as gifts from relatives will be tax-exempt. - However, if the value of the cryptocurrency gift from a non-relative exceeds INR 50,000, it becomes taxable. Cryptocurrency Gifts received on special occasions, via will inheritance or in contemplation of death or marriage, are also exempt from income

How do you calculate 30% tax on cryptocurrency?

- 30% cryptocurrency tax will be levied on the income you made from crypto, which can be calculated as:

Sale Price – Cost Price = Income from Cryptocurrency

Is any exemptions/deductions available for crypto transaction profit?

- No income tax deductions against the expenses are allowed except for the cost of acquiring digital assets.

- This means that a taxpayer cannot claim deductions and exemptions on the profit earned from the purchase and sale of cryptocurrencies.

Whether loss offsetting is available on profits earned from trading crypto futures on Binance India?

-

Losses from crypto trades (including futures) cannot be set off against profits from other crypto trades.

-

Losses also cannot be adjusted against any other income, such as salary, capital gains, or business income.

-

Losses cannot be carried forward to future years. The tax framework explicitly states “No set-off of losses” for VDAs.

Conclusion: Income from crypto transactions is liable to income tax in India

If you engage in any of the following transactions, you will be required to pay a 30% tax:

- Receive cryptocurrency as payment for a service.

- Spending cryptocurrencies to purchase goods or services.

- Receiving Airdrops

- Mining cryptocurrency

- Drawing a salary in crypto

- Receiving cryptocurrency as a gift

- Staking crypto and earning stake benefits

- Exchanging cryptocurrency for other cryptocurrency

- Trading cryptocurrency using fiat currency such as INR

How to report cryptocurrency on a tax return?

- It’s important to keep detailed records of your cryptocurrency transactions, including dates of acquisition and sale, purchase prices, sale prices, and any expenses incurred in the process. This information will be crucial for accurately calculating your tax liability.

- The new income tax return forms include a specific section, ‘Schedule Virtual Delivery Assets for reporting cryptocurrency gains or income.

- As per the standard income tax rules, the gains on the crypto transactions would become taxable as (i) business income or (ii) capital gains. This classification will depend on the investors’ intention and the nature of these transactions.

-

- Business income: If there are frequent trades and high volumes, gains from the cryptocurrency may be categorised as ‘business income.’ In such a case, you may use ITR-3 for reporting the crypto gains.

- Capital gains: On the other hand, if the primary reason for owning the cryptocurrency is to benefit from long-term appreciation in value, then the gains would be classified as ‘capital gains.’ In this case, you may use ITR-2 for reporting the crypto gains.

Disclosure of Crypto Assets in Schedule of Assets and Liabilities

- The Ministry of Corporate Affairs has made it mandatory to disclose gains and losses in virtual currencies. Also, the value of cryptocurrency as of the balance sheet date is to be reported. Accordingly, changes have been made in Schedule III of the Companies Act starting from 1 April 2021.

- This mandate is only for companies, and no such compliance is required from the individual taxpayers. However, reporting and paying taxes on the gains on cryptocurrency is a must for all.

Status of India’s Current Perspective on Cryptocurrency—

- Although the Indian government has stated that crypto is not recognized as legal cash within the nation.

- This does not imply that such operations are prohibited, as there is currently no legislation covering this emerging industry. Holding assets like Bitcoin and other comparable virtual currencies is currently not against the law in India.

- Crypto Exchanges, registered as FIU registration in India, shall be considered for dealing in cryptocurrency, and some of them are CoinX, Unocoin, Bitbns, Zebpay, WazirX, Coinswitch, CoinswitchX and Rario

IFCCL

Office: P-6/90 (2F) Connaught Circus, Connaught Place, New Delhi-110001, India,

Contact: 91-9555 555 480 E-Mail: Singh@caindelhiindia.com

**********************************************************

If this article has helped you in any way, i would appreciate if you could share/like it or leave a comment. Thank you for visiting my blog.

Legal Disclaimer:

The information / articles & any relies to the comments on this blog are provided purely for informational and educational purposes only & are purely based on my understanding / knowledge. They do noy constitute legal advice or legal opinions. The information / articles and any replies to the comments are intended but not promised or guaranteed to be current, complete, or up-to-date and should in no way be taken as a legal advice or an indication of future results. Therefore, i can not take any responsibility for the results or consequences of any attempt to use or adopt any of the information presented on this blog. You are advised not to act or rely on any information / articles contained without first seeking the advice of a practicing professional.